Another way to play Sydney Airport

Elizabeth Moran

Elizabeth Moran Consulting

Attention Sydney Airport bondholders, with the 2030s selling at a premium, it may be time to switch to the 2020 inflation-linked bond for great relative value. You don't have to hold bonds to maturity, investors prepared to trade can earn higher returns. This note tells the story.

Sydney Airport has long been a share market darling, for good reason. It operates the busiest airport in Australia with a long-term lease over monopoly infrastructure assets, coupled with consistent growth over many years.

Few realise that the airport has issued two Australian dollar denominated bonds that provide a different, protective function that is well worth investigating. In recent months, the trading between the two bonds gives great insight into the psyche of bond investors.

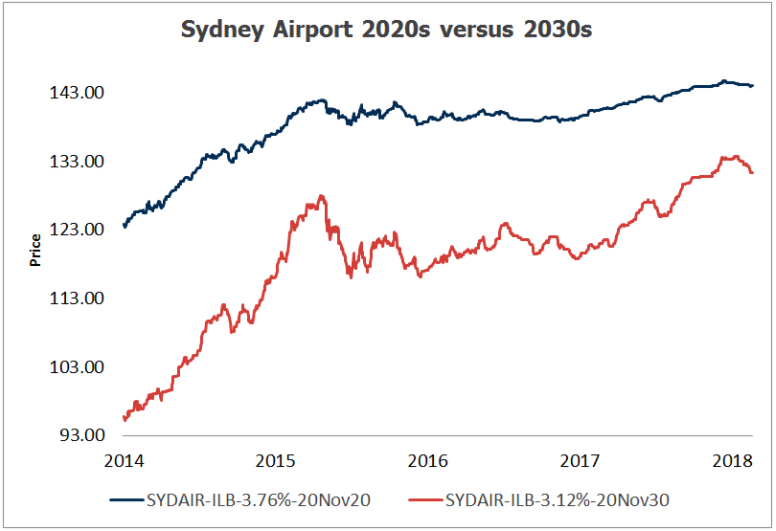

Sydney Airport 2020s versus 2030s: which is the standout?

Back in 2004 and 2006 Sydney Airport issued inflation-linked bonds that mature in 2020 and 2030 respectively.

The 2020 bond was issued at a yield of Consumer Price Index (CPI) + 3.76 per cent per annum and the 2030 bond at CPI + 3.12 per cent per annum.

Source: FIIG Securities

As much of the airport’s income is tied to inflation, think car parking and retail leases, the company issued debt linked to inflation, to minimise the differences between future income and expenses.

The bond issues also provided the company with long-term funding certainty of 16 and 24 years – it’s hard to get that sort of commitment from a bank!

For investors, inflation-linked bonds are the only direct hedge against inflation and for that reason a key, ongoing recommended holding.

Inflation-linked bonds in a low inflation environment

Just last year, persistent low inflation, below the RBA target of 2 to 3 per cent per annum, prompted many to sell-down their Sydney Airport bond holdings pushing bond prices lower. Then the market got interesting.

Prices of other similarly rated fixed and floating rate corporate bonds offered lower projected returns and the two Sydney Airport bonds looked like great relative value – they still are but I’ll circle back on that point.

Investors piled back in. The 2020 bond was thought too short to provide inflation protection and the 2030 bond attractive as it was trading at about $123, a discount to its underlying face value. Investors that reasoned the discount would be eroded over time saw an opportunity for a higher than expected return.

In circa seven months, the discount eroded, the price rose and investors made money. Currently, the 2030 bond is trading at $133, a premium to its underlying face value. So, less attractive to the bond investor with an eye to trading, perhaps time to sell and look for opportunities elsewhere.

Investors didn’t need to look far, just back to the good old Sydney Airport 2020 inflation-linked bond, which is now in demand. Again it looks like great relative value.

The 2020 bond’s current yield is CPI + 2.54 per cent. The fixed quarterly coupon of 2.54 per cent is close to term deposit rates, but investors also get capital appreciation of CPI.

Last December’s 1.9 per cent headline annual inflation figure, if steady over the next couple of years would result in investors earning circa 4.44 per cent per annum for a low risk investment grade asset.

To put the yield into context, consider two other bonds that are considered to be similar risk both maturing within a month of the Sydney Airport 2020 bond – a floating rate bond from ME Bank, with an expected yield of 3.16 per cent per annum and a fixed rate bond from Global Switch with a 3.32 per cent yield.

The 2020 Sydney Airport inflation-linked bond looks a stand-out.

Read on for further insights

Are you ready to find out how you can earn over 5% pa* with corporate bonds? Click here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

3 topics

1 stock mentioned

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment