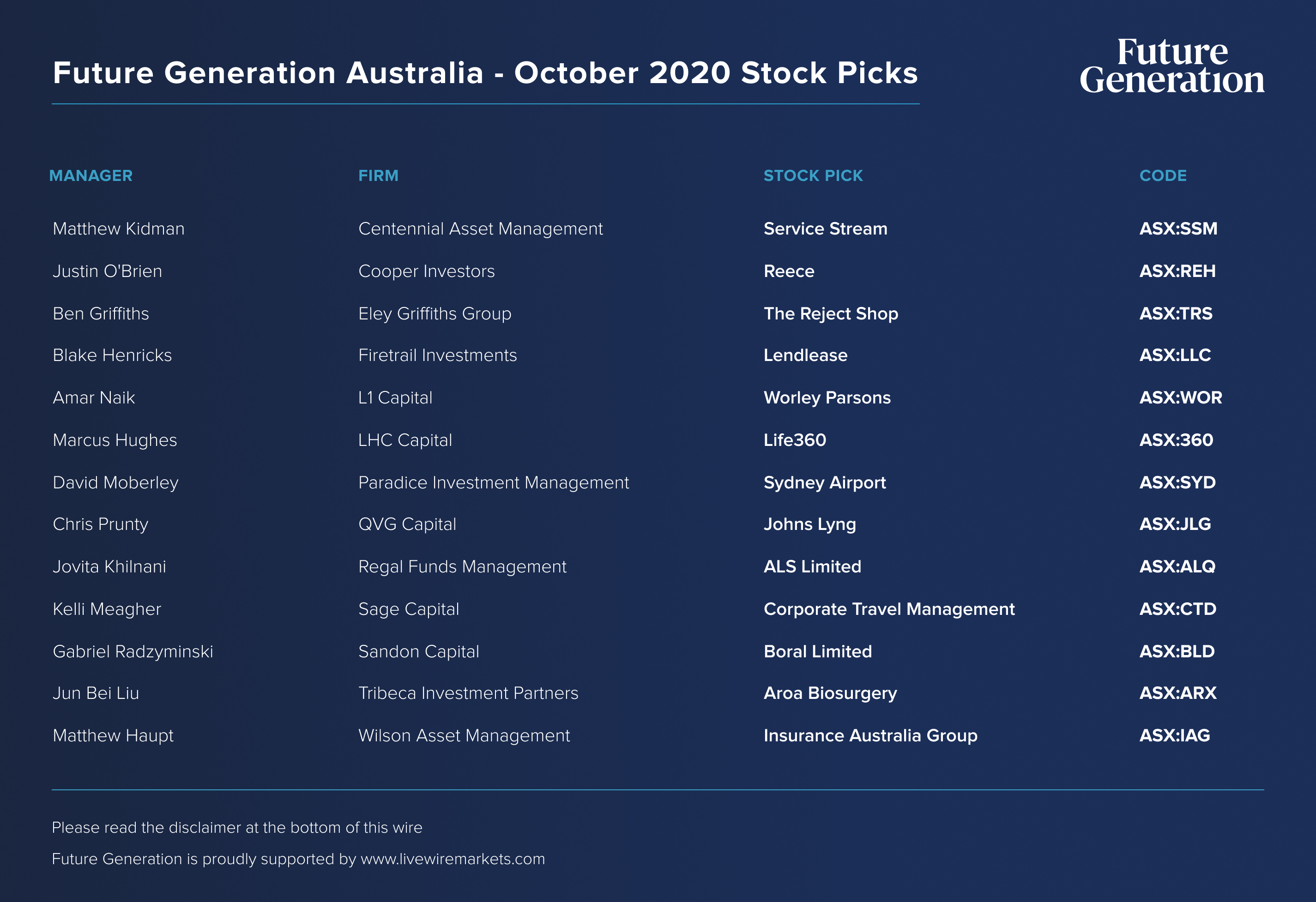

22 high conviction stock picks from Future Generation Fund Managers

Future Generation, the investment vehicles setup to help fund charities that support children and youth at risk and youth mental health is proud to host the Future Generation Virtual Investment Forum. The forum features 22 of Australia's top fund managers, and they share high conviction stock ideas from Australia and overseas.

Claire Britton of Magellan nominated Alibaba as her top stock for the forum in May 2020. The technology behemoth soared 34% since. Meanwhile, ASX fibre infrastructure company Opticomm, selected by Chris Prunty of QVG, and semiconductor giant Infineon Technologies, picked by Curtis Cifuentes of Avenir Capital, jumped 29% and 22%, respectively. Investors who followed the fundies’ picks from May were rewarded with above-benchmark returns during the period.

With the bar set high, Magellan, QVG Capital and Avenir are back as part of a panel of 22 fundies who’ve shared fresh ideas. We’re thrilled to give Livewire readers access via the article below.

13 high conviction Aussie picks

Click on the image to enlarge

Service Stream (ASX:SSM)

Matthew Kidman, Centennial Asset Management

Service Stream provides services, predominately labour, to the large telecommunications, retail energy and water industries. Among the work performed by Service Stream includes connection and maintenance of the national broadband network, building and maintaining mobile phone networks across Australia, the installation and maintenance of smart energy metres and the preservation of water infrastructure. The bulk of Service Stream’s customers are large enterprises such as Telstra or major government owned entities. The bulk of the services are carried out on behalf of Service Stream by contracted skilled labour.

Service Stream’s fortunes have, in recent years, revolved around the evolution of the National Broadband Network (NBN). Initially chosen to help build, connect and maintain the NBN network, the company saw its share price rise seven times from late 2014 to mid-2019. Since then however, as the NBN has neared completion of the original build, the Service Stream share price halved, with investors reducing the price earnings ratio from approximately 19 times future earnings to around 12 times. Driving the negative sentiment was the perceived earnings cliff associated with the NBN work ending.

In recent times however, the fortunes of Service Stream have started to improve. In late August, the company announced a new eight-year contract maintenance agreement with NBN. This was closely followed by the Federal government announcing it would spend an extra $4 billion on improving the NBN. This should placate in regard to an imminent earnings cliff.

In the meantime, the management of Service Stream has done a great job in diversifying the earnings of the company, expanding into the services of energy and water, both much larger overall markets than telecommunications. This now represents over 40 per cent of the company’s revenue. We would expect the company to push further down this path by using its strong balance sheet to make acquisitions in the non-telecommunication service areas.

While the company will always carry the risk of big chunky customers, the management team is best of breed and is working hard to grow earnings while mitigating overall risk. The financial 2021 year will be a consolidation year for the company’s earnings but with new contracts and growth in the non-telco areas, earnings should grow strongly from financial year 2022 onwards. With a price to earnings multiple of 14 times, we think it is worth owning.

Reece (ASX:REH)

Justin O'Brien, Cooper Investors

Reece is Australia’s largest distributor of plumbing products. We like the stock because it scores well in our VoF investment system, which favours companies with identifiable value latencies, positive operating, industry and strategic trends, and focused management behaviour.

Reece’s value latency (V) is all about the opportunity for long-term compounding. Two years ago Reece acquired US-based Morsco. Although offshore M&A can be risky, Reece has the opportunity to help consolidate the more fragmented US market with potential for years of capital deployment and growth. Over time this should lead to further scaling and improved profitability. The compounding achieved by other US distributors like Watsco, Poolcorp, Fastenal, and W.W. Grainger, are useful references.

We also think the odds of successful execution are further improved by backing a ‘proprietorial’ management team (F). As majority shareholders, the Wilson family has been at the helm of Reece for the last 50 years. The best ‘family-linked’ companies bring with them an enduring mindset. In Reece’s case many seemingly small decisions – owning rather than leasing property, over-investing in inventory to avoid stock-outs and higher levels of IT spend versus peers, collectively explain why Reece takes most of the industry’s profits in Australia.

But even the best management teams can still struggle if operating trends (O) are unfavourable. The elephant in the room for Reece is Australia’s housing cycle – will this soon end? One thing the pandemic demonstrated is plumbing is essential and Reece remains focused on the more resilient segments (maintenance, heating & cooling, civils). However, the positive trends in the US are arguably now more important. Despite the pandemic, new housing demand in the US is strong, underpinned by ultra-low mortgage rates and an underbuild of new houses since 2006.

When the three VoF factors come together, reinforce and support each other, we get excited!

The Reject Shop (ASX:TRS)

I’m a subscriber to the theory that companies exhibit life cycles. Inception, growth phase, operational plateau then a decline in fortunes. Examples of life cycles abound. Turnarounds are the next stage but sadly most don’t turn.

The Reject Shop is a classic turnaround play with sufficient levers to ensure a major earnings revival is given every chance of success. It currently operates ~350 stores Australia wide selling discount variety goods in neighbourhood shopping centres.

First, a seasoned new Chairman joined the board last year. Veteran discount variety retailer, Andre Reich, then assumed the CEO role. A new C-suite and general management were installed in the business. Head office was right sized and a new corporate maxim was born- Fix. Reset. Grow.

Second, equity was raised in February this year with longstanding bankers, ANZ, appeased. Management then moved to remove cost and simplify the business. SKU’s are being managed down from 12800 to 4000 units. Across the property lease book, an average two year tenor suggests better rental terms might not be too far away.

Third, operating ratios for each store have emerged as a major focus area, including inter alia, wages/sales, rent/sales, stock/store, stock turnover and shrinkage levels. Supposedly these metrics had been bent out of shape for eternity. To this end management strongly believe each store can be run with McDonalds-like efficiency.

Management have been busy with several sales initiatives with the recent exclusive Tesco deal an early look-in on the inventive merchandising strategy in play.

Valuation on a FY21 EV/EBITDA of approximately 6.0x appears reasonable for this retailing comeback.

Lendlease (ASX:LLC)

Blake Henricks, Firetrail Investments

Lendlease is an integrated real estate developer and manager, with leading positions in Australia and overseas.

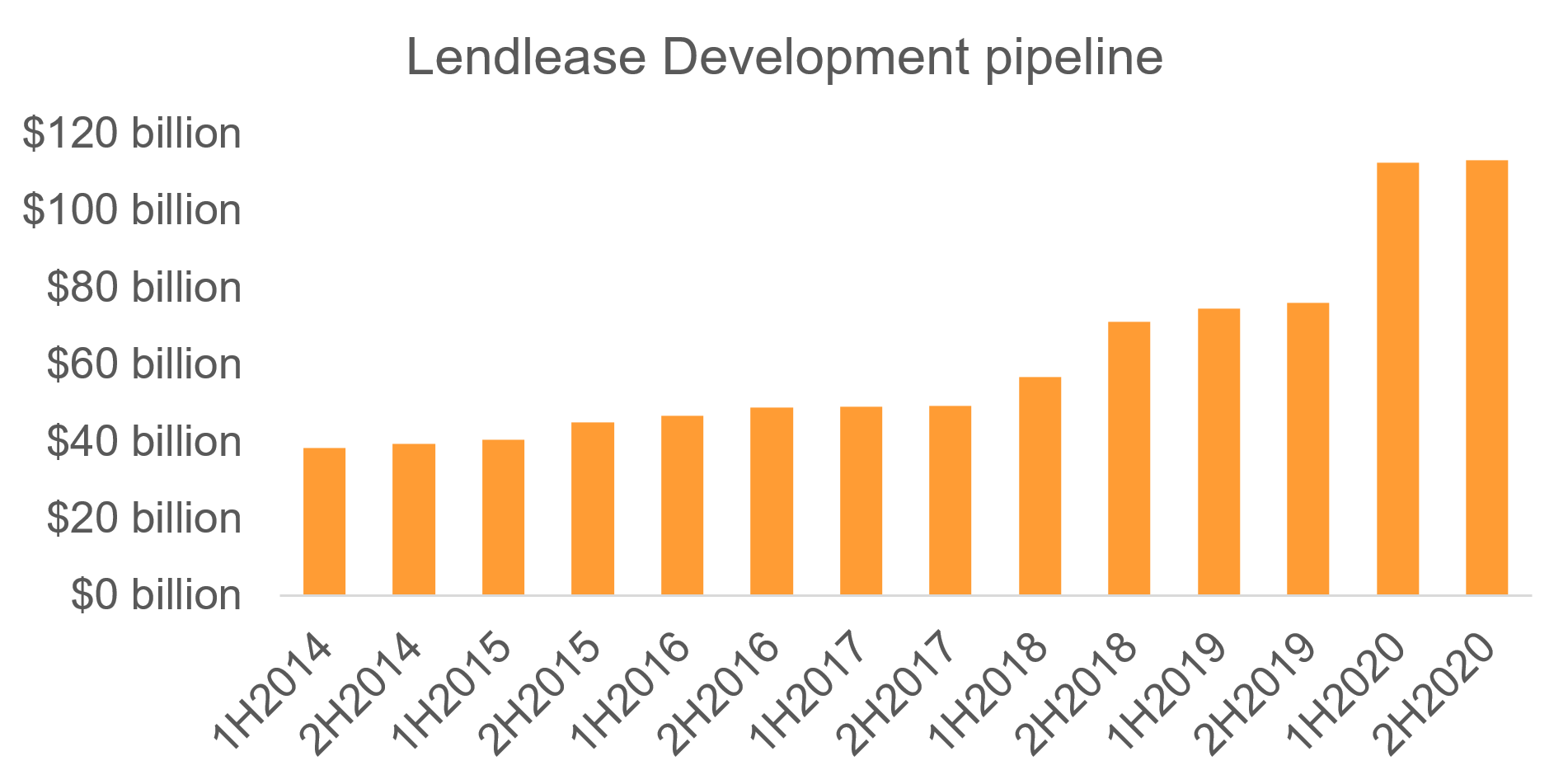

The opportunity in Lendlease comes by way of the market’s focus on the engineering division of the business which has lost more than a billion dollars for shareholders. But that is in the past. Lendlease has since sold the majority of the division, which was small relative to the rest of the company.

Lendlease is a market leader in global development of residential, office, and mixed developments. The company has grown its pipeline from $40b to more than $100b since 2014. Lendlease is also increasingly moving towards an investment management model, which produces high-quality, recurring revenue streams. Today assets under management (AUM) are less than $40b, but we see potential for AUM to be $100b in the coming years. Lendlease was de-rated on short term concerns. But it has strong businesses with massive growth potential, and our valuation forecast provides a lot of upside.

The biggest risk for Lendlease is conversion and execution of their $100b pipeline of opportunities. Somewhat mitigating this risk is the quality of the projects and project partners such as Google in San Francisco Bay.

Source: Lendlease

Worley (ASX:WOR)

Amar Naik, L1 Capital

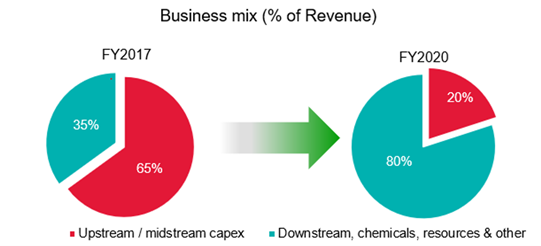

Worley is a leading global provider of professional project and asset services in the energy, chemicals and resources sectors. Worley has a worldwide team of ~50,000 consultants, engineers, construction workers and data scientists that are focused on solving complex problems for a range of multi-national clients.

Worley shares are trading ~30% below pre-COVID levels due to the significant fall in the oil price earlier this year and concerns over COVID-19 restrictions leading to a subdued recovery in oil demand. We believe Worley is an attractive investment, as the market incorrectly perceives the company as a direct exposure to the oil and gas industry, while greatly underappreciating the flexibility of its engineering consultancy led business model and the diversified nature of its operations. Worley is trading on only 13.5x consensus FY21 earnings which is a substantial discount to its 3-year average multiple of ~18x and is on a depressed earnings base impacted by COVID-19.

We believe Worley is much more comparable to a global engineering consultancy business than a lump-sum contractor. Worley derives ~80% of its revenue on a reimbursable basis, with only ~20% of revenue directly exposed to upstream/midstream oil and gas capex (post the ECR acquisition), down from ~65% previously. This has allowed Worley to proactively manage staff utilisation levels and deliver resilient FY20 earnings that demonstrated margin improvement, second half earnings in line with the first half and strong growth in cash generation despite the impacts of the oil downturn and COVID-19. Worley management have a history of strong delivery on prior cost out programs and have initiated a further $275m cost out program (26% of FY20 EBITDA). While the near-term revenue outlook may be more subdued, we believe the significant cost out program and streamlining of operations positions the company well to deliver margins ahead of consensus expectations and to take advantage of an improvement in the capex cycle as global growth recovers.

The main risk is further COVID-19 related restrictions or large declines in business confidence that extends global economic weakness.

Worley's exposure to

upstream/midstream oil and gas capex has reduced substantially

Source: L1 Capital analysis, Worley FY20 results presentation

Life360 (ASX:360)

Marcus Hughes, LHC Capital

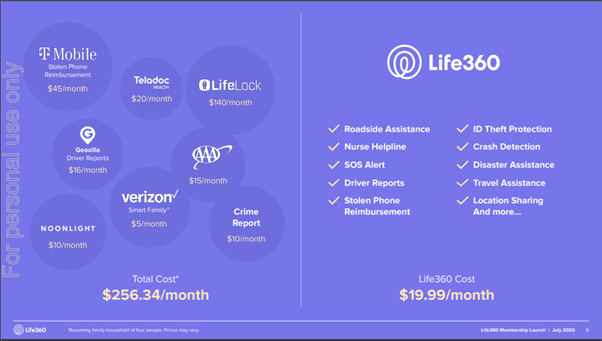

Life360 provides family safety services delivered through an app to a large, highly engaged, and fast growing user base. 360 has done extraordinarily well to position itself as the global leader in a massive market despite historically having limited access to capital. The company has a wonderful and passionate management team and the company’s listing on ASX has given it financial resources to further accelerate its R&D and customer acquisition programs. 360 has formed a new product category and has dominant market share with ~30 million active users. Adoption has grown virally, and we believe the family safety category is supported by strong and durable secular trends.

The recent launch of membership will be a major tipping point in the history of the company. Membership will result in 360’s product offering being extended and additional value provided to a broader range of users. We expect this will result in a further increase in the company’s TAM, a reduction in churn rates whilst delivering a significant improvement in yield at very high incremental margins. The company’s product strategy is compelling and demonstrates that they are seeking to develop a value proposition that extends to all stages of a family’s life.

Whilst the company is experiencing fast growth and is appropriately funded to reach profitability, 360 is presently loss making and consuming cash. 360 is dependent on Apple and Google app stores for distribution and is required to pay away in accordance with app store fee schedules. Potential competitors may emerge to compete with 360 which could increase churn rates or impact the rate of user base growth.

Life360 membership delivering compelling value to users

Source: Company presentation

Sydney Airport (ASX:SYD)

David Moberley, Paradice Investment Management

The prospect of shut international and domestic borders, resulting in the effective grounding of the global population was unimaginable and unprecedented, until the onset of the highly contagious and unpredictable Covid-19.

We view this as a rare opportunity to invest in Sydney Airport – a high quality, well run, near-monopolistic asset which is unregulated with a long-dated concession expiry in 2097.

We like SYD for the following key reasons:

- Evidence of recovery in other geographies – Inherently the desire to travel the world is strong, with aviation demand bouncing back quickly post shock events such as 9/11 and SARs. We believe this time will be no different when borders reopen, and people feel safe to travel. In China where Covid-19 was brought under control quickly, there has been a swift recovery with domestic passenger numbers bouncing back from -95% in April to -5% in the last two weeks of September. Corporate travel has also rebounded quickly to pre-Covid levels, with businesses, especially SMEs keen to visit clients, suppliers, and team. In NZ where Covid-19 was almost eliminated, domestic traffic recovered quickly to -37% vs pcp in July before the lockdowns resumed briefly in August. With Australia regaining control of the Covid-19 outbreak, we believe there will be strong pent up demand once borders reopen as people seek to visit family and friends, and holiday interstate. The resumption of international traffic will likely take longer and be more uneven, however we are cautiously optimistic that effective diagnostic and treatment solutions, and potentially the development of a vaccine will see a recovery emerge faster than what has been priced in.

- Strengthened balance sheet - Post the $2b equity raising in August, SYD has strengthened its balance sheet to weather an extended period of volatility. As of June 2020, it had access to $4.6b liquidity, sufficient for four years of minimal aviation activity. Credit agencies have adopted a pragmatic approach towards its credit rating and will look through the next two to three years as long as there are signs of recovery. With high EBITDA margins close to 80% and low maintenance capex, we believe it is well positioned to restore strong cashflows and distributions, particularly attractive in a low interest rate environment.

- Valuation is attractive. We believe the SYD share price assumes a four to six year recovery period, which we think more than adequately compensates investors for uncertainty in the timing and path of the recovery.

Key risks associated with an investment in SYD include:

- Technology and structural changes in behaviour – the widespread adoption of video conferencing may replace a proportion of business-related travel (SYD has 15-20% exposure), however we would highlight that inventions such as email and cheaper roaming costs have done little to change travel habits.

Johns Lyng Group (ASX:JLG)

Chris Prunty, QVG Capital

Johns Lyng is a building services company with particular focus on repair and restoration of residential and commercial properties for insurance clients. Johns Lyng also has a small but growing strata management business.

Johns Lyng is our largest holding and a company whose defensive growth and unique culture is under-appreciated by the market. At QVG we look for Quality, Value and Growth characteristics in stocks. Johns Lyng is high quality meaning that it generates strong cash flow and high returns on capital with low gearing. It grows revenue and earnings in the mid-teens organically and tops this up with bolt-on acquisitions. The valuation is fair for a company with such strong organic growth and quality characteristics and see potential for further valuation upside should the company make acquisitions in its strata division.

The company operates in an unglamorous industry with seemingly low barriers to entry. We think their strong history of organic growth is driven by a unique culture which is hard to replicate. A third of the company is owned by the board and management and divisional managers get paid a 10% profit share on the profit of their businesses. Johns Lyng has a culture that identifies, nurtures and rewards talent. The company also benefits from a fragmented competitor set and customers – mostly insurance companies – who like to deal with a national player with a track record of excellent service and ability to respond to catastrophic events quickly wherever they occur. We expect the company to continue to grow in the mid-teens organically. This growth will come from replicating their market share in Victoria in their core business across NSW and QLD and by offering building services to their strata customers.

While a season of no fires, floods or storms would be good for the country, some of Johns Lyng’s revenue comes from responding to such events.

ALS Limited (ASX:ALQ)

Jovita Khilnani, Regal Funds Management

One of our high conviction positions is ALS Limited, a global provider in laboratory testing, inspection and certification services to multiple industries including the mining, environmental, food, pharmaceutical, and industrial sectors. We see compelling upside due to the following key factors:

1. Minerals division set to benefit from a boom in minerals exploration spend

ALS commands a market leading position in its Minerals division (~50% of FY19 EBIT), specifically in Geochemistry, which involves the testing of core samples obtained from exploration drilling. Gold and copper represent ~50% and ~20% respectively of total mineral exploration spend globally. With the USD Gold Price recently surging to record highs, it looks like the stage is set for another boom in exploration spend. The last boom in CY12, saw global non-ferrous exploration spend peak at US$22bn compared to an estimated CY20 spend of only US$7bn. Whilst the higher gold price is yet to translate into more work for ALS, the recent spike in junior mining equity raisings gives us confidence that this will occur, albeit with a lag.

2. Currency and market share movements add further tailwinds

For ALS, this upswing in activity has the potential to produce a material uplift in earnings. During the FY12 peak, for example, ALS made A$215M in EBIT from its Minerals division, versus just A$158M in FY19. Given ALS earns most of its revenue overseas, adjusting for the lower AUD against its key currencies (USD, CAD, EUR) since the previous peak in 2012, we would estimate the A$215M FY12 EBIT becomes ~A$280M on a like-for-like basis. This essentially implies that a return to peak exploration levels of 2012, could equate to growth of ~80% versus FY19 levels for this part of the business. Further, market share gains, if held, could represent another leg of upside, given ALS’ market share today (est 45%+) is materially higher than in 2012 (est 30-35%).

Lastly, with the Life Sciences division (~40% of FY19 EBIT) also expected to recover and deliver robust growth, the growth prospects for the group could track materially ahead of market expectations over the medium term.

Key risks include a second wave of COVID-19 cases globally affecting ALQ’s operations, whilst persistent weakness in the gold price or equity markets could dampen capital raisings, impacting the exploration recovery.

Corporate Travel Management (ASX:CTD)

Kelli Meagher, Sage Capital

Corporate Travel Management provides business travel management services for companies globally. Its suite of technology tools makes it easier and cheaper to book flights, accommodation and generally manage staff travel.

Like all companies related to travel, CTD has suffered a huge hit in earnings and share price since the global pandemic began. However, we believe the worst has now passed. With COVID-19 case numbers more manageable, a vaccine on the horizon and wide-spread rapid testing increasing, including at airports, the world will likely start adopting more of a “live with it” approach. As restrictions ease and people become more confident about travelling, they will be more inclined to finally take that business trip, as there is only so much you can do over Zoom. In addition, companies will need corporate travel management services more than ever before to navigate what is likely to be a more complex “new normal” travel environment.

CTD also stands to benefit from industry consolidation. The global corporate travel market is highly fragmented, with many small and medium sized players who are currently under financial pressure and looking to sell. With its strong balance sheet and experienced management team, CTD is in prime position to take advantage of these opportunities. The company has a good track record of both organic growth and integrating and extracting value from acquisitions. It recently made a large acquisition in the US which complements its existing business and significantly increases its scale. This will allow them to add more customers to their existing technology platform, which means higher margins and a strategically stronger position to win new clients.

Obviously, the trajectory of COVID-19 and the timeline for a successful vaccine is unpredictable. Prolonged restrictions on travel within country and internationally would slow down CTD’s share price recovery, but with its flexible cost base and strong balance sheet, CTD is well placed to ride out any bumps along the road to recovery.

Boral Limited (ASX:BLD)

Gabriel Radzyminski, Sandon Capital

BLD is an international construction materials and building products group with three divisions: an integrated construction materials business in Australia; a plasterboard joint venture in Asia, Australia and the Middle East; and a building products and fly ash business in North America

BLD has delivered poor shareholder returns for many years resulting in pressure on the company to divest its troublesome North American assets. This has led to the departure of the CEO and several Board members. A new major shareholder has secured two board seats and is likely to be a significant catalyst for change at the company.

The Australian construction materials business (aggregates/cement/concrete) is a high-quality business. BLD's aggregates quarries hold privileged positions close to major metropolitan markets, a position that competitors cannot easily replicate. The market does not fully appreciate Boral’s pricing power on aggregates, partly because Boral has not acted as an industry leader. The Australian construction materials business should trade at 8 – 10x EBITDA, which represents a significant uplift from prices currently implied by the market.

Other value in Boral that has been overlooked are its property assets and landfill royalty. We conservatively estimate these are worth $1bn (80 cents per share), possibly more.

We believe BLD’s Australian operations have significant tailwinds arising from government focus on infrastructure spending to assist the economy’s recovery from COVID-19.

Even if the North American assets are sold, Sandon Capital believes Boral still needs to focus on improving the performance of its Australian operations as well as exploring ways to unlock the value in its property portfolio. To that end, we recently made the argument for the functional separation of the combined Australian property assets and the landfill royalty from the core Boral Australia segment.

If BLD can sell its North American assets for a reasonable price, run its Australia construction materials business better and optimise the value of its property and landfill royalty, we believe the shares could be worth >$8.

Potential risks include construction activity in Australia and the US, levered balance sheet (which can be cured by asset sales), FX and commodity price movements, industrial disputes, continued poor capital allocation and mismanagement of assets.

Aroa Biosurgery (ASX:ARX)

Jun Bei Liu, Tribeca Investment Partners

Based in Auckland, Aroa manufactures and sells surgical products to improve the healing of complex wounds and soft tissue reconstruction. The company’s proprietary platform, endoform, is derived from sheep forestomach and is supplemented with synthetic polymers, which gives it the ‘best of both worlds’ of both biologic and synthetic products. It comes as a ready to use structure that supports healing.

Since its founding in 2008, Aroa’s core technology has gained regulatory approvals in 37 countries (including from the US FDA). It has five patented products already selling in the US and over four million procedures have been performed with Aroa products globally.

Aroa is an exceptional growth story. It is at an early commercialisation stage of its product portfolio and has already delivered impressive revenue growth as its products gain a foothold in the large US market.

Aroa is currently generating revenue of $22 million which we expect to compound by at least 50% annually over the next three years. Aroa’s current approved products have a combined market opportunity of US$1.5 billion in annual revenue. With its strong distribution networks as well as a growing body of clinical data supporting the effectiveness of its products, our view is that Aroa will accelerate its market share gain in the coming years. Further, Aroa has more products in the pipeline which will grow the total addressable market opportunity to US$3 billion annually.

Aroa has performed very well since its IPO in July. It’s list price was $0.75 and the share price is up more than 70%. We continue to expect significant share price outperformance in the coming years as the group’s products makes inroads into the large wound healing and hernia markets.

Compared to its larger listed peer, Polynovo (ASX:PNV), Aroa is only trading at a fraction of the valuation of its larger listed peer Polynovo despite having a potentially larger market opportunity and established clinical data. We also would not rule out the potential for the company to be acquired by a larger player given the strength of its portfolio and the ultimate size of the opportunity.

Like many healthcare companies Aroa has been impacted by COVID-19. We view this as a temporary setback given the pandemic will have no long-term impact of the long-term demand for Aroa’s products.

Insurance Australia Group (ASX:IAG)

Matthew Haupt, Wilson Asset Management

Insurance Australia Group Limited () is the largest general insurance company in Australia and New Zealand, selling consumer and business insurance products under many leading brands.

Record low interest rates and the coronavirus pandemic have severely impacted the financial sector, however we believe significant opportunities will emerge as the economy stabilises and the macro trends move to tailwinds from the current headwinds.

Financials have underperformed for the last 12 months with low interest rates, poor economic conditions and a flat yield curve. In response to the pandemic the Reserve Bank of Australia (RBA) cut the cash rates, also pushing the three year rate to 25 basis points to match the cash rate.

As economic conditions improve, we believe the RBA’s first act will be to allow the three year rate to rise, providing relief to the financial sector and allowing investment income to improve gradually.

While Insurance Australia Group’s share price currently trades at decade lows, the recent appointment of a new Chief Executive Officer, a sound balance sheet and strong premium growth should see the share price recover. We believe that business insurance claims implied by the share price are overstated versus the reality and we expect clarity within a few months on this key catalyst.

Although business insurance and the closure of businesses through the coronavirus pandemic are a potential risk for the company, IAG is taking a very conservative approach factoring in these claims and we believe these will be significantly less than the market anticipates.

9 high conviction global picks

Click on the image to enlarge

Capital One Financial Corporation (US:COF)

Andrew Baud, Antipodes Partners

Despite having household name status in the US, Capital One (COF) is anything but common in investor portfolios. Emerging from nowhere 20 years ago, this dynamic business is today the fourth largest US retail bank by deposits with a stronghold in the subprime card and auto lending market.

COF’s visionary management is both disciplined and innovative, which has led to profits every year since listing in 1994. The firm has blazed trails in brand and product capabilities. A decade of having Samuel L Jackson and Jennifer Garner ask Americans “What’s in your wallet?” has catapulted COF to become the largest US card player with 50million accounts. Yet, 12 years after the 2008 financial crisis, “subprime” remains a dirty word and the stock’s current price reflects cynicism around the outlook for credit losses.

Antipodes is more optimistic. COF has a great record for pricing and risk management, best evidenced by reducing credit limits in August this year. The moat around the bank’s financials is deep, enough so to withstand GFC level loan write-offs whilst still allowing the distribution of half of its current market capitalisation through to FY23 and trading on 6x FY23 earnings (i.e. a 16%+ yield). There are growth opportunities too: the transition of COF’s workloads to the public cloud (AWS) in 2021 will deliver agility to further innovate product lines and significantly reduce overheads.

Possible changes to banking capital regulations following the US elections in November could pose a risk. Whilst a Trump win could result in further deregulation, a Biden win and Democratic senate majority may lead to regulation of consumer finance costs (which COF is well buffered to handle) and raise the hurdles for returning capital.

Source: Antipodes Partners, Capital One.

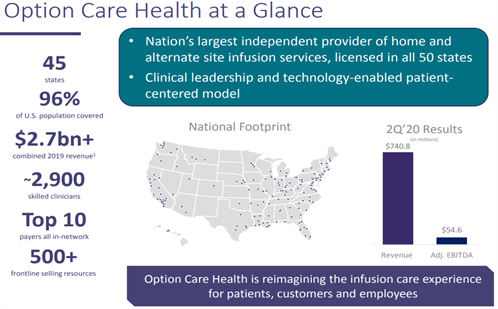

Option Care Health (NSDQ:OPCH)

Bill Pridham, Ellerston Capital

Option Care Health is the only scaled national provider of post-acute infusion therapy covering 96% of the US population with close to 3,000 highly skilled team of clinicians providing quality care generally at home or alternatively in one of its infusion suites located across the country.

The total US Infusion market is estimated at $100bn with only c13% of this currently administered at home despite obvious cost and patient care benefits. The industry is shifting to at-home care and we expect continued migration from a hospital or physician office setting to the home as patients prefer its convenience and reduced risk of infection while payers benefit from the significant cost savings associated with at home treatment.

In August 2019 OPCH became public through a reverse merger with a listed counterpart and the combination is delivering substantial cost and revenue synergies to the group. At the time of transaction, Management expected to generate $60m of run rate synergies within 18-24 months post-merger, however this has been realised much faster with full synergies realised within one year and over achievement of its synergy target expected from here.

We consider that OPCH offers long term durable growth opportunities as it offers a better patient outcome at significantly lower costs to the payers – basically a win/win. We expect it to deliver mid to high single digit revenue growth for the foreseeable future which translates into double digit earnings growth as the platform scales.

Private equity still owns c70% of the business and this is creating an overhang on the stock as the market anticipates further sell downs. OPCH is trading at a double-digit EBITDA discount to comparable companies as a result of this. As patient investors we look forward to further sell downs as in our experience this creates additional liquidity while concurrently reducing the overhang risk, both of which result in a higher multiple and significant capital appreciation to us as shareholders.

Source: Option Care Health Q2 Presentation

Alphabet (NSDQ:GOOG)

Kris Webster, Magellan Financial Group

Alphabet owns Google Search, YouTube, Android, Google Cloud Platform and five other global services that each have more than a billion monthly active users. Many of Alphabet’s businesses are dominant leaders in large global markets that should experience above-average growth for years to come. It also has several underappreciated opportunities.

Alphabet generated sales of US$162 billion in 2019, mostly attributable to Google’s success in capturing about 26% of global media advertising spending (ex-China) via Search, YouTube and its digital advertising technologies. Despite its market leadership, we expect Google to continue to take share of advertising from traditional media due to its superior targeting abilities and the high engagement of its services.

We think the market underappreciates several of Alphabet’s businesses that have considerable value and long growth runways, as they are most likely losing money at the moment. Google Cloud grew revenue by 53% to US$9 billion in 2019, and the business is likely to expand for many years as enterprises increasingly outsource their IT. Among the most promising of Alphabet’s ‘Other Bets’ is its self-driving car software, Waymo, that has the potential to lead the transformation of urban transportation.

Alphabet’s risks stem mostly from its success. Regulators have accused Google of anti-competitive abuses in search, digital advertising technology and Android. New privacy regulations and Apple’s policy changes could limit Google’s ability to collect data, reducing its ability to target ads. Over time, YouTube is likely to face tougher penalties for harmful content hosted on its platform. Governments are seeking to restrict Alphabet’s ability to shift revenue among subsidiaries to minimise its tax. It is spending billions every year on ‘Other Bets’, which are in industries typically distant from its core, and for which success is far from assured.

Spotify Technology (NYSE:SPOT)

Brandon Geisler, Marsico Capital

Spotify Technology is the global leader in digital music consumption and has transformed the way in which people access and enjoy all forms of audio entertainment. The company provides music streaming services and has over 300 million monthly active users in 92 countries. Spotify currently generates the large bulk of its revenue from monthly subscription fees, but we think that this is just the beginning of the way in which the company can monetize its substantial user base. We believe Spotify mirrors Netflix prior to gaining appreciation from the investing community, and that we are on the launch pad ready for the stock to take off.

We view the stock as particularly attractive as we believe that there are a multitude of growth drivers for Spotify that will materialize in the future, particularly in other audio formats. The company has recently made large investments in podcasts through exclusive deals with Barack and Michelle Obama, Joe Rogan, and others. We view this medium as a huge opportunity given the share shift away from terrestrial radio consumption. In 2020, annual advertising revenue for radio is over $50b and we see this as table stakes for Spotify to capture given 60 million users on the platform consume podcasts already. This potential leg of growth from advertising will diversify the revenue base, leading to material outperformance for the stock.

Potential risks to the stock stem around competition, particularly from Amazon and Apple. These formidable competitors have launched similar services to Spotify’s for a much lower cost. These forces could reduce Spotify’s growth through either less overall engagement or inability to maintain their pricing structure. We don’t subscribe to this theory, as we believe that Spotify’s relentless innovation and sole focus on audio will keep them well ahead of any competitive offering.

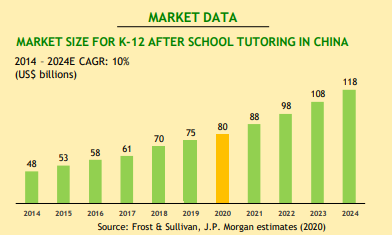

New Oriental Education & Technology Group (US:EDU)

Claudia Kwan, Morphic Asset Management

Established in 1993, New Oriental Education & Technology Group (EDU) is the largest provider of private educational services in China. The company offers a wide range of educational programs. It has had over 55 million student enrolments, operates 104 schools, has 1465 learning centres and 12 bookstores and employs over 41,400 teachers in 91 cities.

EDU is a long-term market share gainer in a growing market that near-term will benefit from the ‘reopening trade’ as their learning centres resume operations. The covid-19 epidemic accelerated their investment in an O2O (online/offline) learning model which we see as the ‘right’ learning model and key product differentiator to propel them ahead of competition.

EDU is a market consolidator beneficiary in a growing market with the best-known brand and the widest network footprint. The education market was undergoing market consolidation as a result of tighter regulations however Covid-19 has accelerated this trend as tough conditions have caused smaller players to exit.

The Chinese after school tutoring (AST) demand is expected to grow between 10-12% CAGR in 10 years to 2030 reaching a market size of almost rmb3 trillion, 3x the 2019 size. This is driven by China’s annual disposable income per capita that grew from rmb17K in 2009 to rmb42K during the 10 year period of 2009 to 2019, representing a 9.4% CAGR.

EDU will benefit from a rising middle class given that they have the widest learning centre network across different tier cities allowing them to capture the faster rate of growth of lower tier cities where teaching staff are less resourced. EDU are guiding to 20-25% capacity expansion per annum that will be a key driver top line growth. Rising utilisation rates and average selling prices will drive margin expansion and a strong upward trend in earnings per share.

Regulatory changes could negatively impact the economics of the industry. Competition from fast growing online players could erode industry profitability and cannibalise offline learning. Geopolitical risks associated with US ADR listings.

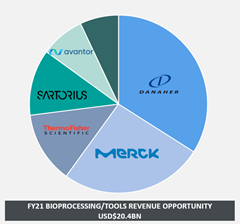

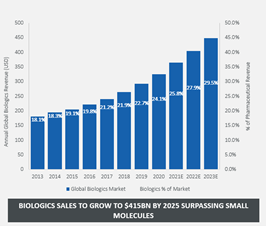

Danaher (US:DHR)

Jeremy Gibson, Munro Global Growth Fund

Danaher designs, manufactures and markets products and services in the sectors of life sciences, diagnostics testing and environmental sciences.

The end market exposure is very attractive given the structural growth and resiliency in an economic downturn. The business has very predictable cash flows given a high proportion of products sold are consumables that act as recurring revenue. The company has one of the best management teams and investment philosophies we have seen with their “Danaher Business Systems” (DBS) framework. Rather than grow margins by cost-cutting, the DBS process invests in innovation and aims to produce more innovative and therefore higher priced products to drive margin expansion.

Danaher’s recent acquisition of Cytiva (GE’s Biopharma business) has significantly increased Danaher’s exposure to life sciences and importantly their exposure to biopharma manufacturing. Even before COVID-19 this was an area of structural growth as the pharmaceutical industry was shifting from small molecule drugs to biologics drugs, as biologic drugs are more targeted therapeutics that come with higher efficacy and reduced side-effects. The arrival of COVID-19 gave the segment an added growth driver – COVID vaccine and therapeutic development and production.

Danaher is the global leader in supplying instruments and consumables to the biopharma manufacturing industry. We think COVID-19 could add an additional $20bn in revenue opportunity for the market. (see chart below). The rush to develop and build increased capacity for COVID-19 vaccines led to sales growth of >20% for Danaher’s operating businesses in this segment, up from a run-rate of high single digits. Investing in Danaher is like investing in the picks and shovel makers in the gold rush, rather than trying to predict which gold miner will strike gold. In this instance, the gold rush is towards cures for ailments such as COVID-19.

However, Danaher is an active acquirer, and this involves risks around integration that can lead to lower profitability or write-downs, should the company make an error in its acquisition strategy.

Given Danaher’s strong track record of creating value from acquisitions and the pipeline of growth ahead from both testing and biopharma manufacturing equipment demand brought about by COVID-19, we see many strong years of growth ahead for Danaher.

Danaher’s sales opportunities

Source: Frost & Sullivan, 30 September 2020

Source: Citi, 30 September 2020

HelloFresh (FWB:HFG)

Iain Fulton, Nikko AM

HelloFresh SE is an international, publicly traded meal-kit company based in Berlin, Germany. It is the largest meal-kit provider in the United States, and also has operations in Canada, Western Europe, New Zealand and Australia. As a disruptor in the highly attractive $7.5 trillion global food segment, in which e-commerce penetration is only 2%, HelloFresh has an excellent opportunity to grow its total addressable market.

We like HelloFresh because it is the leader in the fast-growing meal-kit market. It has created high barriers to entry through investment in data analysis and marketing, which allow it to effectively assess and respond to consumer demand. The company has proven resilient through the COVID-19 pandemic, highlighting the durability of its supply chain and a strong operating model. Additionally, it is well-positioned to address long-term consumer trends such as health & wellness and sustainability, which should drive long-term growth. Importantly, HelloFresh is committed to the UN SDGs, with a primary focus on reducing food waste. According to HelloFresh, its meal-kits contribute 66% less food waste on a production level compared to supermarkets.

HelloFresh has the Future Quality characteristics we look for in a stock idea. Committed to a data-driven approach that facilitates very lean inventory and flexible ordering, HelloFresh has a strong franchise quality. We have confidence in company management. In Q2, HelloFresh added 2.4 million customers to the platform and achieved an AEBITDA margin of 15.8%, highlighting the ability of management to generate impressive top-line growth and margin expansion hand-in-hand. Additionally, with strong cash generation and an undrawn credit facility, HelloFresh has the ability to cater to growing consumer demand. In terms of the valuation, we believe the total addressable market is underappreciated. Management is rolling out new price points to address different market segments and the marketing spend required to attract and retain customers will decline as a percentage of sales allowing margins to stay high. In light of this, we added HelloFresh to the portfolio at the beginning of Q2 and have recently added to our position.

A key risk to the investment thesis is that customer retention rates are not as high as we expect. Pent-up demand for eating out could result in higher churn off for meal-kits and HelloFresh may be forced to increase marketing spend to acquire and retain customers. However, recent evidence of higher number of orders and average order value per customer indicate that habit formation around meal-kits is proving to be more enduring.

Cash return on investment (%)

Source: Nikko AM, July 2020

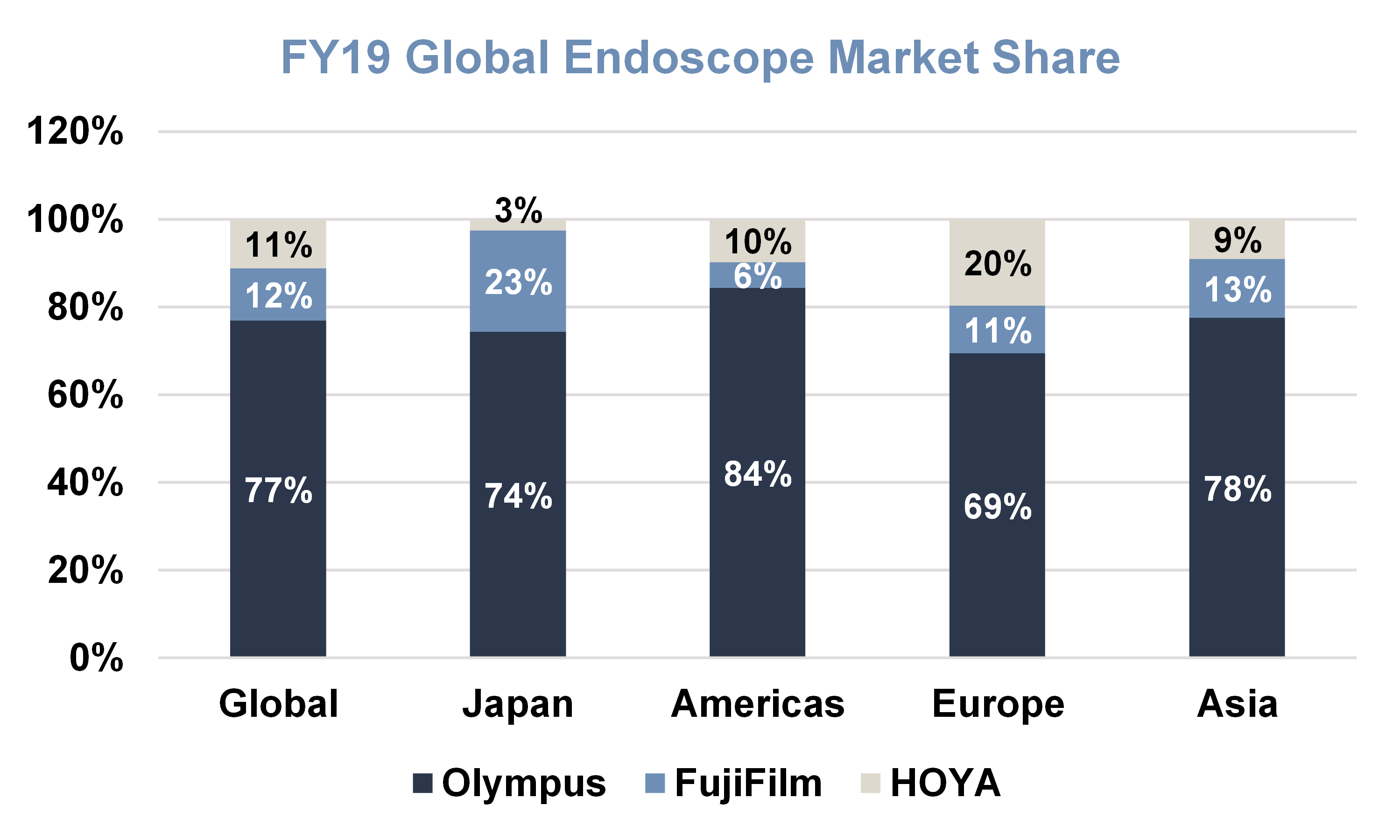

Olympus Corporation (TYO:7733)

Robert Luciano, VGI Partners

When you see the name “Olympus” you probably think of the iconic digital camera business. However, what is less well known is that Olympus was a pioneer in gastrointestinal endoscopes, which are long flexible tubes with a video camera used to screen for gastric and colorectal cancer. Olympus launched its first endoscope back in 1955 and has dominated the industry ever since. With a market share of around 70% today, endoscopes are the key driver of earnings for the business.

As with most medical technology devices, endoscopes require a significant amount of training for the doctors who use them. This leads to a high degree of loyalty, as a practitioner would have to retrain on a new control system if they were to change to another brand.

This is also a market with strong long-term growth. In developed countries, screening programs that use endoscopes are growing as the focus on preventative healthcare increases. In developing markets, the adoption of Western diets is increasing the prevalence of colorectal cancer, which in turn drives demand for endoscopes. China is a high-growth market for Olympus, while India has potential to become a significant market in coming years.

Olympus made headlines for a corporate corruption scandal in 2011; however, this is well and truly behind them and the company is now a corporate governance leader in Japan. They have quite recently appointed three foreign directors onto the board and have announced the divestiture of the loss-making digital camera business; these are both monumental changes for a Japanese company and we find them extremely encouraging. Last year management announced a value creation and transformation program with the aim of almost doubling the operating margin, which currently sits well below global peers.

We think Olympus is a very high-quality business, which is dominant in a highly consolidated and growing industry. There is tangible evidence to suggest management are intently focused on modernising the business and improving its efficiency. We think these factors will drive significant long-term earnings growth and attractive shareholder returns.

Source: Company Filings and VGI Partners Analysis

Louise Walsh

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Future Generation is an investment model that delivers more. We provide investment returns and real social impact by partnering with leading Australian and global fund managers, who generously waive all management and performance fees. This allows us to channel 1% of assets each year to Australian not-for-profits supporting youth at risk, youth mental health and the economic advancement of women – without compromising shareholder returns.

Featuring

Kelli Meagher,

Sage Capital

Kelli has over 20 years experience as an analyst and Portfolio Manager in the Australian and US equity markets across small, mid and large caps.

24 stocks mentioned

1 fund mentioned

16 contributors mentioned

Future Generation

Future Generation is an investment model that delivers more. We provide investment returns and real social impact by partnering with leading Australian and global fund managers, who generously waive all management and performance fees. This allows...

Expertise

Comments

Comments

Sign In or Join Free to comment