Scentre Group sell-off reveals the opportunity in index money

Michael Doble

APN Property Group

Imagine it. Your fund manager has just sold a stock that on almost every measure, from valuation and consensus to intuition and common sense, looks cheap. Why aren’t they buying rather than selling?

Seeking an explanation for what seems like a poor decision, their response dumbfounds you. “We sold down because everyone else is doing it.”

It sounds ridiculous, doesn’t it? Until you realise this is the only possible excuse for a gaggle of index fund managers (a collective noun for the species has yet to be invented) selling down Scentre Group, a listed Australian property trust that owns arguably one of the best portfolios of retail assets in the world.

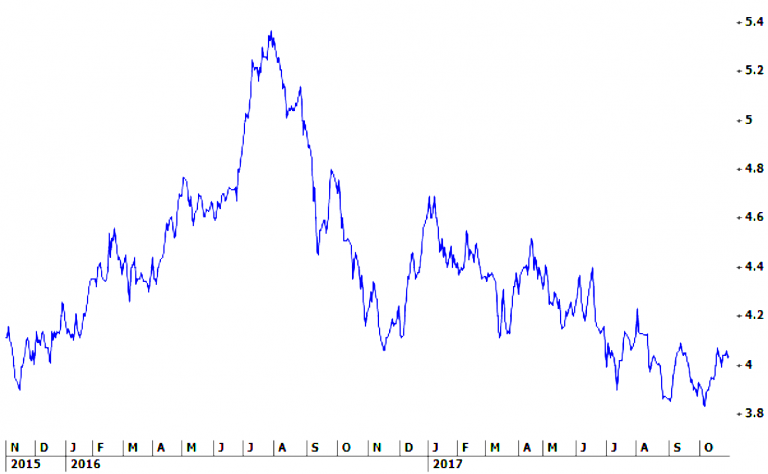

In July 2016, when the price hit around $5.30, the market (presumably) agreed with that view. As of 27 October 2017, with perceptions changing, it has fallen 24%. At one point the stock was trading below the underlying value of its assets. That price ignored the inherent value of the (perpetual) right to manage, develop and lease this circa $34bn portfolio.

SCG 2 year stock price chart to 30 October 2017

Source: Iress. 30 October, 2017

In recent times, the company’s share price performance has been worse than the overall listed property market. Why?

The recent decline in Australian retail sales growth was the starting point. Behind this were cyclical declines in wages growth, higher utility charges, price deflation in apparel and a diminishing residential wealth effect.

These weren’t the only concerns. There was the spectre of Amazon landing in Australia; US equity investors thought that the Australian retail property market is as oversupplied as the US (it isn’t); and that online sales growth will affect all retail assets (it won’t – the weakest assets will be hardest hit).

Soon enough, sentiment changed and Scentre’s share price began to fall. Then the index money effect kicked in. As the price fell, the company’s index weight reduced, triggering further falls. The more index money there is in the market, the stronger the “index money effect” and the greater the price falls (and rises).

None of this is conscious, of course. Index fund managers are required to ignore what we consider important. They do not care that Scentre Group assets are exceptionally well located and managed. They have to disregard the fact that retail outlets in Scentre properties are quite different from those High Street outlets typified by weak ABS retail sales data. They care not about Scentre’s occupancy rate of greater than 99.5%, with new retail chains and concepts taking up space released by struggling department stores.

Index fund managers are obligated to disregard a range of pertinent facts like these in favour of only one fact – a stock’s overall representation in the index. If a stock rises, they buy. If it falls, they sell. And that’s pretty much it.

The modus operandi of the index fund manager is to simply act on the sum of the typically irrational, short term reactions of other investors, expressed through the day-to-day changes in the share price of all the companies on the market.

They say that the trend is your friend but for index investors it’s more than that. It’s their business model.

We think this is absurd but are nevertheless grateful for it. In our view, more index money in the market means more opportunity, with Scentre being a case in point.

Capable managers operating well located real estate are capable of re-invention. Australia’s biggest shopping centres, which are thriving, prove it. Trends come and go but good assets are adaptable and long standing. Our analysis gives us confidence that Westfield shopping centres will not only survive but prosper in the years to come.

In the meantime, the yo-yo business model of the index manager offers savvy investors an opportunity. Recent price falls mean Scentre now features a distribution yield of 5.4% (Source: APN Property Group, 30 0ctober 2017), which is why we’ve bought it recently.

Thank you index fund managers. Now, please return to your black boxes.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

2 stocks mentioned

Michael Doble

Chief Investment Officer, Real Estate Securities

APN Property Group

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

Michael Doble

Chief Investment Officer, Real Estate Securities

APN Property Group

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets