What Mattered Today; Shorts target Blue Sky, A2 Milk attracts competition

+40 up yesterday and -40 down today as we roll into the four day break over Easter from tomorrow afternoon onwards – the longest stretch of the year the market is closed! Stock options expiry today (rare on a Wednesday) so a busy one on the desk while a number of interesting stock specific rumblings filtered across the ticker – a particularly interesting note on Blue Sky (BLA ) while A2 milk and Fortescue Metals were also in focus. More on those later.

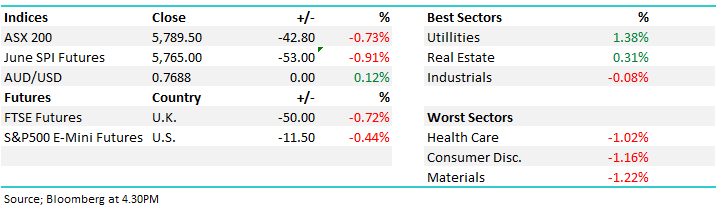

On the market today, resources were the weakest link down around 1.2% while it was the defensive names – Utilities and Real Estate that did best. An overall decline of -42pts or 0.73% on the ASX 200 which closed at 5789.

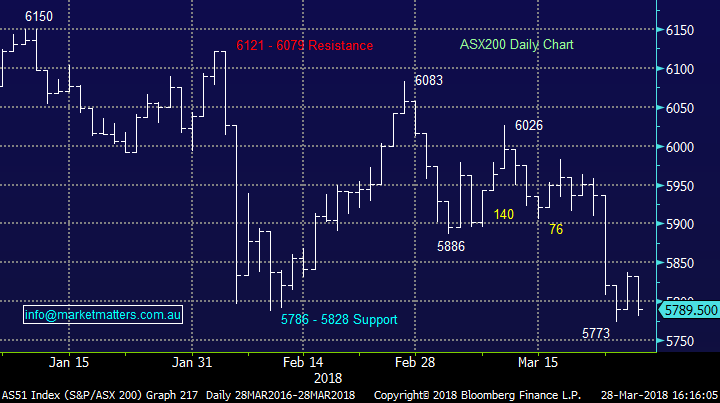

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE

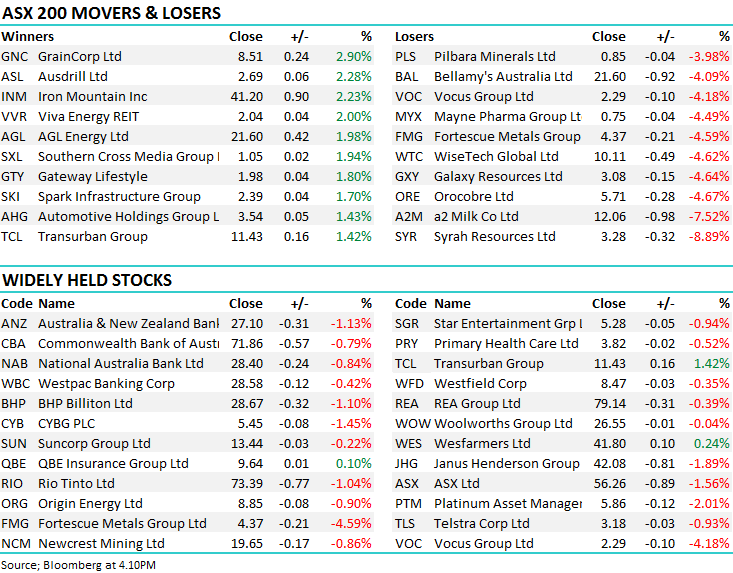

A2 Milk $12.06 / -7.52%; came under pressure today as Nestle, the world's biggest food and beverage company, announced plans to ‘rip off’ the A2 concept launching a brand of infant formula that uses the A2 beta-casein protein. They’re even calling the product Atwo – reminds me of the McDowell’s restaurant in the movie, Coming To America! Clearly A2 Milk has a highly attractive business with sublime metrics as shown in the last report, but that makes it ripe for competition, and Nestle is a big Gorilla. A2 clearly have the advantage of the ‘paddock to plate’ quality perception but as Peter McKenna suggested today when I was on Sky Business around lunchtime, Blend 43 is a bad cup of coffee but it’s the world’s best seller!

A2 Milk Chart

Blue Sky Alternative (BLA) $10.40 / -9.01%; This was the target of a ‘big short’ piece from a research house today with Glaucus Research suggesting the stock is actually worth <$2.66 a share, a fraction of its current value – nothing like an inflammatory note to get the mkt excited.

Firstly, the short thesis on BLA is not new with discussion of this floating around the market for some time. The fact that it’s now getting airtime through a reasonably well recognised research firm clearly adds to the strength and thus the market’s reaction. The report highlights a few things that really, we should already know, however here is our take.

This is an extremely complicated company with more than 80 different funds underneath it’s umbrella , a huge variety of assets, and a complex mechanism of collecting fees between them. Simply put, we find this hard to reconcile which I guess is the crux of the research report. To dumb things down though, I’ve always thought of an asset manager simply in the context of rising asset prices and cheap money. If the cost of capital is low and asset prices are rising, then all is good, BUT if the cost of capital rises which coincides with declining asset values, then things can unravel.

Over the past few years the drivers of BLA earnings (cheap money and rising asset prices) have been incredibly strong, however it's our belief that we're at a turning point, and for that reason we have no interest in BLA, irrespective of wherther or not todays research piece ihas substance or not.

Blue Sky Alternative (BLA) Chart

Have a great night

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 stock mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment