Why 2019 could be uranium’s break out year

The spot price of uranium is up 33% this year, ending a 7-year bear market, although it remains below the cost of production for close to half the world’s production and a number of mines have been shut down in 2018. With the demand picture improving and a run down in stockpiles caused by significant supply cuts and under buying by nuclear generation companies, we see a bright future for uranium.

Rising Demand

Global electricity demand is forecast to grow approximately 50% over the next two decades, with this number potentially looking conservative in the face of rapid electric vehicle adoption. To address capacity needs, the world is seeking high baseload, low cost and zero emission power. Nuclear power can solve all three. There are currently 454 Nuclear Power Reactors in operation supplying 31 countries around the world, with 54 under construction, another 148 planned and 337 proposed, across Europe, India, USA and China according to the International Atomic Energy Agency.

We see growth in nuclear power generation, driven by three major regions:

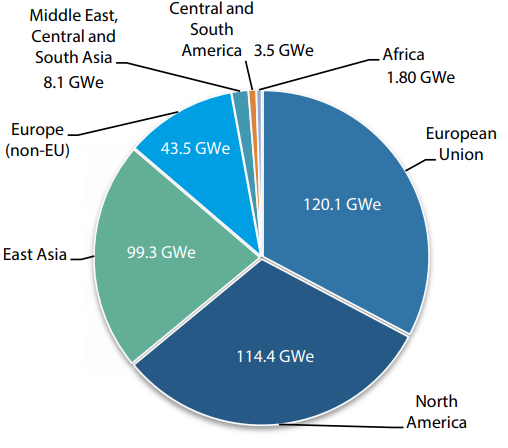

Global installed nuclear capacity (source: IAEA)

Western (North America and Europe) demand account for approximately 60% of nuclear capacity, and demand in these regions is flat to slightly growing. There are few new reactors being built in these regions due to very high construction costs and significant lead times, although this is being balanced by the need for reliable baseload power and public concern over fossil fuel use. Countries which are heavily reliant on nuclear such as France and the US are extending reactor lives which is a positive sign for ongoing demand.

Japan has approximately 10% of the world’s reactors however the majority are not operating post the Fukushima disaster in 2011. The pace of these restarts will be slow, however bringing Japanese reactors back online will support demand growth over coming years.

China has the most aggressive growth plans for nuclear. With only 4% of power generation currently met by nuclear power and a target of 20% non-fossil fuel generation by 2030, there is a significant reactor build required of approximately 5 times current capacity. According to research by the Chinese Ministry of Education and Tianjin University, China, within the latest 2018 Optimal Power Paper, nuclear energy is now the lowest cost source of electricity generation in China.

In China the first of a kind (FOAK) reactor designs were switched on this year in China after 9 years of design. This testing means China is ready to roll-out new reactors, which is confirmed by the current 5 Year Plan. There are also new High Temperature Gas Reactors (HTR-PM) currently being commissioned that are compact, safe, efficient, capable of use in inland areas and are able to attach to existing coal fired power plants to replace coal use.

More recent research out of China suggests a more than 20 fold increase in nuclear generation (from 26GWe in 2015 to 554GWe 2050) is required in order to meet the target of limiting global temperature rises to 1.5°C. While reaching these numbers would be a huge stretch after considering nuclear capability and funding requirements, it is evidence of the commitment that the country has to combatting pollution, with nuclear energy benefiting as a zero emissions power generation source. For much of the decade through to 2014 nuclear had around a 2% share of power generation in China, however this has been steadily rising since, and in the last few months of 2018 has spiked to nearly 5%. This production is coming at the expense of coal fired generation.

The need for China to secure supply to meet its growing nuclear generation needs is expected to be an emerging theme over the next 12-24 months.

In addition, there have been two major recent positive demand developments we have seen this year. Firstly, Cameco is having to buy a significant quantity of uranium on the spot market to satisfy their sales contracts due to shutting a large quantity of their own production. Secondly, there have also been several financial players enter the market to buy uranium for speculative purposes – the most significant being London listed Yellow Cake, who have an agreement to purchase uranium from Kazatamprom.

Supply Deficits

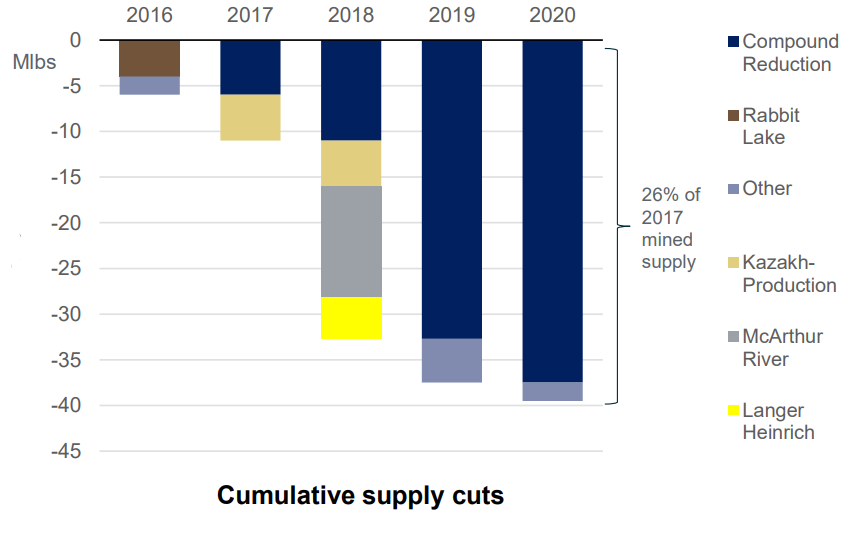

While demand is showing signs of reasonable growth, uranium in the short term is really a supply story, with a number of significant uranium producers cutting back production over the past two years in response to the sustained low price. Cameco shut McArthur River earlier this year (the world’s largest uranium mine), Kazakhstan is the world’s largest producer and has cut production 20%, and Paladin (ASX:PDN) has shut their Langer Heinrich mine in Namibia.

Uranium supply cuts (source: Paladin Energy)

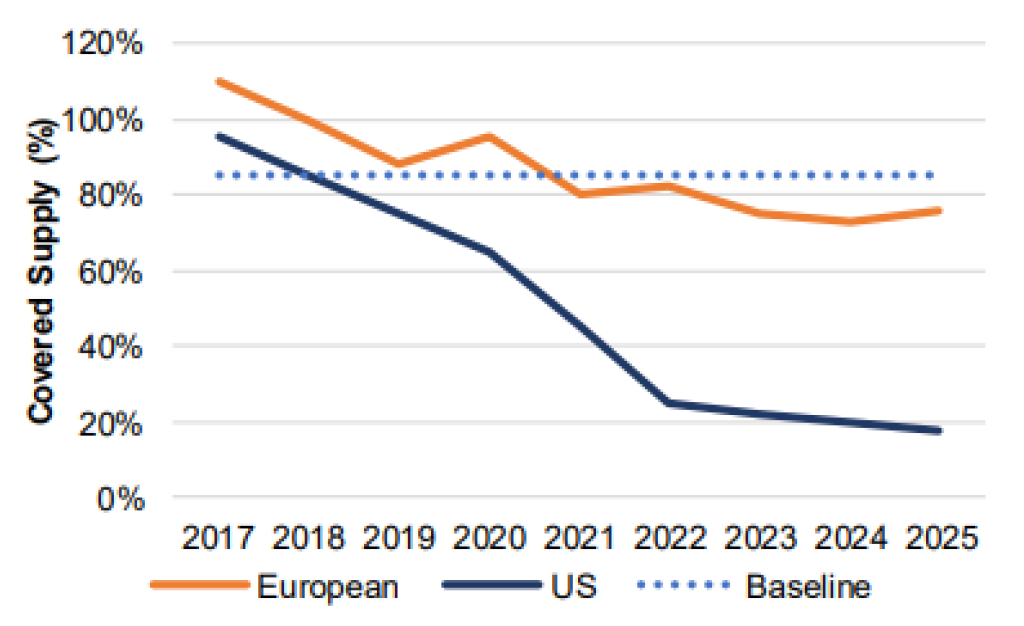

We think that around half the world’s mines are producing at loss making levels at current prices, and this will really start to hurt producers once higher priced contracts roll off in the coming years. Uranium is a unique commodity whereby the raw material cost represents only around 3% of the total cost to produce nuclear energy. Therefore the cost per MWh of electricity is highly inelastic to any price changes in the Uranium spot price, and when utilities enter the market to contract future supply they typically pay a premium to spot for certainty of long term supply. US utilities in particular will need to re-enter the market given their supply coverage is rapidly falling away over the next 3 years. We think this will be a key catalyst to get the uranium price higher in 2019.

Future contract coverage rates (source: EIA, Euratom)

There is a clear supply shortage present in Uranium, with new production not incentivised to come online until prices reach a level of material profitability. We estimate the market is currently around 10% under supplied, with this supply gap increasing over coming years unless production levels recover.

Some commonly quoted numbers are $40-60/lb to re-start idled mines and $60-80/lb to incentivise new mines to start construction. These prices represent upside of between 38% and 176% compared to today’s price of $29/lb. Whilst timing is always the great unknown, it is clear that supply has been cut sufficiently to warrant a price reaction, and we see it as being a matter of when, not if, uranium prices rise back towards incentive levels.

How to Gain Uranium Exposure

International investors may look to pure play exposure such as Yellow Cake (LON:YCA), or Cameco (TSE:CCO) for its diversified position across the supply chain, but in Australia the cleanest way to play uranium is through Paladin Energy (ASX:PDN).

Paladin’s Tier 1 Langer Heinrich mine is the lowest cost open pit mine globally. According to UxC, the leading nuclear industry market research company, Paladin was in the first tier of the production cost curve, with all in cost of production at Langer Heinrich of US$28/lb. Paladin is well funded to a restart decision, with the company forecasting to hold around US$40m in cash by the end of the current quarter. If the uranium price reaches a sufficient level to incentivise a mine restart, the mine could be up and running in around 12 months and potentially be one of the first restarted mines back into production.

The leverage in Paladin is huge – at a US$40/lb uranium price we estimate their 75% share of the Langer Heinrich mine will produce around $40m of cashflow, going to $130m at US$60/lb and $230m at US$80/lb. These numbers compare favourably to Paladin’s current market cap of $315m and demonstrate the value proposition on offer. At higher uranium prices the market will also likely start to ascribe some value to Paladin’s other assets – the Kayelekera mine and their 300mlb exploration portfolio. At this stage Paladin remains a risky proposition (like most other uranium stocks), however if the uranium story plays out like we believe it should, then investors will be rewarded for their patience.

Recent share price movements for uranium companies have lagged the spot price. We see a brighter future for uranium stocks as the demand outlook continues to improve, cumulative supply cuts draw down existing inventories and buyers re-enter the market.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt is Co-Portfolio Manager for the Maple-Brown Abbott Australian Small Companies Fund. He has 14 years investment experience in the Australian small and micro cap space, previously working for AMP Capital, IFM Investors and Macquarie Group.

1 topic

1 stock mentioned

Matt is Co-Portfolio Manager for the Maple-Brown Abbott Australian Small Companies Fund. He has 14 years investment experience in the Australian small and micro cap space, previously working for AMP Capital, IFM Investors and Macquarie Group.

Expertise

Matt is Co-Portfolio Manager for the Maple-Brown Abbott Australian Small Companies Fund. He has 14 years investment experience in the Australian small and micro cap space, previously working for AMP Capital, IFM Investors and Macquarie Group.

Expertise

Comments

Comments

Sign In or Join Free to comment