Stellar earnings results from Corporate Australia

Craig James

CommSec

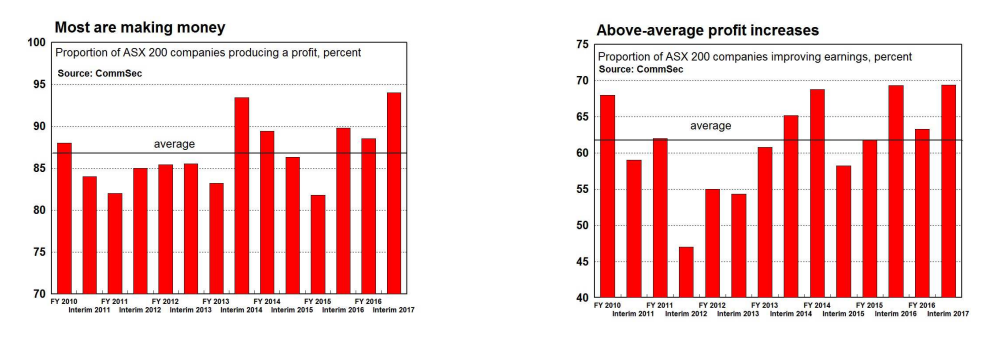

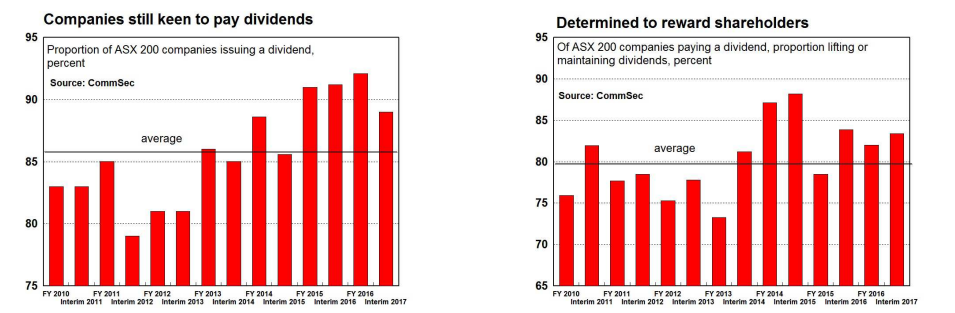

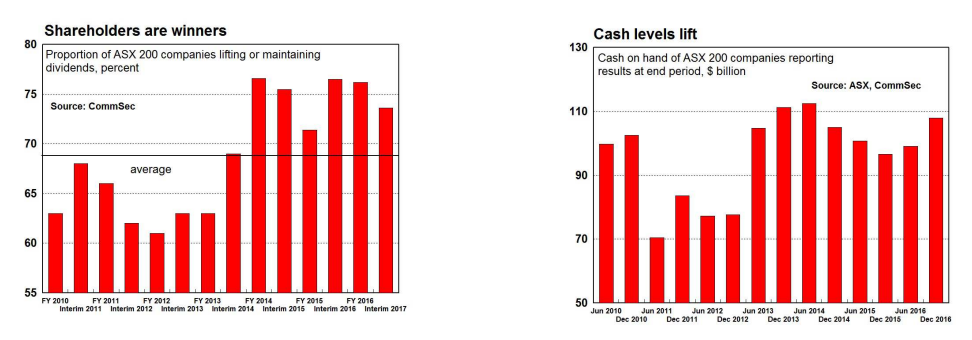

There are still two days of the earnings season to go. Remarkably all but 8 of the 135 companies produced a profit for the six months to December. That is, around 94 per cent of companies made money. Excluding BHP Billiton, aggregate profits lifted by 37 per cent. Almost 89 per cent of full-year reporting companies elected to pay a dividend. Cash levels rose. For all ASX 200 companies reporting interim or full-year results, cash levels rose by 9 per cent to over $108 billion.

The Profit Reporting Season

Every six months CommSec tracks the earnings of Australia’s largest listed companies. Some analysts track whether companies have met broker expectations. That tells you little about the financial performance of companies. And unfortunately only a few brokers are surveyed. Also broker expectations have proved too pessimistic in recent times. Other analysts just track the earnings of those companies they ‘cover’ – the companies they have detailed information on. CommSec includes all ASX 200 companies in its macro (big picture) assessment of the reporting season.

In short, the earnings season has been good. Very good. Only eight companies (so far) from the ASX 200 have produced a statutory loss for the six months to December. Recently many were surprised by survey results that showed that business conditions are the best in nine years. The earnings results confirm that Corporate Australia is in good shape.

There have been two key positive influences:

- Commodity prices (especially iron ore, coal and oil) have risen contrary to expectations.

- The record-breaking home building boom has lifted a lot of boats.

Add in the fact that the Aussie dollar hovered in the 70s against the greenback, down from the higher levels in previous years. The lower Aussie has assisted companies with significant offshore operations.

The main negative was the caution caused by the UK Brexit vote, Australian Federal Election and US Presidential Election. This influence dominated mid-year and was reflected in softer employment and slower business and consumer spending. But as shown by some of the recent economic indicators, positive momentum returned late in 2016 and in early 2017.

The Details: Half-year earnings

CommSec has analysed all results from ASX 200 companies. Traditionally brokers or analysts focus on smaller subsets of results. And some merely focus on just whether companies have met or fallen short of “market expectations”.

Overall, 135 companies from the S&P/ASX 200 have so far reported profits for the six months to December. Including all companies, profits rose 130 per cent over the year to $28.1 billion. But a significant boost is imparted into the results from BHP Billiton. The mining heavyweight swung from a loss of US$5.7 billion to a profit of US$3.45 billion. To include BHP Billiton in the aggregate results would present an incorrect picture of the earnings season.

Some of the key results:

- Excluding BHP Billiton, aggregate profits rose by 37 per cent to $28.1 billion.

- Average earnings per share rose by 19 per cent (ex BHP Billion, up 14 per cent).

- Aggregate sales were up by 5 per cent over the year; aggregate costs/expenses fell by 2 per cent.

- All but 8 companies recorded a profit for the year to June: that is, 94 per cent of companies recorded a profit.

- 69 per cent of companies increased profit over the year; above the long-term average near 60 per cent.

- Aggregate cash holdings rose by 11 per cent on June levels to $82 billion.

- Adding in the 26 companies reporting full-year earnings, cash levels were up by 9 per cent on end June levels to $108 billion.

- Aggregate dividends rose by 6.0 per cent over the year.

- 89 per cent of companies (120 of 135 companies) paid a dividend.

- Of companies paying a dividend, 69 per cent lifted dividends; 14 per cent maintained dividends; and 18.0 per cent of companies cut dividends.

What are the implications for interest rates and investors?

Before the earnings season, the Aussie sharemarket could be considered slightly overvalued with an historic price-earnings ratio sitting near 17, above the longer-term average of 15.7. But the latest earnings results justify the recent gains in the sharemarket. And with the economy gaining momentum in recent months, share prices have scope to track profits higher – particularly in light of the super-low interest rate environment.

We see no need to change our long-held forecasts. We currently expect the All Ordinaries to be between 5,700-5,900 points by mid-2016 (ASX 200 probably 100 points lower) with the index lifting to 5,850-6,100 by end-2017.

Global sharemarkets have lifted markedly since the US Presidential Election on the hope that the new President will cut taxes and increase spending on infrastructure. The hope still exists, but investors are still waiting on the plans being fleshed out. The US Federal Reserve is also expected to lift interest rates over 2017. Investors are closely watching the compliance by OPEC oil countries with production cuts. And there are a number of European elections to watch in coming months, in particular the Dutch election in March and French Presidential election in April.

So clearly the sharemarket will face some potential hurdles. And the risks are reasonably evenly balanced. The good news is that balance sheets across Corporate Australia are in good shape. While some companies have continued to pay out dividends, others have also been keen to pay down debt levels, to reduce risk and provide some flexibility to respond to opportunities in 2017.

Indeed companies have decisions to make. Cash levels are near the highest in the 14 earnings seasons we have covered. Australia’s biggest companies have access to near $108 billion (more companies are still to report).

Apart from the geopolitical uncertainties, a number of the mining producers still believe that commodity prices may ease over 2017 – especially iron ore and coal. And at home, the $64 question is how will the east coast home building boom end? Clearly now is not the time for complacency.

Contributed by Craig James, Chief Economist, and Savanth Sebastian, Senior Economist

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I am married with three children (all in their 20s) and currently live in Huntleys Cove in the inner west of Sydney. Chief interest is athletics and trying to keeping up with the children.My current role is Chief Economist, Commonwealth Securities, interpreting big picture economic and financial trends for customers, clients and staff. Previously I was Chief Economist at Colonial and have worked at the Australian Financial Review as a senior writer.As well as providing presentations to staff and clients and commentaries on financial and economic trends, I appear regularly in the electronic and print media.I have worked in banking, finance and journalism for 38 years.I hold both Bachelor and Master degrees in Commerce (Economics). Both degrees were undertaken at University of NSW. I am an Adjunct Professor at Curtin Business School in Perth.

7 topics

1 stock mentioned

Craig James

Chief Economist

CommSec

I am married with three children (all in their 20s) and currently live in Huntleys Cove in the inner west of Sydney. Chief interest is athletics and trying to keeping up with the children.My current role is Chief Economist, Commonwealth...

Expertise

No areas of expertise

Craig James

Chief Economist

CommSec

I am married with three children (all in their 20s) and currently live in Huntleys Cove in the inner west of Sydney. Chief interest is athletics and trying to keeping up with the children.My current role is Chief Economist, Commonwealth...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment