Value Investing: a religious experience

Farmers of seasonal crops are at the whims of the weather. Despite the work and effort put into ploughing and seeding the field, the harvest is, in the end, dependent on the outcome of the weather which delivers feast or famine years. Value investing (the process of buying stocks that are priced the cheapest) has a similar profile. Despite the hard work and effort put into building a value portfolio, the return is, in the end, dependent on the outcome of the stock market whims which delivers feast or famine years to value investors. There have not been feast years in Value investing for a long time.

There are anthropological theories positing that the ability of religion to provide psychological support to farmers was key to the spread of religion. When a farmer puts his all into his work only to have the weather ruin a crop it is helpful to have the representative of [insert regional god here] to explain the random event and encourage the farmer needs to keep the faith and work hard again the next year and the year after.

There is a direct analogy with value investing which tends to deliver its returns in spurts – there are long periods of buying stocks and waiting for them to come good – it is about the belief that value will eventually perform again. There is a fair bit of circumspection among value practitioners, you buy the cheap stocks and then you wait and have faith.

Value is replete also with a never-ending stream of prophets, usually in the form of investment newsletter publishers who generally run with the line that “Ben Graham was the Lord of Value and I am the (self-appointed) prophet who will interpret what he would want you to do (for $1,999 per annum)”

Unfortunately for investors (and fortunately for the prophets), because value returns come irregularly it is hard to judge a value investor. Are the value investors true to their beliefs or have they been tempted by the devil (growth stocks) and so strayed from the righteous path? Are value investors straying from the true path in the darkest hours so when value finally outperforms they are shown as no longer being a true believer and so their portfolio fails to ascend to heaven? You can only tell once every few years when value outperforms and so newsletter writers can keep selling the dream, comfortable in the knowledge that the days of reckoning are widely spaced apart.

Two-part series

I’m going to look at this in two parts (three if you count this podcast):

- What is Value and what has gone wrong

- Measurement error in Value and Value is an axis

Value is a very different strategy

Investment strategies are methods used to divide stocks into different categories and then buy the most attractive in those categories. Some of the most popular are:

- Momentum: very similar to technical analysis – you buy stocks where share prices have been going up and try to avoid ones that have been falling

- Quality: trying to buy stocks with low debt, steady earnings and wide profit margins

- Low volatility: trying to buy stocks with low volatility in price and those that have low correlation with other stocks

- Growth: trying to buy stocks that are going to grow earnings/cashflow faster than other stocks

- Value: trying to buy the cheapest stocks

The important factor to remember when looking at the investment strategy is working out what you are actually assuming. With most investment strategies there is an implicit assumption that there will be no mean reversion. i.e. if you buy a high-quality stock then you are expecting that it will remain high quality. If you buy a stock with good price momentum then you are assuming that the price momentum will continue.

Value is different.

Value is one of the only investment strategies where you are taking the opposite bet and implicitly assuming stocks that are cheap today will go up in price and so not be as cheap in the future.

In my view, this is the key reason why the returns from Value strategies are more sporadic than other strategies: the payoff for Value comes when the market regime changes which doesn’t happen very often. Most other investment strategies are designed to be profitable when the market regime is consistent with the past, which is typically the case.

Value: Where did it all go wrong?

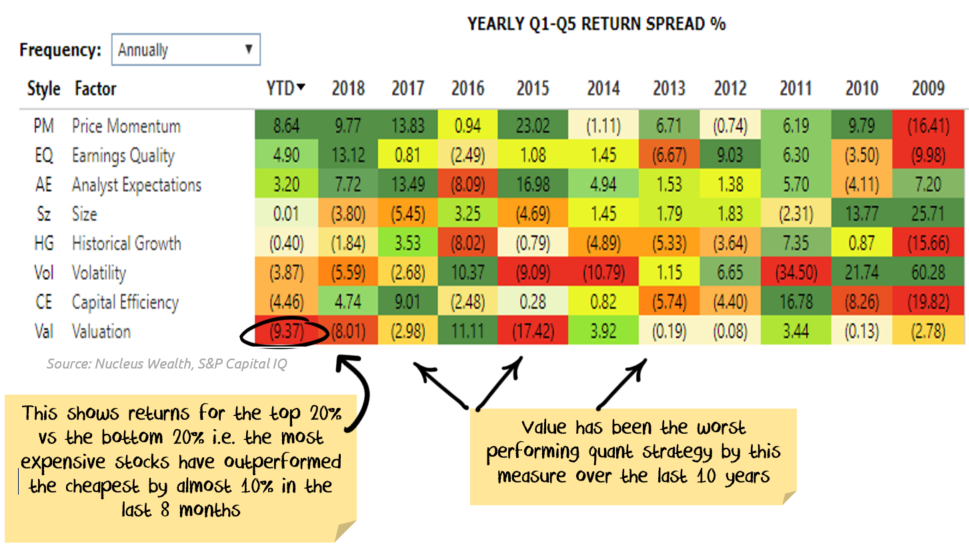

The below tables show the return from a range of different quantitative strategies on the US S&P500 – the story is very similar in most developed markets. The tables show the percentage return between stocks in the best 20% vs the return from stocks in the worst 20%.

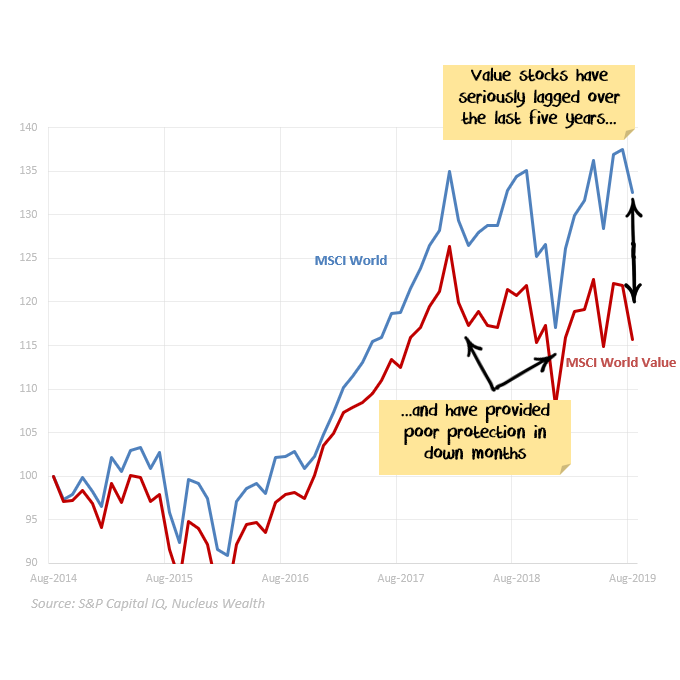

Value performance has been bad. You would have been far better off buying the most expensive stocks over the last ten years:

If you look at the trees rather than the forest it looks no better.

At a macro level, there is an argument that we have been in a bull market for stocks, with stock prices rising rapidly and so it makes sense that value has been underperforming in that environment. One reason for sticking with a value strategy is that Value should protect you when the market does fall.

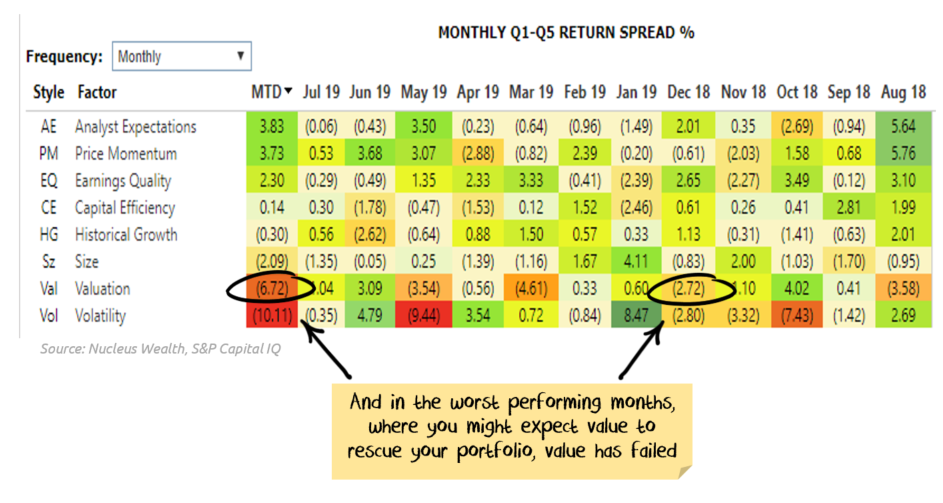

But, concerningly, Value hasn’t been protecting investors in the down months.

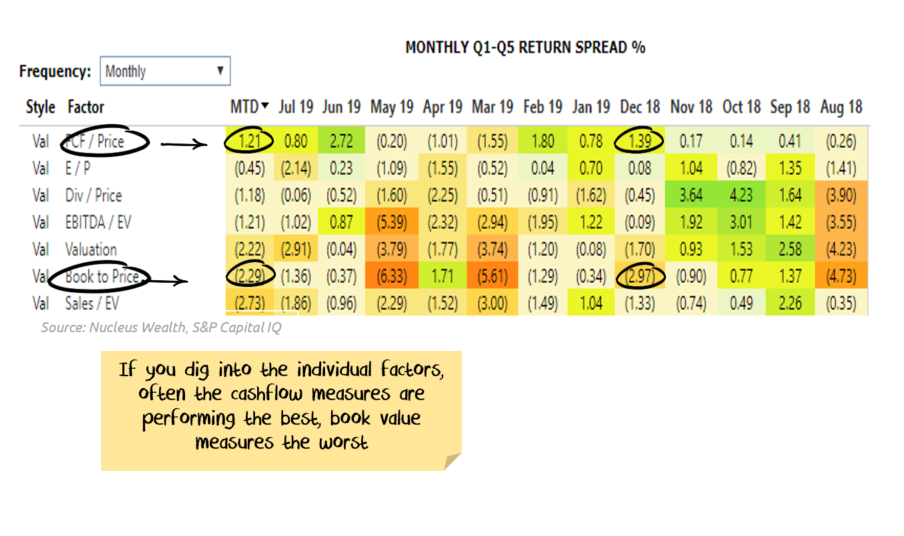

If you look at some of the worst-performing months (August and December) over the last year, and you find that value would have made your performance much worse in those months:

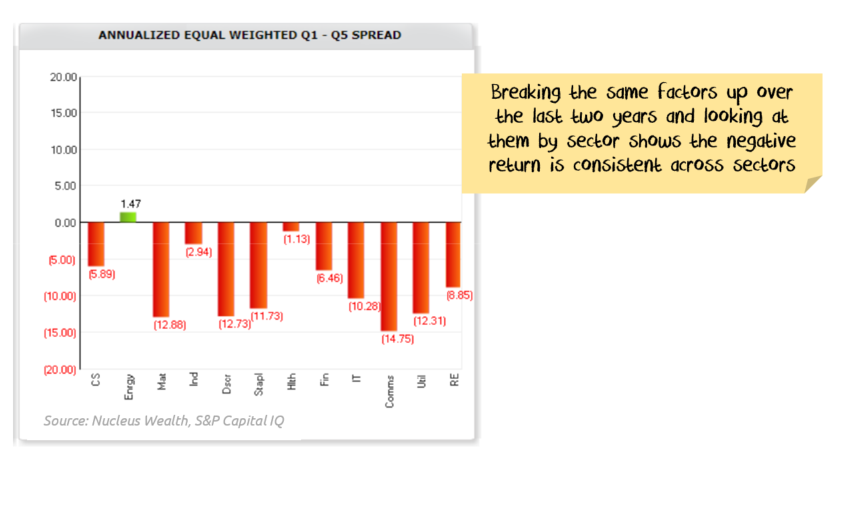

Sometimes when this occurs you find that it is a particular sector that is driving the results, distorting the overall statistics.

That is not the case with Value – the strategy has been poor across a range of different sectors:

The final chart gives some clues as to the culprits behind the underperformance – cashflow value measures, and earnings measures to a lesser extent, have been much better performers and protectors in down months than book value measures:

This is what we will delve into in part II of this post:

- Are there measurement errors with Value strategies? (spoiler: yes)

- Should you be using Value on its own as a strategy (spoiler: no)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

........

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

1 topic

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Comments

Comments

Sign In or Join Free to comment