3 factors that keep AREITs performing

The AREIT sector returned 3.3% over 2018. Compared to Australian equities, down 3.1%, it was a respectable performance considering the wintry outlook predicted by some experts late last year.

The year-to-date figures add the gravy. AREITs have returned 6.6% year-to-date while equities have delivered 4.6%. But don’t read too much into short term performance. The real value of this reporting season is in the three factors that ensure the stocks in which we invest can continue to produce the cashflow to pay our investors their monthly distributions;

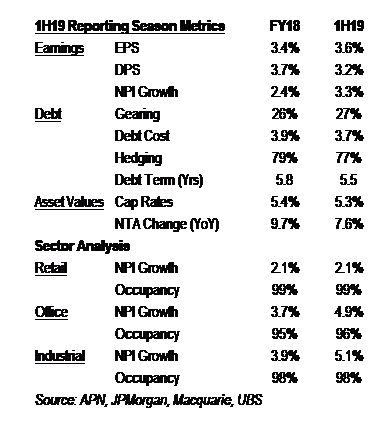

1. Earnings and distributions continuing to grow at sustainable rates. According to JPMorgan, earnings per share (EPS) is forecast to grow 3.6% (up from 3.3%) while FY19 distributions (DPS) are expected to grow by 3.2% (down from 3.8%). Both would be welcomed by investors, especially in a low growth environment with inflation around 2%.

2. Debt levels remain low: Gearing across the sector was 27%, 1% higher than at the FY18 result which was the lowest level since 1999 and well below the long term average of around 30%. AREITs are well positioned to deal with higher interest rates, should they eventuate, with average debt terms over 5.2 years. Debt diversification remains a key focus (less reliance on bank debt), as are debt terms, which comes at a cost but added security. These factors make our investment appreciably safer.

3. Asset values are rising: Net tangible asset values (NTA) were up 7.6%1 across the sector over the half. Industrial and office assets enjoyed larger increases while retail was generally positive.

Let’s now look at individual asset classes, starting with retail.

Retail weighs the barbell effect

To understand the performance variation in retail one must first understand the barbell effect. At one end are high quality super-regional and regional centres that dominate their catchments. These centres, like Chadstone owned by Vicinity (VCX) and Westfield Bondi Junction owned by Scentre Group (SCG), are destinations. At the other end are convenience centres close to home owned by landlords such as Charter Hall Retail (CQR) and SCA Property (SCP).

Both are good places to be. The top end enjoys higher occupancy rates and stronger sales growth whilst convenience centres have most of their rent sourced from supermarkets such as Coles, Woolworths and Aldi, offering a high degree of income security over a long term.

Stuck in the middle are High Street shops (thankfully not owned by any AREITs) and sub-regional centres that lack the accessibility of your local centres and the product range and experiences of destination centres. The High Street and sub-regional centres are more at risk, exposed to cannibalisation from each end of the barbell and online retail.

The key for landlords is to position their assets to capture changing consumer spending patterns. In well managed destination centres there are more food, services and experiential retailing options. These attract foot traffic and are replacing low rent paying department stores and apparel which is more susceptible to online. Convenience centres, meanwhile, must focus on being just that and shoppers will continue their regular visits.

Reporting season offered further evidence of the barbell effect, providing support to APN’s decision to focus on AREITs with most of their assets at either end of the retail barbell. Nevertheless, subdued wages growth and falling house prices remain a major headwind for consumers with the upcoming election providing further uncertainty. Cyclical problems remain but the right types of retail assets can continue to provide APN investors the security and stability of distributions they have become accustomed to over the past decade.

Office just keeps on keeping on

With near record low vacancy rates in Sydney (4.1%) and Melbourne (3.7%) it can’t get much better for office landlords. With the negotiation table tilted significantly in their favour, landlords have been able to continue growing rents (and net property income) at rates far above long term averages.

New supply is on the horizon for Melbourne this year and Sydney the year after, but this is unlikely to rupture the favourable market trends. There is every chance above trend rental growth will continue.

Income growth of 4.9% for the rolling year (up from 3.7%) highlights how strong these key markets have become. Tenants facing the prospect of renewing their lease are in for a shock. Market rents are now 35% to 40% higher in Melbourne and Sydney than when they last signed their lease. Even a fixed review of 3% a year over the past five years would entail a 20%+ increase when renewed. Tenants don’t have much choice. With 4% vacancy rates in key markets, tenants can either pay up or move out. Most are paying up.

Industrial

If you thought things were hot in the office market, you ain’t seen nothing yet. The industrial sector was the top performer returning 11.9% over the six months to December 2018 or 29.0% over calendar year 2018, driven largely by Goodman (GMG), now the largest AREIT in Australia.

That moniker is misleading. Goodman is a real estate operating company and carries all of the associated risks. How it continues to be classified as an AREIT is beyond us, but there it is. AREIT returns should be less racy than this. The fact that they’re not means many conservative, income-focused investors may be taking on risks they are not aware of.

Across the sector improving supply chain management is leading to a growing sophistication, fuelled by omni-channel retail operators that combine online sales and quick delivery times with real world experiential retailing. This has added a mystique to what was once a bland, unappealing sector.

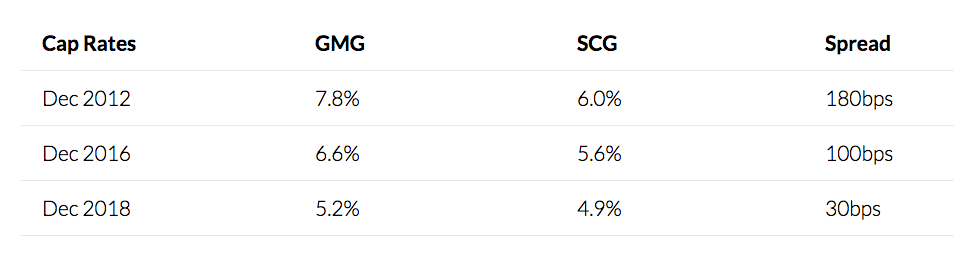

While there is much to like about the industrial asset class or more specifically logistics and distribution centres it is riding an unsustainable wave of growth and asset price appreciation which we are increasingly concerned about. Industrial asset valuations have converged markedly with retail over recent years to levels never before seen. The following table highlights this trend indicated by the narrowing spread between Goodman and Scentre’s cap rates over the past six years.

Goodman’s share price and the demand for industrial assets in Australia indicates this convergence trend has further to run. This would be a new paradigm for the Australian real estate hierarchy.

While we debate this issue constantly, a real concern for us is the level of optimism around the industrial sector and specifically Goodman which returned a jaw dropping 60.4% over the year to February 2019. While the AREIT sector returned an impressive 18.9% over the same period, this was a staggering 41.5% behind Goodman’s return. The means around 40% of index return was from a stock that represents 17.5% of the index.

The last time I can recall a spread of this magnitude was in 2006. Back then Goodman (then Macquarie Goodman) returned 66.8% for the year while the AREIT Index returned 34.2%, a spread of 32.6%. Great returns while you can get them but clearly not sustainable over the long term. You only need to look back to what happened in 2008 when Goodman fell 81.5% to recognise why we are concerned.

What else?

Over 2018 small cap REITs raised $1.1b in equity, highlighting support of Trusts where APN is often nicely positioned. One deal we particularly liked was Shopping Centres Australia’s (SCP) acquisition of 10 assets from Vicinity Centres (VCX) for $573m. It was a good arrangement for both parties, delivering capital to VCX to finance its development pipeline and scale to SCP’s existing portfolio of assets which it will manage well at a discount to valuation.

We wrote about Blackstone’s offer for Investa Office (IOF) in June last year. We felt the offer was too low and told anyone that would listen why. It paid off. Oxford Properties won the prize fight at a knockout price of $5.60. This was a highlight for APN and a great return for our investors, showing the value of a good argument strongly made.

All up, the AREIT sector remains in good shape. Providing investors with secure income and managing risk remains the key focus for most AREIT management teams, attributes that have recently become the flavour of the month. The resulting surge in AREIT share prices is being driven by investors seeking shelter from uncertainty but does little to change the operating outlook for the AREITs and the income they provide.

That’s a general theme across the sector. Yields are attractive and the cashflow that supports them is stable and growing at a sustainable rate. But investors’ interests are best served by not getting carried away.

Never miss an update

Stay up to date with the insights from the real estate expert team at APN Group by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to find out how to invest in website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Pete joined Dexus Real Estate Securities in 2006 and is responsible for the management of the suite of real estate securities funds. With more than 19 years of experience in financial markets, Pete brings a unique knowledge set, completing Masters-level academic research papers on both commercial real estate cycles and global property securities.

1 topic

5 stocks mentioned

Pete joined Dexus Real Estate Securities in 2006 and is responsible for the management of the suite of real estate securities funds. With more than 19 years of experience in financial markets, Pete brings a unique knowledge set, completing...

Expertise

Pete joined Dexus Real Estate Securities in 2006 and is responsible for the management of the suite of real estate securities funds. With more than 19 years of experience in financial markets, Pete brings a unique knowledge set, completing...

Expertise

Comments

Comments

Sign In or Join Free to comment