Why it pays to be contrarian

Nathan Bell

Investsmart

In part one of this three-part series, we explained how buying companies where management has their own wealth on the line can help you beat the market. In this article, part two, we’re going to analyse a current portfolio holding to show how you can trounce the market if you’re prepared to be contrarian.

Being contrarian is not a simple mathematical formula. Nor does it guarantee success, which is why value investing is not more popular. Instead, it requires a detailed knowledge of how a company and its industry works so you can handicap what expectations are priced into its stock and act accordingly.

Most importantly, though, being contrarian doesn’t mean doing the opposite of other investors just for the sake of it. As the father of value investing Ben Graham once said, ‘You are neither right nor wrong because the crowd disagrees with you. You are right because your data and reasoning are right.’

While it’s necessary to do the opposite of what most other investors are doing to make large returns, your factual reasoning must also be correct. This is what gives you the confidence to go against the herd. If you don’t know the inner-workings of the business you’re buying, or the industry it operates in, how can you estimate whether the stock’s prospects are accurately reflected in its stock price?

Liberty Broadband

Let’s analyse a contrarian investment we bought in February 2016. Liberty Broadband is a holding company that we bought at a discount to the value of its only major asset, a shareholding in cable TV company, Charter Communications.

Figure 1. Negative press in the media.

Source: Wall Street Journal

Last year, you couldn’t open the Wall Street Journal without reading another obituary about cable TV companies. The perception was that cable subscribers were falling and would fall faster over time as more people switched to cheaper online entertainment alternatives, like Netflix or Stan. As the market often does, it put these ‘facts’ together and assumed the days of charging customers over $100 per month for their cable service were at an end.

Adding to concerns was Charter Communications’ bid to acquire Time Warner Cable, which would make Charter the second largest cable company in the US in an industry where size matters. The 800-pound gorilla of the cable industry, Comcast, had effectively been denied the right to acquire Time Warner Cable just one year earlier. The market figured Charter’s bid would suffer the same fate.

Different conclusion

After performing our due diligence, the facts provided a different view of Charter Communications’ prospects compared to the consensus.

First, Charter Communications wasn’t losing cable TV subscribers. It was mainly the satellite cable TV providers that were suffering, as their service was inferior and they didn’t offer phone and broadband services that you could bundle with your cable TV subscription in comparison to at Charter, where you could save money (also known as the ‘triple play’).

Second, while over time we expected Charter to lose cable TV subscribers, its broadband internet service should enjoy strong growth and increasing average revenue per subscriber for years to come. That’s because most people upgrade their internet service when they cut their cable subscription to make sure online services like Netflix aren’t slow or interrupted. It’s also worth noting that that the broadband business enjoys much higher margins than cable TV, as the incremental cost of adding a broadband subscriber is minimal.

We were also confident that Charter Communications would receive regulatory approval to acquire Time Warner Cable, as Netflix’s CEO Reed Hastings had given his blessing along with the New York state regulator. Our view turned out to be correct, but if we were wrong we expected it to be a case of heads we win, tails we don’t lose much. These odds are what we look for in all our investments.

Contrarian view

So here was a classic case where a very high quality business was undervalued because the market was myopically focused on one part of the business, instead of its many virtues, including its highly recurring revenue, huge barriers to entry (as shown recently by Google’s failed attempts to expand fibre to the home – it’s very expensive digging up the sidewalk to install cables and wires), fast-growing broadband internet service, and the potential to create a huge amount of value from an impending acquisition; all overseen by CEO Tom Rutledge, who is widely regarded as the cable industry’s best operator.

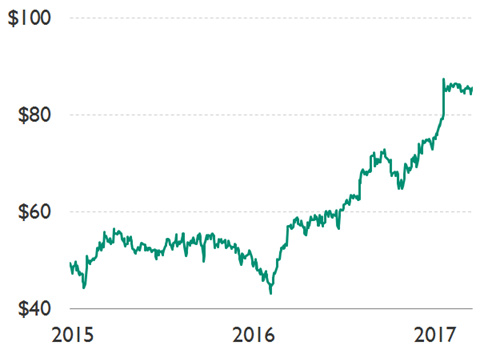

Chart 1. Liberty Broadband share price chart.

Source: Capital IQ, Peters MacGregor Capital Management

With Liberty Broadband’s price almost doubling over the past year, it became our largest holding as investors regained their senses and recognised its true value. Telecommunications company Verizon has also shown interest in acquiring the business recently, again showing that it was vastly undervalued for such a high-quality business when we bought it.

The large gain so far was only possible because the market was myopically focused on the cable TV business, and wasn’t thinking long-term about the broadband internet division to uncover the stock’s true worth. The facts were available to anyone prepared to do the work, but you had to stand against the crowd and be prepared to wait for the value to be realised.

Betting on macroeconomic changes consistently is virtually impossible. But if you look for reliable indicators of value, such as insider ownership and low valuations, and most importantly you’re prepared to back your judgment despite the consensus arguing otherwise, you can beat the indexes too.

Nathan Bell is Head of Research at Peters MacGregor Capital Management.

Disclosure: Peters MacGregor Capital Management Limited holds a financial interest in Liberty Broadband through various mandates where it acts as investment manager.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nathan has over 20 years' investment experience. Before joining Peters MacGregor, he worked for 9 years at Intelligent Investor, including 4 years as a Portfolio Manager. Nathan is a CFA charterholder

4 topics

Nathan Bell

Portfolio Manager

Investsmart

Nathan has over 20 years' investment experience. Before joining Peters MacGregor, he worked for 9 years at Intelligent Investor, including 4 years as a Portfolio Manager. Nathan is a CFA charterholder

Expertise

Nathan Bell

Portfolio Manager

Investsmart

Nathan has over 20 years' investment experience. Before joining Peters MacGregor, he worked for 9 years at Intelligent Investor, including 4 years as a Portfolio Manager. Nathan is a CFA charterholder

Expertise

Comments

Comments

Sign In or Join Free to comment