Why Infigen's share price could power up

As Australia continues its slow, but steady, journey to decarbonise its economy, there will no doubt be winners and losers. One of those winners could be Infigen Energy (ASX: IFN), which develops, owns and operates renewable energy generation assets.

Big picture – the Paris Accord – United Nations climate change agreement

The Paris Accord is an agreement outlined in 2016 by 196 nations, 188 of which have now signed up and become a party to that agreement, with the only significant emitters failing to do so being Iran and Turkey. The Accord lays out cuts to carbon emissions, 26-28 per cent of a baseline by 2030, that are required to achieve a limit on global average temperature increases to 2 degrees, and pursue “efforts” to achieve a lower 1.5 degree increase. The Accord doesn’t force parties to set specific national emissions targets, but ask’s parties to determine and report on emissions and initiatives that seek to mitigate global warming.

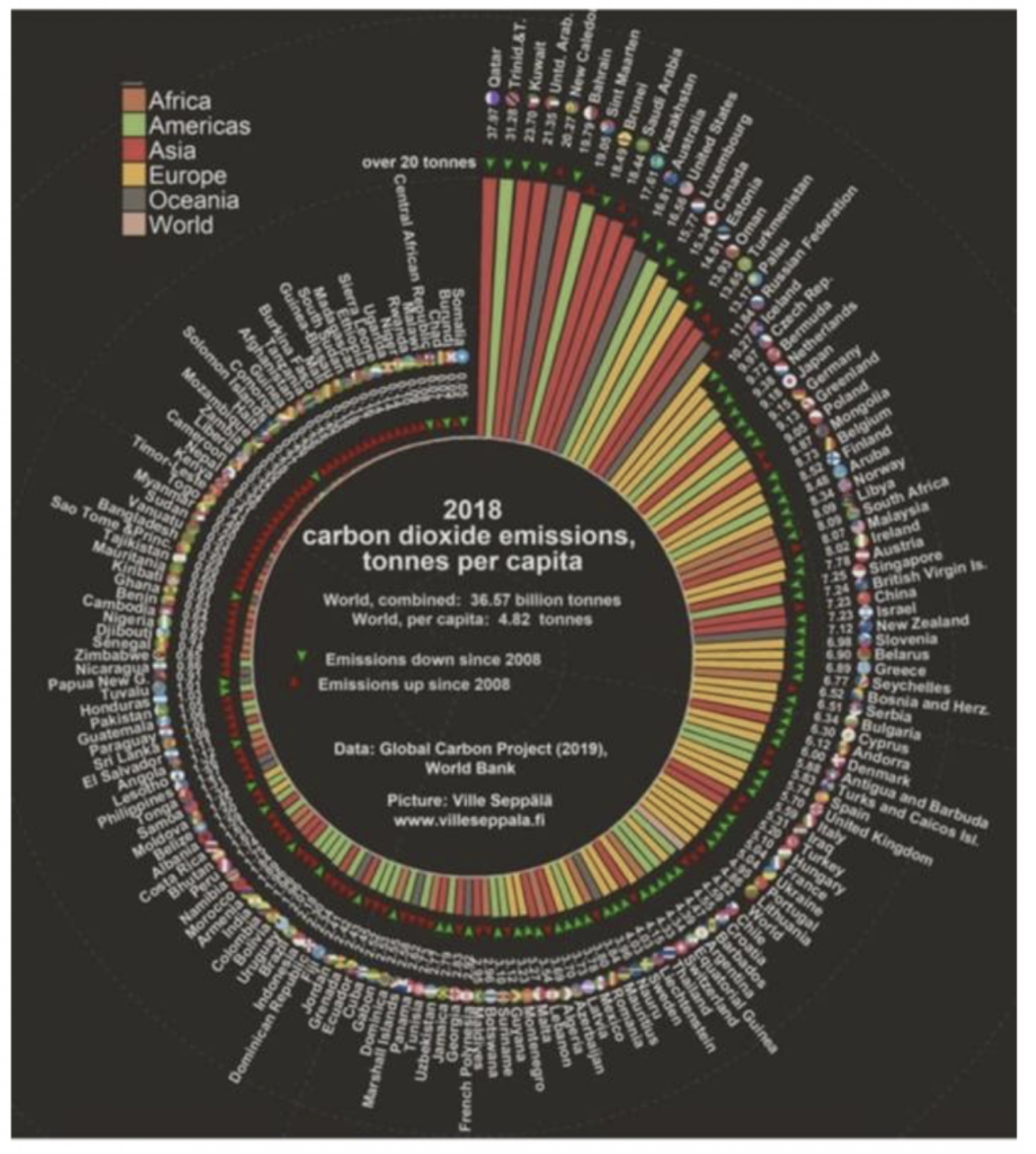

Different nations are at different start points in their “de-carbonisation” journey, with the developed world economies clearly much more carbon intensive than emerging markets. See Chart 1 using World Bank Data from its Global Carbon Project resource.

C02 Emissions per capita

Source: World Bank

According to the data, Australia is a top 10 per capita emitter, so we have work to do. Unfortunately, the politics of climate change here has been sufficiently toxic as to deny leadership clarity on this issue; today it doesn’t look like Australia is positioning to meet its Paris Accord commitments.

Australia is not alone, for example the US, under the Trump Presidency, has indicated it plans to withdraw from the Paris Accord.

However, there are other nations taking active steps to meet their Accord obligations. The tipping point of climate change concern amongst many European societies appears to have been reached and despite the economic pressures many nations are actively taking the steps to alter the carbon intensity of their economies. Measures like legislating for the ban of sale of internal combustion engine cars at some future point (Norway 2025, UK 2035/40 and others), altering the mix of their electricity generation networks, targeting high carbon emission generation (coal largely) and replacing it with renewables (wind and solar) supported by flexible generation (usually gas) to cope with the fluctuations that renewables bring when the wind doesn’t blow or the sun doesn’t shine.

The changing profile of the UK’s generation mix

Source: Electric Insights

What’s changed – Global Corporates are starting to act

A recent series of poor climate events have elevated the climate change debate as a top media topic, here and overseas, and it’s spurring some large companies and institutions to act. Some are seeking to de-couple their brands from carbon-intensive activities that are seen to be part of the problem (for example some large investment funds are committing to sell fossil fuel investments), others are going further to be seen to be part of the solution and taking action to become carbon neutral, or negative. Microsoft’s recent “2030 carbon negative” pledge is an illustration of the type of informed decision making, taken independently of legislation driven by politicians. There are many more (Google, HSBC, Amazon, IKEA, and others, even fossil fuel energy companies BP & Shell).

So, decarbonisation is coming, its being driven by corporates, responding to trends they see in society. A consistent feature in the response is a move to power operations using renewables, from the lights in the office to the fuel source for vehicles. The renewable electron is at the heart of the solution. Corporates are assuming that carbon has a cost, and it’s not zero.

Where to find the renewable electron in Australia? – Infigen Energy (ASX:IFN)

IFN is a renewable electricity generator. It’s had a chequered past, caught up in the financial engineering bubble that preceded the GFC which means that many fund managers aren’t looking, and don’t appear to have noticed what now looks like a good volume growth story with conditions firming around the medium term outlook for a price on carbon – two significant drivers we think for IFN’s earnings and valuation that we explain here. IFN’s portfolio and capital structure are now in a “sustainable” state (pun intended), dividends re-started at the end of F19, and 100 per cent of its production are those sought after renewable electrons.

IFN is positioned to be a multi-year volume growth story

IFN has a portfolio of wind assets capable of generating renewable electricity to the tune of approximately 1.8 GWh of power per annum, it also has a newly commissioned battery storage facility (52MWh) and has recently acquired two gas peakers – 123MW in NSW and 120MW in SA – adding these assets to the portfolio changes the game for IFN.

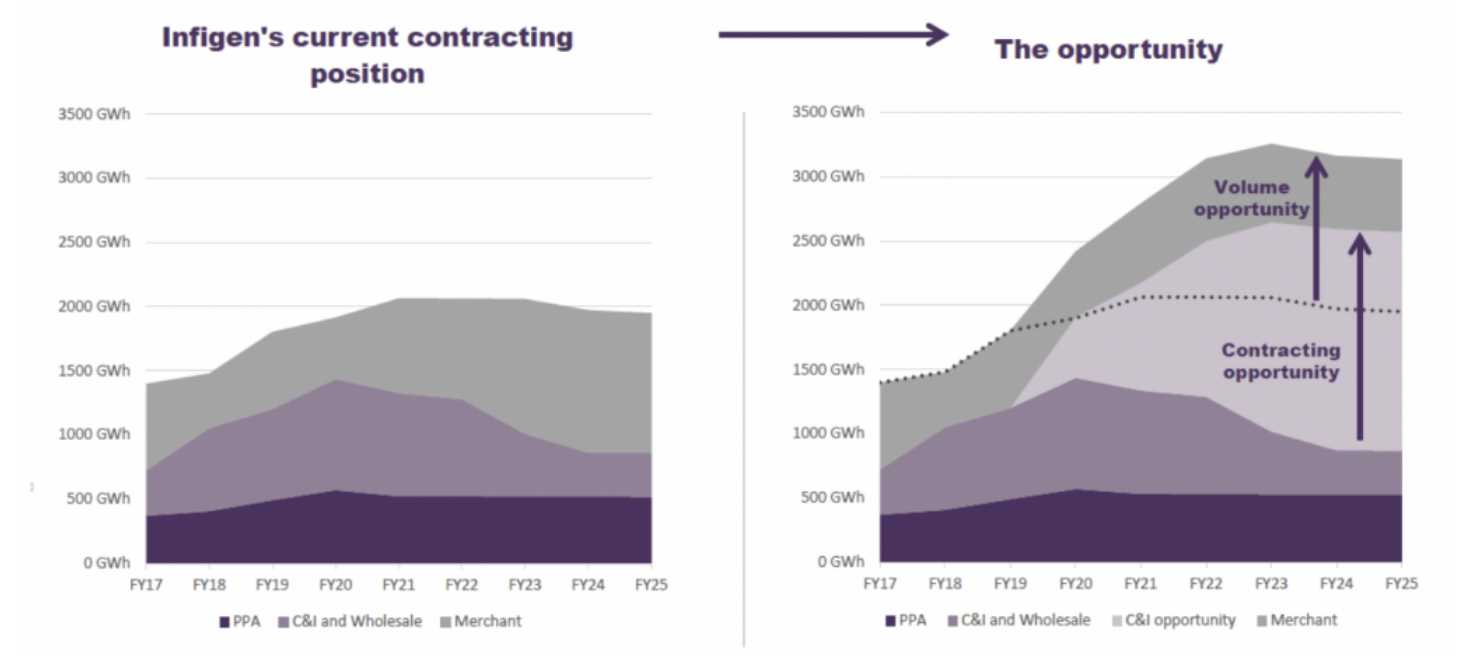

Renewable generation comes with the problem of what to do when the sun doesn’t shine or the wind doesn’t blow (in IFN’s case) in the right place, renewable generation at an asset level can be intermittent. Diversification – having assets at many different locations in your portfolio – helps but doesn’t reduce this risk sufficiently; consequently IFN doesn’t seek to contract its full supply position for fear of not being able to deliver. This positioning is illustrated in chart 3 from IFN below, “merchant” representing the uncontracted exposure.

IFN production volumes & the expected impact of firming assets

Source: Infigen Energy

The solution is to “firm” the renewables with assets that offer reliable supply when called upon – this is where the battery and the two gas peakers come in and change the game. These three assets should allow IFN to contract more of its renewable supply than before. In fact, a lot more. IFN has suggested that the recently acquired firming assets can support over 3GWh of renewable generation, (we think this could turn out to be more like 4 GWh) which is greater than IFN’s existing capacity.

Consequently, IFN is seeking to contract intermittent renewable generation supply from other renewable sources, and sell that supply on a contracted “firmed” basis to customers looking for green energy. The contracted price of “firmed” renewable green energy is higher than for “unfirmed”, allowing IFN to collect a margin on the way through. Contracting for supply, rather than building and owning the assets, allows IFN to grow its production without incurring the capital cost, the growth here is capital light. The chart above from IFN shows the volume growth plan to get to roughly 3200GWh, which is about 65 per cent higher than production in 2019.

IFN and the carbon price

The price IFN receives for its renewable generation is made up of the “black” price for the electricity plus a “green” credit for its carbon-free nature. This “green” credit is known as an LGC and represents the “carbon price” of approximately 0.8 tonnes of CO2 emissions. It’s these credits that turns “black” electricity “green”, and corporates can acquire these to offset their emissions profile. IFN’s earnings and valuation are sensitive to the carbon price as it’s a revenue stream with no input cost, it’s 100 per cent profit. Simple maths suggests that every $10 of carbon price, at current production of 1.8GWh, that’s $18 million to EBITDA; at the expected future production of 3200MWh, that same sensitivity rises to $32 million to EBITDA. But what is the outlook for the carbon price?

The price of carbon is difficult to call, historically it’s been heavily influenced by political and regulatory changes, as well as the demand-supply balance for these LGCs. There are a significant amount of renewable projects that are being added to Australia’s generation mix and these will add to the supply of LGCs. We see rising demand too. There is no liquid market for carbon to act as a reference. LGCs in Australia last traded at A$31, (having traded between A$30 and A$50 over the last 12 months) equating to A$39 per ton of CO2, and the price of a European Emission Allowance (a permit to emit 1 ton of CO2 or equivalent) is EUR23, or A$37 per ton of CO2. We don’t know what the price of carbon will be but based on what we can see today it’s unlikely that the market will conclude that this price is going to be zero any time soon. And that volume growth we see should convert to growing profits.

Is IFN an interesting investment?

IFN is levered to a strengthening global theme – decarbonisation – and is executing a strategy to take advantage of the rising demand for renewable electricity through the recent acquisitions of its firming assets, volume growth is expected to be strong and also capital light. Whilst we can’t accurately forecast the future price of carbon, we believe that we can see conditions emerging where corporates, driven by growing public opinion, take steps to decarbonise their activities. A core element of their response so far is to seek renewable power and the green credits that come with that, which we think is supportive for carbon price and good for IFN’s growth, earnings and cashflows.

These conditions are supportive for IFN’s business growing its earnings, but we note that consensus expectations are for earnings decline, not growth, as consensus forecasts have yet to pick up the volume growth opportunity or are not reflecting a better carbon price outlook.

IFN’s current valuation at 6.2x F20 EBITDA is attractive. We value the stock at $1–1.10 depending on how quickly volume growth comes through.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

4 topics

1 stock mentioned

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

Expertise

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

Expertise

Comments

Comments

Sign In or Join Free to comment