Valuing NABHA

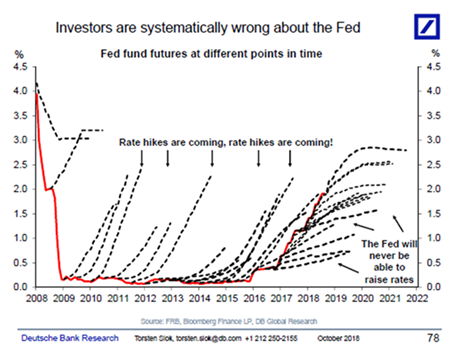

I've written a column summarising our valuation views on NABHA, which are excerpted below (click on that link to read the full column or AFR subs can click here). We look at scenarios where NABHA remains perpetual and others where it is called with both converging around the $85 mark. As a random aside, I have also enclosed a chart from Deutsche Bank showing how markets have consistently underestimated the speed of the Fed's rate hikes...

One of the biggest myths about the $2 billion NABHA is that its contribution to NAB's additional tier 1 (AT1) capital (or equity) buffer has declined by 10 per cent annually from January 1, 2013, implying that only 40 per cent (or $800 million) currently counts as AT1.

NABHA was issued in June 1999 with what looks today like a miserly non-franked income margin, or spread, of only 1.25 per cent above the three-month bank bill swap rate (BBSW). Given a current BBSW rate of 1.93 per cent, NABHA costs NAB about 3.18 per cent in annual income distributions, which is materially below new-style hybrids.

If only 40 per cent of NABHA classifies as AT1, however, it is becoming increasingly expensive compared to its historic cost (when it contributed more AT1) and Basel 3 hybrids. The imputed spread above BBSW of 6.02 per cent of a 40 per cent AT1 share of NABHA, which comes to a total cost of 7.95 per cent, is both dramatically higher than its original 3.18 per cent price (in today's BBSW terms) and the cash cost of recently-issued hybrids.

The problem with this analysis, which has presumably motivated tens of millions of dollars of allocations to NABHA, is it is wildly wrong.

When moving from Basel 2 to Basel 3, APRA allowed NAB to aggregate all its hybrid securities at the end of 2012, which amounted to $6.05 billion, and then deduct 10 per cent (or $605 million) annually from this fixed number. As NAB repaid or refinanced different Basel 2 hybrids, the amount of AT1 capital remaining based on the fixed $6.05 billion pool is credited to any outstanding securities.

This drives the counter-intuitive result that NABHA's contribution to NAB's AT1 capital base is more than double what investors believe – exactly 82.9 per cent today rather than the 40 per cent level deduced from straight-line amortising NABHA's $2 billion face value. And because NAB has just announced that it is repaying the only other Basel 2 hybrid it has left (the £400 million security cited earlier), NABHA's contribution to AT1 will jump to 93.3 per cent in 2019...

This begs the question: what is NABHA really worth?

My quants offer the following methodology. Let's first assume NABHA is never repaid or exchanged, thereby remaining perpetual. Given NABHA ranks equally with modern hybrids in a wind-up, has lower equity risks in non-viability, and a longer maximum term, let's suppose that the return required by investors is set around the longest-extant hybrid, WBCPH. This suggests a required spread above BBSW of between 3.71 per cent and 4.0 per cent, which in turn indicates NABHA is worth between $83.65 and $87.42 if it is never repaid or replaced.

NAB does have an incentive to replace NABHA with a new hybrid by the end of 2021, which is a year in which it notably has no hybrid maturities. It would make sense not to offer to repay NABHA, and only give holders the option of either keeping the perpetual or exchanging it for a new hybrid.

Suppose NAB is generous and sets the exchange price at $90, providing holders with a decent capital gain to encourage them to roll into it. If this happens, NABHA is worth between $84.53 and $85.51 given its future cash flows of 1.25 per cent over BBSW, the 2021 exchange price of $90, and a required return (or discount rate) of between 3.75 per cent and 4.0 per cent over BBSW. In either scenario, a price around $85 looks reasonable.

Click to read the full column here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management