Valuations are creating endless opportunities

In the past quarter, we have seen a significant divergence between the performance of the US stock market compared to emerging markets and Europe. Donald Trump’s hard stance on tariffs and his trade wars have driven fear into emerging markets, especially China. Weakening manufacturing numbers in Europe, a populist five Star movement – legal coalition in Italy and Brexit negotiations have raised cause for concern in Europe. Further, falling automotive sales have also driven worries about a macroeconomic slowdown globally.

This has created a stark divergence in the performance of equity markets as the US market has continued to rise, driven by the concentration of the market in large capitalisation technology stocks like Apple (NASDQ:AAPL) and Amazon (NASDAQ:AMZN), where incessant inflows are pushing up valuations.

In emerging markets and Europe however we are seeing outflows driving markets lower, and with them, valuations. Despite this, there has not been much of a change in the fundamentals and earnings in these regions and respective industry sectors.

While our skew to Asia and Europe has not kept up with the global index this quarter, we are comfortable with the fundamentals and confident in the earnings trajectory of the companies we have invested in.

In the short term, stock prices simply reflect sentiment as the stock market is a voting machine, rather than a true reflection of fundamental value for the asset you are buying.

Valuations in each geography are moving in different directions and we are excited about the opportunities that we are presented with today. I couldn’t have said this at the start of this year.

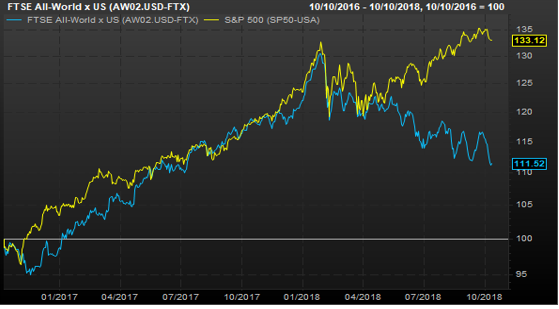

Global indices diverging

Source: FactSet

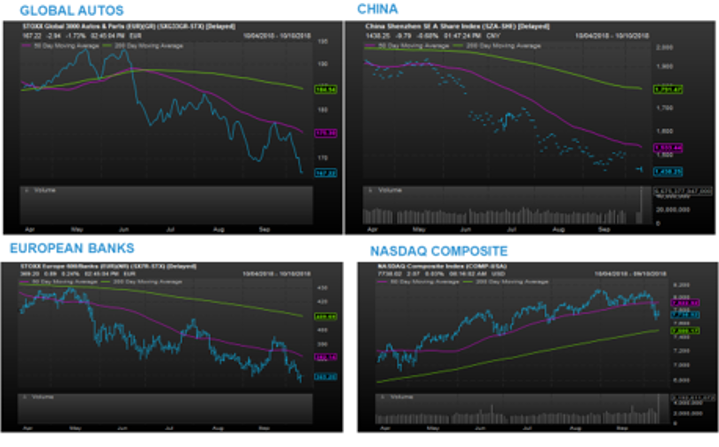

As can be seen in the charts below, while the Nasdaq has continued its steady appreciation over the past six months, pushing Apple up to a PE of 19x, well above historical averages, China, autos and European banks have traded down together, down around 25%, as panic sets in around global trade. As I write this, the US market has just this week had a large one-day correction, so we will see whether things normalise from here.

Macro fears causing sell offs in certain sectors

Source: FactSet

As contrarian value investors, this is the type of market that we get excited about as it throws up intriguing long-term opportunities for the brave. While the International Monetary Fund downgraded their global growth forecasts for 2019 from 3.9% to 3.7%, this is actually a marginal decrease in projected growth. You would think that China and emerging markets are entering a recession by the way the stock prices have reacted in the past three months, but the IMF only downgraded their forecasts for Chinese gross domestic product (GDP) growth in 2019 by 20 basis points to 6.2%. While the trade tariffs are expected to impact Chinese GDP growth by 1.5%, domestic policy stimulus is expected to offset a large part of this impact. If you think about the tariff impact, Chinese exports represent 18% of GDP and China’s exports to the US represent 19% of this figure. So while the impact is not trivial, it is manageable.

China’s exports in September actually accelerated from 9.8% YoY growth in August to 14.5% growth in September. The Yuan has depreciated by 11% since March against the US dollar. This is not insignificant and enables Chinese exporters to offset some of the impact of the trade tariffs. President Xi Jinping and the Chinese government are using the currency as part of this trade war. It is no surprise that Steven Mnuchin, the US treasury secretary, has recently stated “We are going to absolutely want to make sure that as part of any trade understanding we come to that currency has to be part of that.”

Interestingly, US GDP growth is expected to decelerate from 2.9% this year to 2.5% in 2019. Tariffs actually causes inflation and with US unemployment at 3.8%, the only option that the Federal Reserve has is to increase interest rates and remove liquidity from the system.

At the moment we have been increasing our positions in Asia as we haven’t seen these sorts of valuations for quality companies in quite some time.

We are still holding a decent amount of cash in the portfolio due to rising rates in the US.

Trade Wars - Why are they occurring?

I was recently at the Alibaba investor day in Hangzhou and Jack Ma gave a speech about why he was stepping down as Chairman. He said that the US has a history of going after an emerging superpower and did the same thing when Japan became the second largest economy in the world in the late 1970s. China surpassed the size of Japan’s economy in 2010 and will rival the US over the next few decades. Jack Ma believes that this trade conflict may continue for the next twenty years.

Xi Jinping wants to “make China great again”. He has stated that by 2025 he wants China to dominate its domestic markets in 10 major new technologies including driver-less cars, artificial intelligence and quantum computing. In 2035, he wants China to be the dominant force in technology and innovation everywhere.

Donald Trump is accusing China of stealing their intellectual property and this is part of the basis behind the trade war. The US don’t want to cede to China the dominant position in the world and China wants to keep growing and make China greater. These two ambitions might not be mutually exclusive and if so the Chinese and US can come to an agreement. However I don’t think Donald Trump wants to come to an agreement until the mid-term elections as he is using this strong stance to get votes and fuel the xenophobic vote that got him elected.

How are we positioned for the current market environment?

As fundamentally driven investors, we look to take advantage of market fear to buy into quality, growing businesses at value prices. We increased our cash position to 15% and in the past few days have been deploying some of this cash as the US has finally started falling with the rest of the world.

Over the past year we have been reducing our exposure to US domiciled earnings and increasing our exposure to more attractively priced, quality stocks around the world. While the recent sell off in global markets outside of the US is causing some transitional indigestion, we are really excited about the opportunities that we are buying today. Having travelled through China for a week and the US for another week, visiting four cities in each country, I am more excited about the opportunities for growth in the companies that we own.

More importantly the valuation opportunities that we are seeing today outside of the US feels like the opportunities we saw during the global financial crisis in 2009 and the more recent fears around Brexit in 2016.

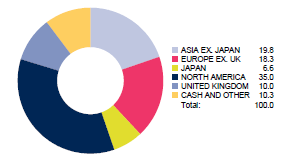

Portfolio regions

Source: Perpetual

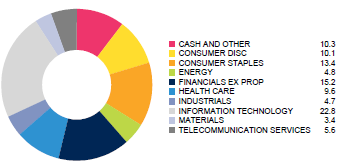

Portfolio sectors

Source: Perpetual

Where is the value in Technology?

We have taken the view that the US and China both have leading technology businesses and have been happy owners of Alphabet (NASDAQ:GOOG) and eBay (NASDAQ:EBAY) since inception of the global share fund in 2011. We also bought into Alibaba at the IPO in 2014 (having sold out soon after on valuation grounds but recently have bought back in) and have also recently bought back into Baidu.

We have been increasing our exposure to Asia as valuations have been falling. The region has globally leading businesses with strong balance sheets. This is what the US and Donald Trump are afraid of. The reality is that the strongest and most innovative survive in global capitalism. China is actually more advanced than the US in terms of e-commerce with 18% of retail sales being online versus only 14% in the US. Alibaba is a leader in ecommerce and is one step ahead of the US leader, Amazon, in payments.

When we look at Amazon and Alibaba we see a lot of similarities in terms of their businesses and new ventures. Amazon represents 5% of all retail spend in the US and 49% of all online retail spend with about 350m active customers. Its sales are growing at around 30% this year but are expected to slow down a bit to 20% next year. Their earnings growth is much quicker than this as operating leverage will double their EBIT margin from 2.3% to 4.7% this year. While they started off with books, they continue to expand their product categories. While consumer electronics and technology are their leading product categories, they are expanding into areas like fresh food with the whole foods acquisition and are growing in personal care and beauty. Some of Amazon’s greatest feats have been to build businesses from scratch which is a testament to Jim Bezos.

Amazon web services provides cloud services to large corporates like Verizon and Fox as well as thousands of SMEs. They are investing in artificial intelligence (AI) and are building out Amazon echo and Alexa’s capabilities. Aside from having featured heavily on the most recent series of 'The Block' as an integral part of the contestants' luxury apartments. Alexa as a personal assistant has been evolving to move calendar meetings via voice as well as answer questions. Alexa has also been launched into the hospitality industry allowing guests to use it as a concierge as well as for in room services. While Amazon is developing some wonderful assets and earnings streams, its valuation has reached 1 trillion and trades on a price to earnings ratio (PE) of 100x. As value investors, we can’t stomach paying such a valuation.

On the other hand, Alibaba has fallen to a valuation that we see as extremely attractive, trading on a PE of 20x one year forward, with investments in areas like cloud and video streaming that are loss making today but will create significant value going forward. Jack Ma has taken Jim Bezos’ playbook and rolled it out into China. Alibaba has 58% of total retail ecommerce in China. Its revenue is growing at 60% and its monthly active user base across Tmall and Taobao is at 634 million. It is more of a market place and has two leading platforms – Taobao which is its consumer to consumer platform and Tmall, its business to consumer platform. It is spreading its tentacles similarly to Amazon. Alicloud dominates China’s cloud services and it has 50% share in Infrastructure as a service. It has also been acquiring bricks and mortar retailers and investing in expanding its fresh food offering with its Ele.me online food delivery business and Hema, their supermarket offering. They have also been investing in AI with Tmall Genie, their voice assistant.

Alipay is one of their undervalued assets. It has 870 million annual active users. While I was traveling through China with my colleague Thomas, it became evident that credit cards weren’t used anymore in China. Consumers are using Alipay and We-chat pay for payments online and offline and to transfer money between friends rather than using credit or debit cards. Alibaba is looking to roll out technology to convenience stores around China, whereby you scan your Alipay wallet as you enter the store and then you pick up the items that you want and walk straight out without having to go to a cashier. It automatically debits your account as you walk out. While the rest of the world is using a mix of Paypal, credit cards, Stripe, Square and Venmo for online payments, Alipay and Wechat pay are dominating the entire ecosystem in China. Alipay is looking to expand outside of China as Alibaba is.

We think the valuation and earnings growth potential makes it a much more attractive investment than Amazon.

We also own an indirect stake in Alibaba through our investment in Softbank, which effectively gives us exposure to Alibaba at a 30% discount.

I don’t have time to go through our thesis on Baidu here, but let me just say that it feels like when we invested in Google seven years ago, when you had a leading search engine growing at double digits, building out other businesses that weren’t being valued by the market. At that stage Youtube wasn’t really earning much and they were still building out their other bets. Baidu controls Iqiyi which has over 400m monthly active viewers and is expected to breakeven next year. It is also investing heavily in artificial intelligence and their driverless car platform, Apollo. These businesses are a 15% drag on earnings but we think will become very valuable. Once you give these businesses a value and strip out their stake in Ctrip, the Baidu search engine is trading below a PE of 15x today.

Conclusion: Volatility brings opportunity

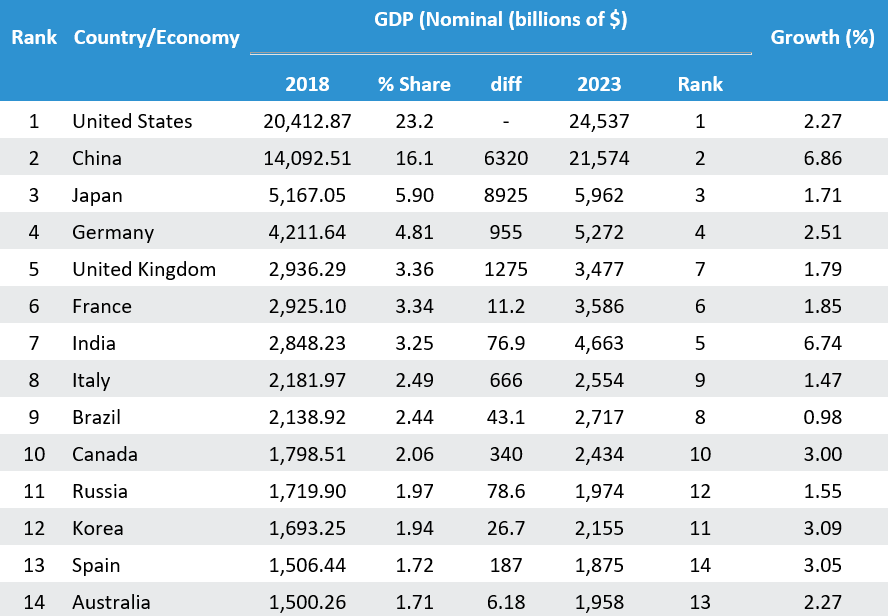

As I write this, the US market has had a short, sharp 5% correction and the volatility index has spiked up. Our portfolio is much lower beta than the index and we are carrying a decent amount of cash to take advantage of opportunities. As you can see we are already seeing some very exciting opportunities. While the S&P 500 is up 3.5% calendar year to date and is trading close to all time highs, European markets are down circa 10%, the Hang Seng is down 15% and the China Shenzen A Share market is down 32%. While the US still represents 55% of the MSCI World Index, it actually only represents 23% of global GDP and this share is shrinking over time if the forecasts provided by the IMF below are correct. We are looking at investing in tomorrow’s leaders at attractive prices and think the environment today will provide us with a good entry point over the course of the next year.

Source: IMF, World economic outlook report October 2018

Want to find out more?

Did you know that 98% of the world’s investment opportunities are located outside of Australia? We enable investors to access companies from different regions and industries under represented in our domestic market. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments.

Profeta Investments is a global asset management firm focused on delivering high absolute returns. We focus on investing in quality businesses through different phases of their maturity. We manage a high conviction portfolio taking a long term view. We focus on growing companies with strong balance sheets where management teams are aligned with shareholders. For more information visit www.profetainvest.com

2 topics

1 stock mentioned

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments. Profeta Investments is a global asset management firm...

Expertise

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments. Profeta Investments is a global asset management firm...

Expertise

Comments

Comments

Sign In or Join Free to comment