Temptation is high but is the timing right?

Raf Choudhury

State Street Investment Management

The bear market bounce or relief rally continued through May but might be showing signs of losing momentum. The rally in April came after the initial shock of the coronavirus pandemic and deep and rapid plunge in global equities. Technical analysts will point to the fact that the market was in extreme oversold territory. Momentum behind the rally has built since, as markets have grasped hold of any positive COVID-19 related news that has emanated. Through May the good news continued to out weighted the bad. As the rally continues, investors are beginning to suffer from FOMO – fear of missing out. However, rather than succumbing to such urges, this might be the time when investors should hold their nerve and wait for clearer signs of a sustainable recovery.

At the start of the year we had cautioned that valuations were already stretched, and the double digit returns in 2018 had been driven by multiple expansion. For markets to continue to march forward we were looking for earnings to come through. Equity markets are not far from the levels they saw at the start of the year but with the impact of COVID-19, it is clear earnings support will be lacking, at least for the rest of 2020. Markets might be looking past this to longer term earnings but what is also sustaining the current rebound is, in part, the extreme levels of central bank support.

While the Fed is no longer buying Treasuries at the same rate as in late March, they are still there supporting financial markets. However the market rally which aligned with the FED’s increasing balance sheet has also tapered along with the rate of Fed purchases.

As a result we have an extremely fragile market where volatility, despite having fallen from extreme levels is likely to remain high and cautionary.

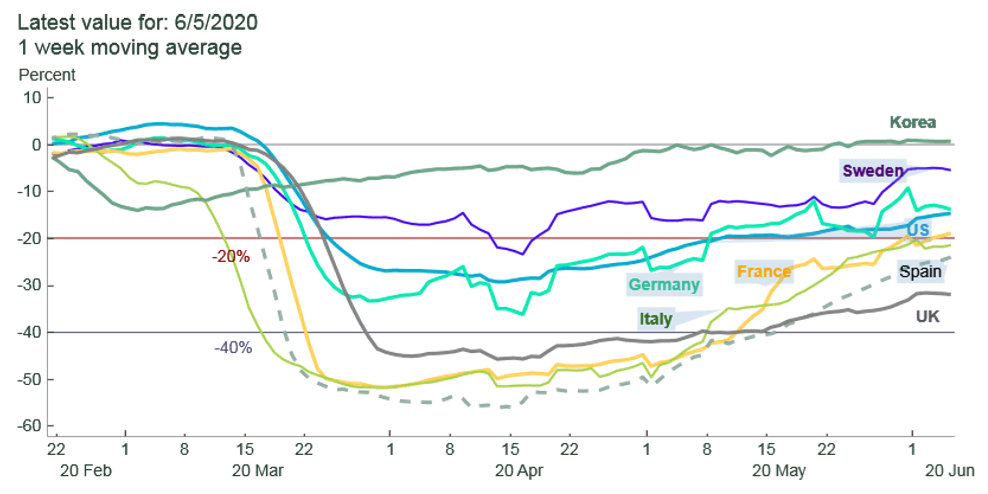

With economies slowly reopening there is positive news but there still remains a lot of uncertainty. Australia in particular has managed to contain the spread of the virus and social distancing measures have been taken on board and are proving to be effective. There are some positive signs in the US as well where certain states are also slowly reopening. Mobility trackers show the broad reopening across the globe, although at different rates.

Figure 1 - Google Mobility by Country (excluding Parks)

Percent vs. baseline, average. (Retail & Recreations, Residential, Transit Stations, Workplaces, Grocery & Pharmacy)

Source: Macrobond, State Street Global Advisors Economics, Google as at 10 June 2020.

While things are starting to look better, there are still a number of headwinds to overcome and implications to understand. The real extent of that damage will likely become understood in the next phase, beginning with the number and impact of actual bankruptcies. There is also the risk of a second wave of infections. Although we are better prepared now than we were in March, markets may reprice accordingly on the back of further outbreaks.

The key is to understand that volatility will remain high and uncertainty will continue which will create unpredictability in stock prices. While it might be tempting to see the rally and look to jump back in, holding off a little while longer might be a more prudent approach. Especially in the context of still elevated market levels and high volatility, meaning markets are exposed to a disproportionate amount of downside risk if the recent relief rally ends.

Every portfolio needs a solid foundation.

The evolving market backdrop creates plenty of opportunities and challenges for investors, and we believe that a multi-faceted and thoughtful approach is the key to generating successful investment returns. Stay up to date with my latest insights by clicking the follow button below. You can also watch our latest Fund in Focus presentation here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

........

Important Risk Disclosures

State Street Global Advisors, Australia, Limited (AFSL Number 238276, ABN 42 003 914 225) (“SSGA Australia”). Registered office: Level 17, 420 George Street, Sydney, NSW 2000, Australia · Telephone: +612 9240-7600 · Web: www.ssga.com.

The views expressed in this material are the views of Raf Choudhury through the period 20 June 2019 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

Investing involves risk including the risk of loss of principal.

All the index performance results referred to are provided exclusively for comparison purposes only. It should not be assumed that they represent the performance of any particular investment.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions. Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations. Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries.

This material is general information only and does not take into account your individual objectives, financial situation or needs and you should consider whether it is appropriate for you. Investing involves risk including the risk of loss of principal There is no representation or warranty as to the currency or accuracy of this material, and SSGA Australia shall have no liability for decisions based on such information.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA Australia’s express written consent.

© 2019 State Street Corporation — All Rights Reserved.

Tracking Code: 2605705.1.1.ANZ.RTL

Expiration Date: 30 September 2019

2 topics

Raf Choudhury

State Street Investment Management

Expertise

Raf Choudhury

State Street Investment Management

Expertise

Comments

Comments

Sign In or Join Free to comment