RBNZ Bank Dividend Decision: Impact for Equities, Debt, Hybrids

Quick thoughts on the RBNZ decision to ban NZ banks from paying dividends until the crisis passes and what it means for the Aussie major banks' equities, senior bonds, Tier 2 bonds, and AT1 hybrids:

- APRA has come out and immediately stated that bank dividend policies are a matter for bank boards, although they continue to monitor the situation and encourage banks to maintain prudent capital levels.

- Like the US banking regulator, APRA is not going down the path of trying to dictate capital management policies to bank executives and boards.

- Put differently, APRA (and the US) are not blindly following the lowest common denominator policies of arguably inferior banking regulators, such as those in Europe or the UK. APRA has often exercised jurisdictional independence when it thinks this is appropriate.

- This also makes sense because APRA has over a long period of time worked to ensure the major banks are the best capitalised banks in the world.

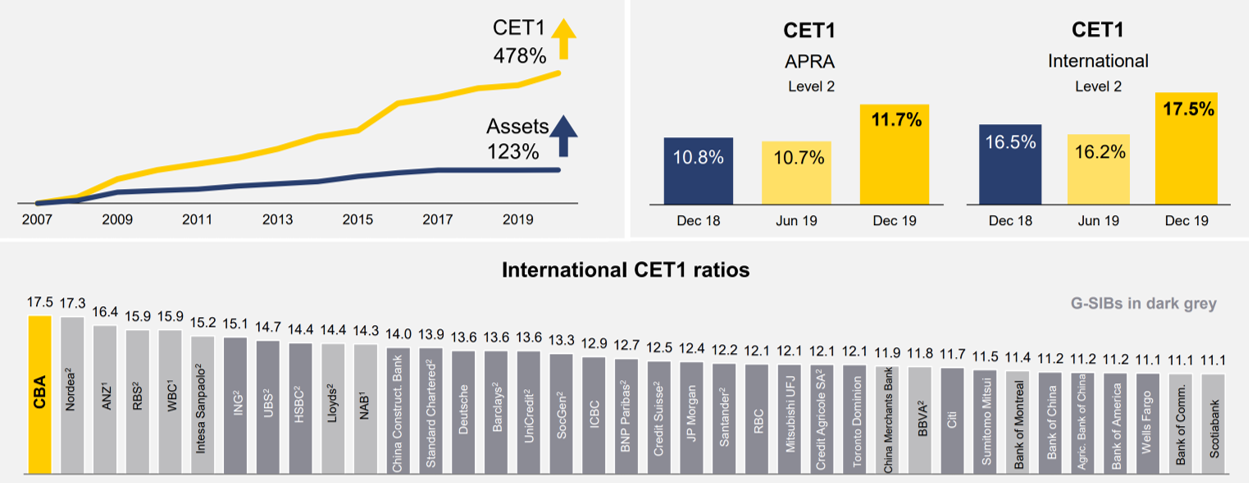

- As at CBA's last reporting date, it has an internationally harmonised common equity tier one capital ratio of 17.5%, which was No.1 amongst its list of large global banks (see first chart). The three other majors were close behind.

- APRA has repeatedly stated that the major banks' have built these huge capital buffers precisely to be utilised as shock absorbers when adversity arrives such as during times like this.

- One unusual thing that the RBNZ did that no other regulator has done globally is prevent the banks calling or repaying their capital instruments until this crisis passes.

- APRA again has taken a very different view, allowing both Macquarie and NAB to repay about $1.8 billion of existing hybrids in March, and then permitting them to withdraw from listing another $2.6 billion of new replacement hybrids that were contractually committed.

- In a weaker banking system, the regulator might have loved these two banks raising very cheap hybrid capital. But by the time the listing came about, hybrid spreads had jumped 300 basis points, which would have imposed immediate losses on these securities.

- So instead of grabbing this newly cheap capital, NAB and Macquarie secured APRA's approval to withdraw these hybrid issues simply because their retail investors would have been worse off. This was a tremendous statement of support from the banks and the regulator for this predominately retail sector.

- In March APRA also allowed Westpac to call and repay a $1.1 billion Tier 2 subordinated bond while not replacing it because the market pricing would have been heinously expensive.

- This week APRA allowed Challenger to defer the call and replacement of its small May hybrid until a future quarterly distribution date when market conditions have normalised. Challenger formally stated that it is committed to calling the security and replacing it with a new issue.

- Other considerations include the fact that the four majors make up almost one-third of all dividend payments on the ASX, and are therefore a key source of income for both retail and institutional investors, including retirees and super funds that are looking to maximise liquidity.

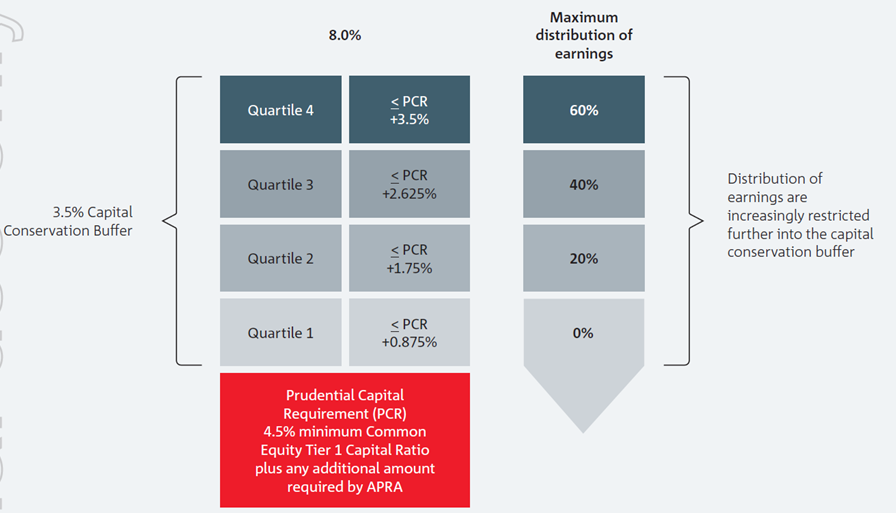

- Importantly, APRA has also already put in place a capital protection system whereby the majors are forced to hold or escrow an increasingly large share of their earnings as their CET1 ratio declines below 8%. These earnings are not allowed to be paid to shareholders (see final image below).

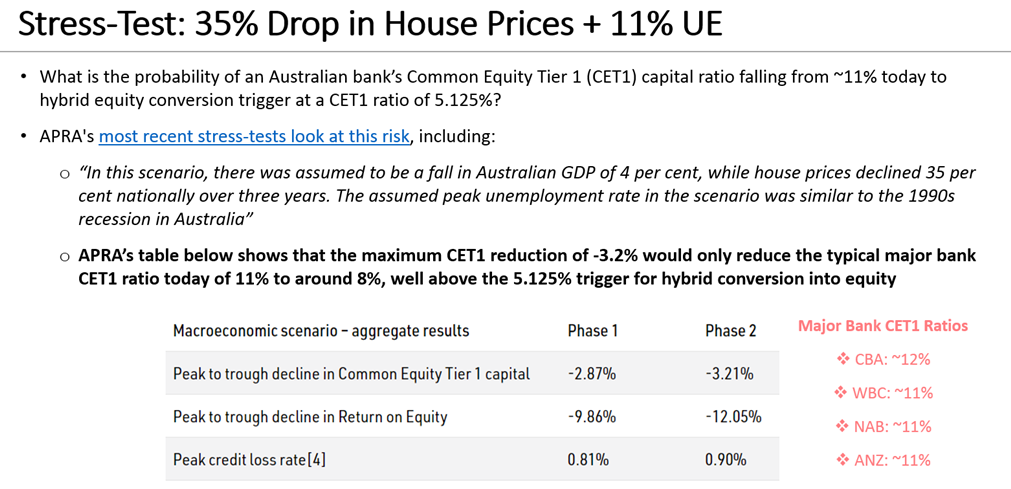

- Finally, APRA recently ran a stress-test of the major banks to look at the impact on their CET1 ratios of a deep recession that was worse than 1991. In this scenario house prices fall 35% and unemployment goes to higher than 11%. The banks' CET1 ratios fell on average by around three percentage points, putting their CET1 ratios at circa 8% and well above the 5.125% level where the automatic conversion of hybrids to equity kicks-in.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Disclaimer: This information has been prepared by Smarter Money Investments Pty Ltd. It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not an indicator of nor assures any future returns or risks. Smarter Money Investments Pty Limited (ACN 153 555 867) is authorised representative #000414337 of Coolabah Capital Institutional Investments Pty Ltd, which holds Australian Financial Services Licence No. 482238 and authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271.

1 topic

4 stocks mentioned

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX playmakers making things happen

Livewire Markets