Trade war rhetoric overshadows deeper problems for Emerging Markets

We have passed the sweet spot in this business cycle, where easy monetary conditions and synchronised growth pushed share markets higher. We are transitioning into a more challenging phase, as China and Emerging Markets (EM) decouple and we are left with a US economy at risk of overheating.

Monetary conditions that have been easy for far too long are now tightening, pushing the US dollar higher. This is impacting activity not just in the US, but also in EM that have borrowed in dollars. Finally, globalisation, a key source of growth for decades is now threatened, as trade wars ensue between the world’s largest economies.

Credit and trade have for decades grown well in excess of GDP, fuelling global commerce. Indebtedness in many of the world’s largest economies has risen to unsustainable levels and can no long bolster growth the way it has in the past. Just consider Australian household debt, amongst the highest in the world relative to the income required to service it.

Excess liquidity has found its way into Emerging Economies, with cross border US dollar debt doubling to $7 trillion since the crisis. The stronger dollar and rising US interest rates together act as a tourniquet on world liquidity and for those countries that have borrowed in dollars.

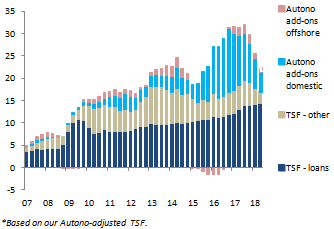

Authorities in China have also restricted credit growth as they try and clean up over-levered companies and contain excesses that have built up in the shadow banking system. In fig 1 you can see credit growth has fallen back to 2013-14 levels. Given the extent of tightening, not dissimilar to what proceeded the downturn in 2015, we would expect to see activity in China decelerate further in the short to medium term.

Fig 1: New Credit is slowing sharply in China as credit tightening measures bite.

Source: Autonomous Research

Liquidity has tightened acutely in some sectors with credit spreads and default rates rising. The Renminbi has also tumbled, which was a harbinger of trouble ahead when the Chinese economy slowed in 2014.

While investment spending and export volumes have been weak in recent months, the rest of the Chinese economy has proven remarkably resilient. As this crackdown on shadow credit continues, the Chinese economy will likely decelerate further. This is where the trade dispute with the US becomes interesting - the traded goods sector is far larger in China than the US and with the Americans threatening tariffs on a further $US 200 billion of imported Chinese goods, while facing a slowing economy, the Chinese are in a difficult position. If share markets are the scoreboard for this trade war, the Americans are clearly in front and under no pressure to back down any time soon.

If you cast your mind back to 2014, the primary concern of investors was a slowing Chinese economy. The global industrial supply chain slowed through 2015 as the industrial economy slipped into recession. The Renminbi came under intense pressure and EM shares collapsed (Fig 2). Having initiated this downturn, China led the global recovery in industrial production that commenced back in early 2016.

Fig 2: Emerging Market Shares and the Renminbi are indicating the cycle may have turned

Source: Bloomberg

The extent of recent losses in EM shares and debt securities is troubling, the cycle looks to have turned. Meanwhile, share markets in most major economies are testing all-time highs, ignoring this important development. This seems incongruous and is a major risk given EM contribute most of the world’s growth.

The trade dispute is not the real problem. After a pause, US interest rates and the US dollar are likely to push higher, ensuring any relief rally in EM from an easing in trade tensions may be short lived.

This has important ramifications for the Australian share market also. The Australian share market is considered a defensive part of the Asian basket and has rallied as EM indexes have collapsed. The Australian banks, not forsaking their challenges with the Royal Commission and the poor profit outlook are considered a safe harbour in an Asian storm.

Mining shares and the mining economy are of course highly levered to commodity prices and Chinese demand. You wouldn’t know it though with BHP Billiton’s shares reaching a cycle high. Again, investors in mining shares are attributing the weakness in commodities to the trade dispute, when instead they should be focussing on the outlook for EM growth which accounts for all the growth in demand for commodities.

As for the rest of the Australian share market, industrial shares (Ex-Banks and REITs) continue to re-rate higher, becoming more expensive, while profit forecasts are trimmed further Fig #. At 20 times forecast earnings (blue line) we are paying a very high price for modest profit growth.

Fig 3: ASX 200 Industrial Companies (Ex Banks and REIT’s)

Source: Bloomberg

Take CSL Limited as an example, the largest non-bank industrial company in this group, which we will discuss at length later in this report. While CSL is a fine company and is very well managed, investors should not forget it is a ‘growth cyclical’ benefiting from highly favourable trading conditions. The plasma business goes through deep cycles- the good times won’t last forever.

There are some important challenges ahead also for CSL, as new technologies using gene therapy and recombinant antibodies target some of CSL’s key indications. We recently sold our remaining CSL shares, as we simply cannot justify the share price, even under the most bullish of scenarios.

Investors are abandoning value and instead are chasing earnings revisions as the market keeps rewarding growth and momentum. This can only go on for so long before it ends badly. The ultimate risk in holding any asset is in the price you pay, and this market is red hot.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

We are active, high conviction investors in Australian shares. As an absolute return manager, Watermark offers a proven alternative to traditional institutional funds.

3 topics

We are active, high conviction investors in Australian shares. As an absolute return manager, Watermark offers a proven alternative to traditional institutional funds.

Expertise

We are active, high conviction investors in Australian shares. As an absolute return manager, Watermark offers a proven alternative to traditional institutional funds.

Expertise

Comments

Comments

Sign In or Join Free to comment