Stocks and strategies for a stormy market

In a recent note the research team at Morgans outlined why they believe a cautious approach is warranted in the current reporting period. The broker highlighted four factors that suggest risks are likely skewed to the downside. These are 1) Factset consensus forecasts that show robust industrial earnings have been eroding 2) There is a dispersion of consensus earnings and dividend expectations that is wider than usual - reflecting lower corporate confidence; 3) market expectations for margin expansion look optimistic versus recent performance and 4) expanding payout ratios are potentially setting investors up for a painful reality check if companies under-deliver on dividends. With expectations subdued Livewire reached out to a selection of fund managers to see where they do and don't want to be invested in the current environment. Responses come from Katana Asset Management, Avoca Investment Management and The Montgomery Fund along with a great chart from Morgans.

The chart below highlights the recent performance of a selection of companies after they have issued an upgrade/downgrade. The market is delivering harsh treatment to those stocks that miss expectations.

[Screen Shot 2016-02-11 at 10.07.16 am.png]

Beware of stocks with lofty PEs

Jeremy Bendeich, Portfolio Manager, Avoca Investment Management

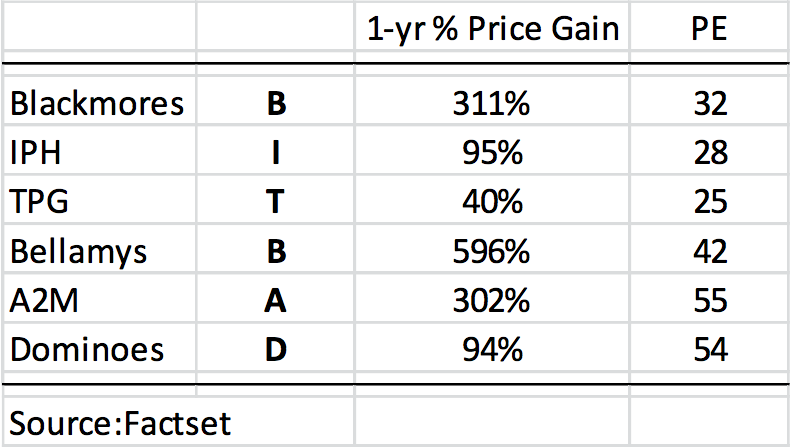

We are cautious about equities that have been the beneficiary of so-called momentum investing and whose PEs have excessively expanded relative to changes in their expected earnings growth. Recent underperformance of the so-called US FANG stocks (Facebook, Amazon, Netflix and Google) should be a worrying sign for momentum investors, of which we are not. Other instructive examples would be Linkedin and Tableau recently both falling over 40% on one day due to small earnings misses. We have composed our Aussie equivalent which we call a “BITBAD”. The table below highlights these names and their dizzying multiples. Clearly this group of stocks is particularly exposed to any small misses or global multiple retracement.

Look for quality, growth and price

Russell Muldoon, Portfolio Manager, Montgomery Investment Management

At Montgomery we have positioned our portfolios to benefit from anticipated strong market growth in sectors like Health Care, Telecommunications, Information Technology and niche Industrials. Strong underlying market growth does not mean that any company in these sectors is a worthwhile investment. We look for businesses with the right combination of quality earnings, bright prospects and attractive share prices. Our process has led to investments in companies like Sirtex Medical, CSL Limited, Resmed, Medibank Private, Vocus Telecommunications, Chorus Limited, REA Group, iSentia, Altium and Bursons Group. We feel these attributes are contributing to their share prices holding up well against the broader market, and from a portfolio perspective, delivering excellent returns to our investors.

Value investing is dead; momentum is king

Romano Sala Tenna, Portfolio Manager, Katana Asset Management

The overriding negative macro environment has indiscriminately impacted the larger end of the market. Individual stock fundamentals have been swamped by the wave of negative macro commentary. In such a period of top-down dislocation, investors invariably turn to emerging companies with a specific thematic that distinguishes that stock or stocks from the crowd. Value investing is dead; momentum is king. One clear thematic that investors have gravitated towards at present is the rise of the Chinese and Asian consumer. This has been characterised by stocks such as Blackmores, Bellamy’s, Capilano Honey, Bega Cheese and others. In our universe, we have attempted to capitalise on Asian demand through holdings such as Crown Resorts, Icar Asia and Seek Limited. In addition, the largest holding across both of our funds is BWX Limited. BWX is the manufacturer of the Sukin range of beauty and personal care products, which has recently attained the coveted #1 sales positon in the Australian market for ‘natural’ products. This has provided an excellent launching pad for a push into the Chinese ‘grey’ market and beyond

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

1 topic

19 stocks mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets