Sunset Strip > Trading Day Wrap From Blue Ocean 20170814

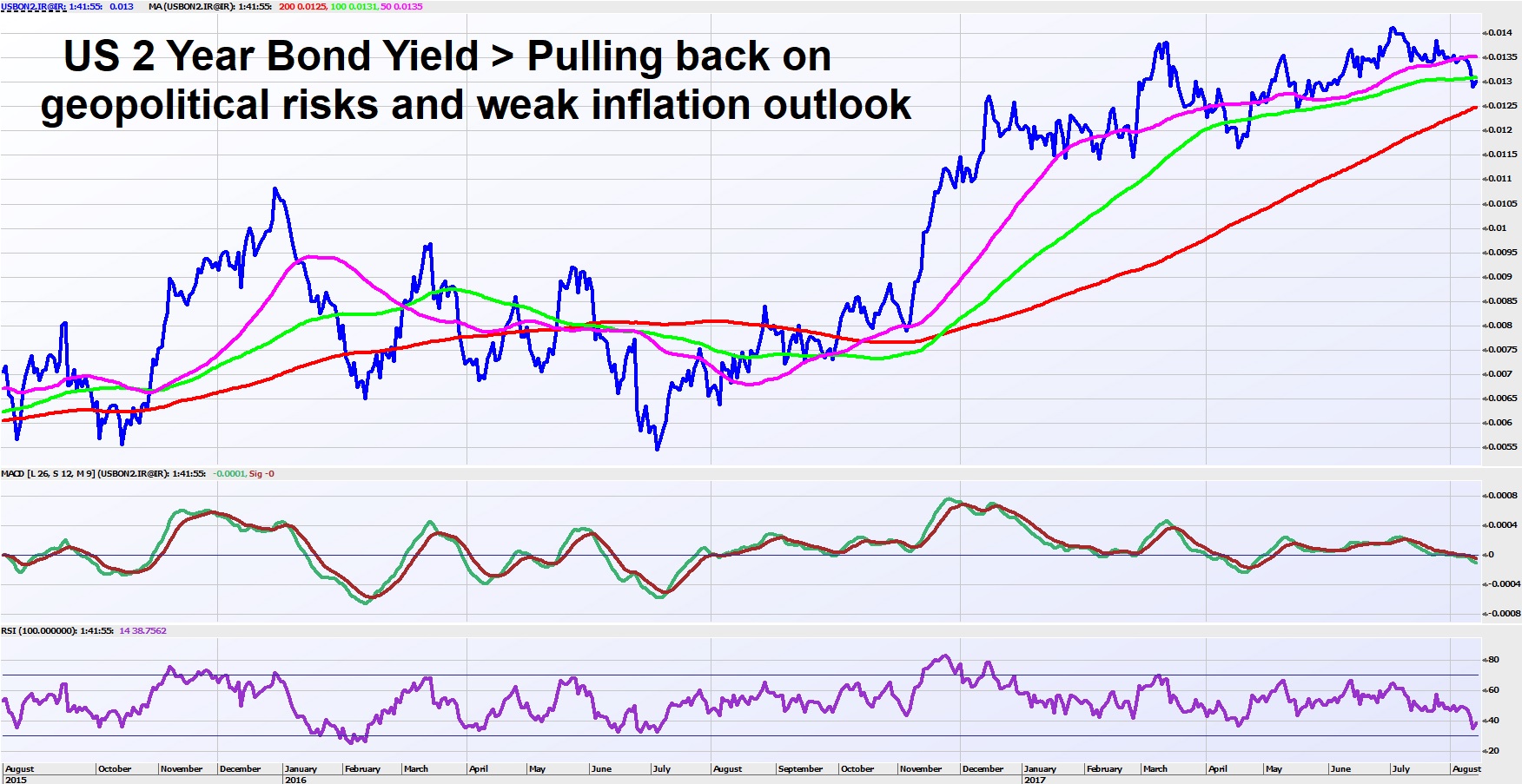

Local market had a relief rally as the “War of Tweets” between US and North Korea started to settle down. The weaker than expected US inflation outlook pushed down USD and pushed up AUDUSD. China data showed that we may be closer to the top in the recent commodity run in the short term as Chinese regulators act. Japanese growth data shows that the retail pick up is finally coming to support the sixth straight positive growth quarter. The market remains in very low sentiment and reporting season will continue to deliver big swings…stay nimble!!! We are expecting updates tomorrow from ANZ, CGF, CQR, DMP, FXL, GPT and PLG. The best performing sectors were IT, Banks and Energy while the worst performers were Gold, Utilities and Property.

Click here for the full report.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and CEO at Deep Data Analytics (www.deepdataanalytics.com.au) which is an integrated data analytics driven investment strategy service provider.

5 topics

11 stocks mentioned

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Comments

Comments

Sign In or Join Free to comment