The ‘go too’ stocks hit hardest today (CCP, APT, NSR)

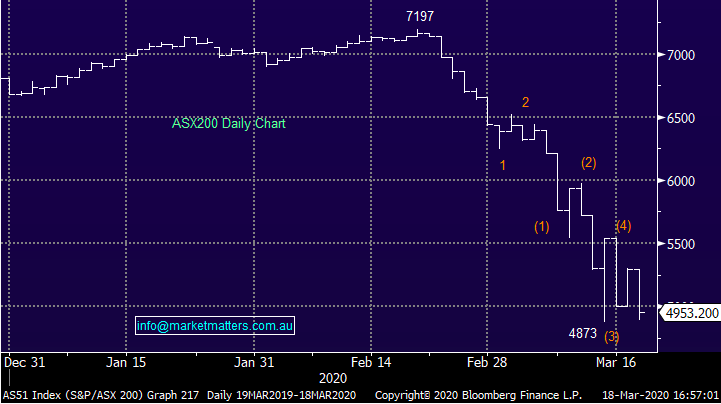

After a day in the green yesterday where the index put on nearly ~6% we were back in sell mode today and aggressively so, the market giving back those gains and some to end down 6.43%, back below 5000pts. Despite strength in US markets overnight and a flat open priced in by our futures, our market opened on the back foot and the selling just fed on itself before a volatile close played out, the index rallying more than +150pts before the match, then fell back by more than 100pts in 10mins, its just extreme volatility, no other way to explain it.

The market made a new closing low today at 4953 just a few ticks above the intra-session low about a week ago. We’ve seen decent support around this 4900 region when tested and we’re back knocking on the door of that level again, debt / and or access to credit a dirty things at the moment as credit markets seize up. I was asked today by a very good client of mine what we need to look for before going all out in the market and the corporate bond markets are clearly the key. Credit spreads need to calm, buyers need to gain confidence and for that to happen there needs to be some sort of circuit breaker. What then is the simplest way of monitoring this theme I was asked?

NBI is a listed investment trust investing in high yield bonds, skewed globally but weighed more towards US debt markets. They publish a daily NTA which can been seen through the ASX – its released around 3.30pm each afternoon. At issue price, NTA of NBI was $2.00, today NTA was $1.71, yesterday was the same, on Friday last week it was $1.79, Thursday was $1.80 etc, you get the gist. An easy way to monitor corporate bonds is to watch the NTA of NBI, and look for the worm to turn.

At the sector level today, IT stocks hit hard, Energy remained under pressure while the real-estate companies were again sold into, now the bulk trading below NTA after trading a long way above NTA for an extended period.

Asian markets were better than our own today, Japan down -1.68% while Chinese stocks were off just 0.60%.

Overall, the ASX 200 fell -340pts / -6.43% today to close at 4953 - Dow Futures are trading down -821pts/-3.93%.

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE:

Go Too Stocks Hammered: Today there was a clear move out of the ‘go too’ names on the ASX, the route was led by Afterpay which was savagely sold off today down 34% to the point where it was forced into a regulatory trading halt late in the session to ease some of the pain. Alternative financing plays across the market were all under pressure today but none more so than APT.

Concerns are rising that BNPL players will see significant increases in defaults which will see these companies roll over as well. The target market for much of this debt is part time & casual employed people, those most at risk of losing jobs and as result, not paying debts back. On the other side of the scales, transaction volumes are likely to take a hit as people tighten the belt, while access to credit will also tighten.

Elsewhere, in the payments space, EML Payments (EML) was hit another 23% with its shares trading from a recent high around $5.60 to todays close at $1.54, while IDP Education (IEL) fell by 16% although it was down more early.

AfterPay Touch (APT) Chart

Credit Corp (CCP) -20.68%: The stock peaked on 21st February at ~$38 and closed today $12.31. A few things at play here however the main issue is debt / balance sheet strength. The stocks that have been most heavily sold are those that carry higher debt and CCP fits that bill. At last reporting date in January they had net debt of $206m with gearing of 30%, however they have a covenant in their lending arrangements which says that they need to keep gearing at less than 60% of financial asset carrying value. The takeaway here is that this is a leveraged business where debt is higher than we’d like and the value of the assets underpinning that debt has likely declined.

Collection House (CLH) is one of their competitors and in mid-February they were suspended from trade with an alarming announcement. In short they effectively said that collection practices were too aggressive and need to be changed,. The change would result in lower earnings from their purchased debt ledgers (PDLs) and that in turn would reduce the value of the PDLs on their balance sheet. That move seems to have triggered an issue with senior lenders. In short we think CLH is in a world of trouble and that has focussed attention on CCP.

While CCP is a higher quality business than CLH, it seems clear that traditional debt collection practices are under the microscope and this could have a negative impact on the value of their inventory (which is essentially purchased debt). If the carrying value of inventory changes it puts pressure on the balance sheet at a time when the market is very focussed (and rightly so) in financial strength rather than growth.

I can also remember CCP during the GCF, it traded down to ~60c and very nearly went out the back door. We have no interest.

Credit Corp (CCP) Chart

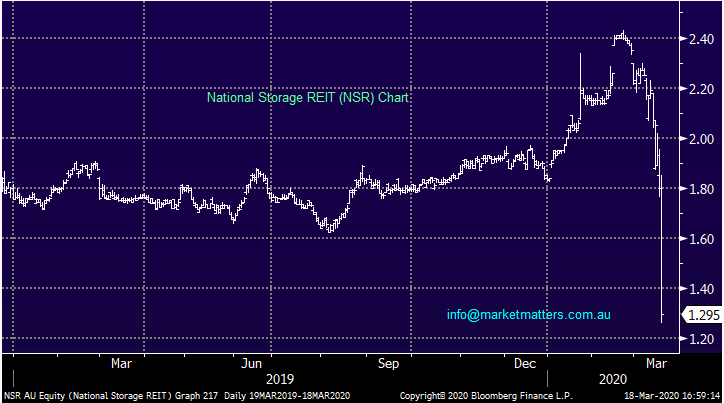

National Storage REIT (NSR) -28.06%: a big move for what most would consider a safe asset – NSR saw the takeover bid from Public Storage pulled today as a result of the virus uncertainty. The bid at $2.40/share was around 35% premium to NTA at the half year result not long ago. It seemed the market had caught a whiff of the news with the stock sharply lower from mid-morning before entering a trading half ahead of the announcement. The deal will be one of many to fall over before the corona scare passes - Caltex (CTX) will be nervous EG & Couche-Tard walk from the table. NSR though presents some good value at current levels, trading well below NTA with little near term debt maturity and a reasonable ~40% gearing.

National Storage (NSR) Chart

BROKER MOVES:

- Premier Investments Raised to Buy at Citi; PT A$14.90

- JB Hi-Fi Raised to Neutral at Citi; PT A$31.20

- Flight Centre Raised to Buy at Citi; PT A$22.70

- City Chic Collective Ltd Raised to Buy at Citi; PT A$2.50

- Regis Resources Raised to Outperform at Macquarie; PT A$3.60

- Resolute Mining Raised to Outperform at Macquarie

- Qantas Raised to Buy at Citi; PT A$3.70

- Coca-Cola Amatil Raised to Neutral at UBS; PT A$10

- Technology One Raised to Neutral at UBS; PT A$7.25

- Pro Medicus Raised to Buy at UBS; PT A$29.30

- Altium Raised to Buy at UBS; PT A$37.50

- St Barbara Raised to Outperform at Macquarie; PT A$2

- OceanaGold GDRs Raised to Outperform at Macquarie; PT A$3

- Newcrest Raised to Neutral at Macquarie; PT A$22

- FlexiGroup Cut to Neutral at Macquarie; PT A$1

- Evolution Raised to Outperform at Macquarie; PT A$3.80

- SCA Property Raised to Buy at Jefferies; PT A$2.65

- Kogan Raised to Outperform at RBC; PT A$5

- Medibank Private Cut to Hold at Morningstar

- Metcash Cut to Sell at Morningstar

- Transurban Raised to Buy at Morningstar

- Blackmores Cut to Hold at Morningstar

- ALS Raised to Hold at Morningstar

- GPT Group Raised to Buy at Morningstar

- Pendal Group Raised to Positive at Evans & Partners Pty Ltd

- Austal Raised to Buy at Goldman; PT A$3.73

- James Hardie GDRs Raised to Sector Perform at RBC; PT A$23

- South32 Raised to Buy at Renaissance Capital; PT A$3.02

- Worley Cut to Neutral at JPMorgan; PT A$8.30

- Woodside Cut to Neutral at JPMorgan; PT A$24

- Oil Search Cut to Neutral at JPMorgan; PT A$3.65

- Carnarvon Cut to Neutral at JPMorgan; PT 39 Australian cents

- Beach Energy Raised to Overweight at JPMorgan; PT A$2.15

- Crown Resorts Raised to Outperform at Credit Suisse; PT A$11

- IOOF Holdings Raised to Hold at Bell Potter; PT A$3.25

Get regular market updates

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking the 'CONTACT' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

........

Any advice provided is of a general nature only.

1 topic

3 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment