SME Lending March Market Perspective

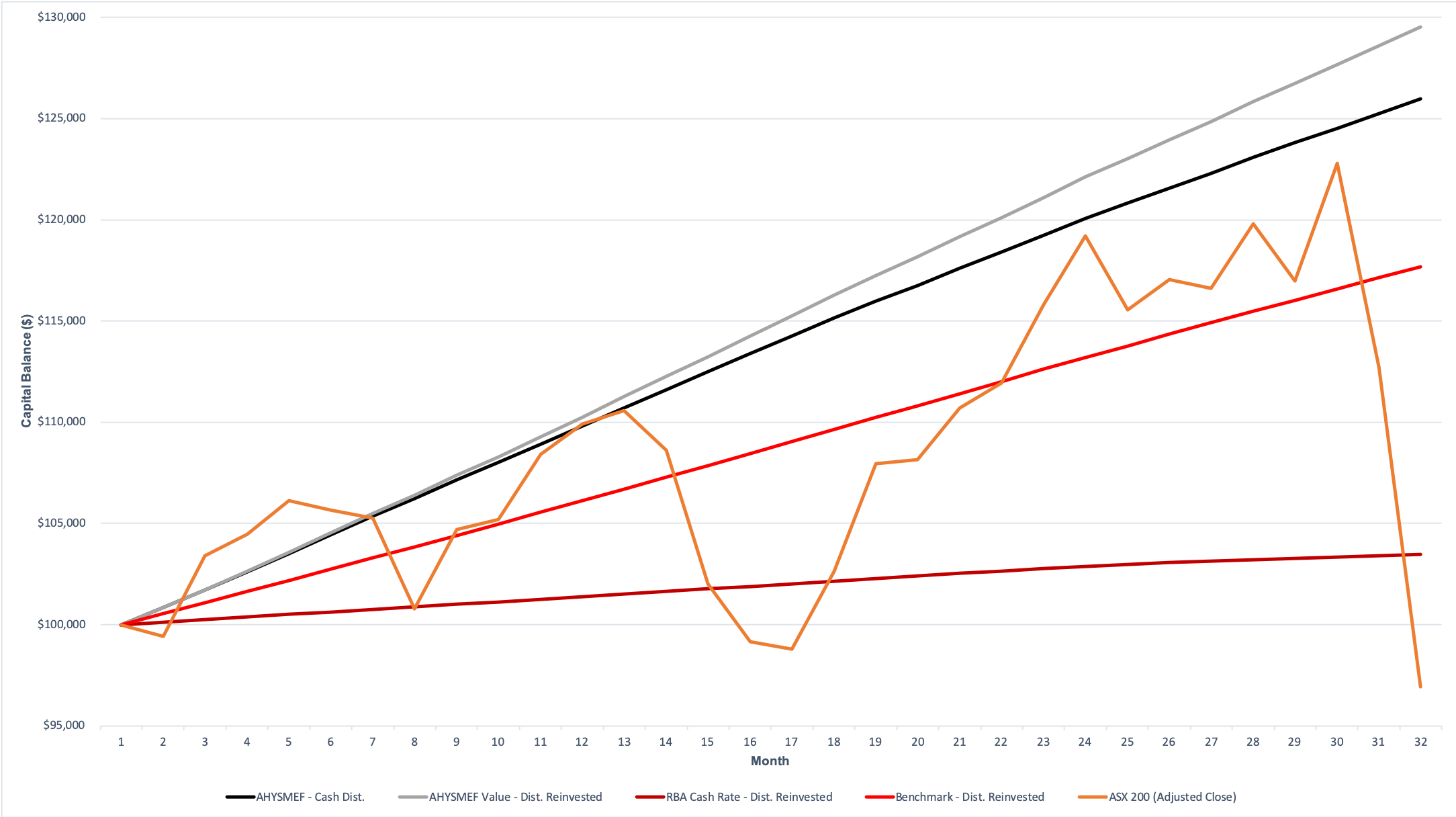

The March ’20 Distribution was the 32nd since the inception of the Aura High Yield SME Fund. We have delivered returns of 9.60% in the last 12 months, and 30.25% since inception, net of fees and expenses on a distribution reinvestment basis. Since inception the fund has outperformed the ASX200 on a cumulative returns basis, with stability in the return profile.*

Given the speed of change in markets, and to maintain relevance of the information, our commentary on the market will have crossover from March into early April. March saw the height of global market panic surrounding the COVID-19 episode. This has somewhat calmed in the following three weeks, as infection rates have reduced, and the Federal Government has started to discuss measures to loosen the current lockdown restrictions. During this period we are very happy with the performance of the book through this volatile period in markets.

•March distribution has risen to 75 bps, up two bps from the February distribution.

•NAV retained at $1.

We see these results as an indication that our work with lenders on actions, such as tightening of lending standards, hypervigilant arrears management and high-frequency communication with our originators, are coming to fruition. Our originators understanding of, and participation in these measures are crucial to navigating this time-period.

Government stimulus Packages

The Federal Government announced the Job Keeper package on March 30. The package, designed to keep employees in their current jobs and ease the cashflow burden of COVID-19 affected businesses countrywide, amounts to $130bn. From May 1, eligible businesses will receive $1500 per fortnight, per employee, backdated to March 30, for six months. Eligible businesses include those who have experienced a 30% decline in turnover or a 50% decline for businesses with greater than $1bn annual turnover. In addition to previous packages and the $105bn from the RBA, stimulus measures now total $320bn or 16.4% of GDP. As at the 14th of April, over 800,000 businesses had registered for the Job Keeper payment.

The Aura High Yield SME fund sees a number of supportive measures as a result of these packages:

The Aura High Yield SME fund sees a number of supportive measures as a result of these packages:

•The increased free cash flow of the underlying borrowers as a result of the new wage subsidy, totalling $19,500 per employee, tax-free, over the next 6 months; and

•$20,000 - $100,000 cash injections to businesses with registered employees.

Furthermore, our Non-ADI lenders have also seen several supportive measures announced:

•50% government guarantee for new loans written by eligible lenders; and

•The announcement of a $15bn fund to provide financing for Non-Bank SME lenders.

There have also been a number of announcements that are supportive to the SME lending market:

•The Structured Finance Support Fund has made its first funding commitments to an Australian SME lender, Judo Bank;

•The AOFM has announced a $250m funding round from the Australian Business Securitisation Fund, a $2bn fund designed to invest in securities issued by SME originator warehouse facilities; and

•A new mandatory code of conduct for commercial tenants and landlords will see SMEs receive rent waivers and a minimum 24 month catch up period on late payments.

Credit Markets

In the broader credit market, the Australian iTraxx, which tracks 5-year credit spreads on investment-grade corporate bonds, rose from 46 bps in late February to a peak of 245 bps on March 23rd in response to the crisis. This reflected an increased risk premium required for corporate credit. The spread on the close of April 14th had fallen to 115.5 bps, but pushed wider in lien with equity markets to 124.5 bps on the 21st of April. We interpret this as a return of some investor confidence in bond markets as analysts are now pricing the inherent risk premium. This reduction in credit spreads has run in line with a rally in equity markets over the last two weeks, as there are some early signs of the virus being controlled in Australia.

What We are Seeing in the Lending Market

As an overarching statement our originators remain on heightened alert and are tightening up accordingly. We are happy with the actions taken by our originators. We are working with our originators to adjust our portfolio to meet the current market conditions, shifting sector exposures to those that are trading well through this period.

Arrears

Our lenders have been very proactive in arrears management, which has shown through in the March arrears read. The focus of lenders at this point is managing the current book, rather than driving volume.

Risk Appetite Tightening

All of our lenders have continued to tighten risk appetites, which has shown through in reduced lending volumes, and increased book quality. Specific sectors have been cut out, however there are a number of sectors such as construction (with an infrastructure focus), agriculture, online retail and logistic that are showing strength in this market.

Volumes – Slower in late March

With the exception of Agrilending, volumes have dropped with risk tightening. Our livestock lender, has been seeing solid growth, as farmers are looking to restock with rains hitting the East coast and providing some much-needed pasture. TradePlus24 has built a solid pipeline of quality deals, however we are yet to fund as the fund is fully deployed.

Summary

Overall, we are seeing more of a positive tone in markets since the peak of market panic around March 23, as cash from government stimulus measures enters the economy, and the infection rates and mortality rates decrease. We are seeing strong opportunities to deploy capital into loans exposed to the agricultural sector, which is currently flourishing, and also to fully insured credit exposures.

Our strong lender assessment process is working at this point. Our lenders are generally taking the right actions with their books, and are maintaining consistent, transparent dialogue with us.

As prudent managers, we are working with our lenders to protect capital, and maintain return levels. We are interacting with the Commonwealth Government to assess whether there are options to work with them to maintain credit flow to Australian SMEs, while meeting our objectives.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brett is responsible for portfolio management and asset origination for the Aura High Yield SME Fund. He has over 15 years’ experience in sales, origination and analysis of debt finance.

........

This document is dated April 2020 and has been issued by Aura Funds Management Pty Ltd (ABN 96 607 158 814, AFSL Authorised Representative no. 1233893 of Aura Capital Pty Ltd AFSL no. 366 230, ABN 48 143 700 887). This document is for information purposes only and does not constitute an offer or invitation for the subscription, purchase or transfer of units in Agrilending (Fund). Accordingly, this document does not constitute an information memorandum, prospectus, offer document or similar document in respect of units or the Fund. This document is only directed at persons who are wholesale clients within the meaning of the Corporations Act. This document may not be made available to any retail client. Neither this document nor anything contained herein nor any presentation in connection with this document shall form the basis of any contract or any obligation of any kind whatsoever.

This document must not be distributed to any party without the express written consent of Aura Funds Management Pty Ltd. All information and opinions expressed herein are subject to change without notice. Neither Aura Funds Management Pty Ltd nor its affiliates, associates, directors, officers, agents, employees or advisers warrant the accuracy of the information provided in this document. The offer of units in the Fund will only be made in, or accompanied by, a copy of information offer document. This presentation contains only indicative terms. Investors should read the offer document, and in particular the risks section there in, before deciding to invest in any securities.

Every care has been exercised in compiling the information contained in this presentation.

Past performance cannot be used as an indicator of future returns. Information on taxation is for general information purposes only and cannot be construed as taxation advice.

2 topics

Brett is responsible for portfolio management and asset origination for the Aura High Yield SME Fund. He has over 15 years’ experience in sales, origination and analysis of debt finance.

Expertise

Brett is responsible for portfolio management and asset origination for the Aura High Yield SME Fund. He has over 15 years’ experience in sales, origination and analysis of debt finance.

Expertise

Comments

Comments

Sign In or Join Free to comment