3 'speccy' uranium plays

The US Senate Committee on Environment and Public Works (EPW) has approved a bipartisan bill that advances the initiative to establish a US strategic uranium reserve. This is a clear positive move for the sector plus uranium from companies related to Russia or China being excluded has a positive impact on the Australian names looking to move forward in this volatile space which has never really recovered from the Fukushima nuclear disaster back in early 2011.

The US government is understandably concerned that it produces less than 1% of its own uranium demand and its reliance on imports from countries such as Kazakhstan, Russia and China don’t sit well. Hence, we saw the formation of the Nuclear Fuel Working Group (NFWG) in July 2019 to assess the entirety of the US nuclear industry. Since the formation of the NFWG, there has been steady progress supportive of domestic investment in the sector including the following decisions.

In Feb-2020 President Trump announced a US$150mpa buying program for a strategic uranium stockpile, ~2Mlb/yr for 10 years, an NFWG report released in April 2020 stated that “it is in the nation’s national security interests to preserve the assets and investments of the entire U.S. nuclear enterprise and to revitalize the sector to regain U.S. global nuclear leadership.” plus a NFWG Russian Suspension Agreement was signed in 2020 which effectively removed a significant impediment to US utility contracting and provides greater certainty for the market in general.

It’s likely the 20-year extension on the limits of Russian uranium imports will not only encourage mine and enrichment investment in the US but also force US utilities to adjust and reduce their dependence on cheap Russian supply, in summary, we should have increased US demand from countries like Australia.

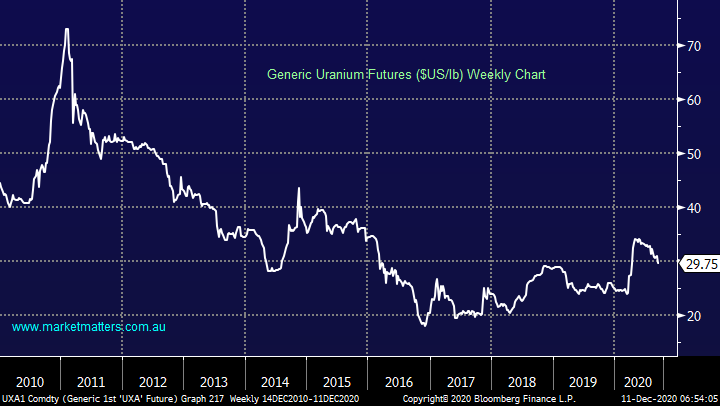

MM is bullish on the uranium space with sector risks skewed to the upside due to a lack of industry investment since 2011.

Uranium Chart

Hence if we believe nuclear demand is set to rise in the years ahead the question is do we see any solid risk/reward opportunities in an environment where we’ve already stated our desire to be long the reflation trade i.e. resources. Today I have briefly looked at the 3 largest uranium plays on the ASX which all fall very much in the “speccy” basket.

1. Paladin (PDN) 20.5c

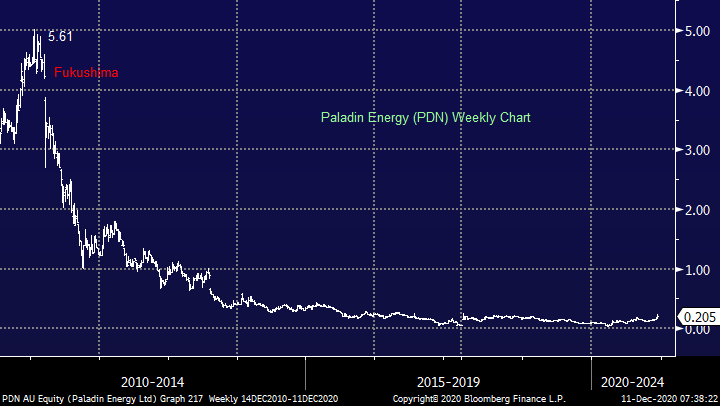

The chart below illustrates this $415m uranium business has endured a really tough time since the Fukushima disaster almost a decade ago but we do believe its now the standout of the Australian Uranium Sector on a risk/reward perspective based on a combination of uranium price leverage, underlying asset quality and project lifecycle phase. Paladin is preparing for a restart of the Langer Heinrich (PDN 75%) uranium mine in Namibia. In our view, the company needs spot Uranium around US$43/lb to re-start which is not out of the question if US demand continues to increase.

MM is bullish PDN around the 20c area with stops under 17c.

Paladin (PDN) Chart

2. Boss Energy Ltd (BOE) 8.1c

BOE is a $148m WA based uranium company that’s 100% owned fully permitted in situ recovery Honeymoon project in South Australia which requires low upfront capital (US$24m for 0.9Mlb/yr production re-start) and only 12 months to get going. BOE is the only company in today’s list whose key asset is in Australia, an important factor given the geopolitically sensitive nature of uranium. In our view BOE requires spot uranium prices ~US$45/lb in order to sanction a restart.

MM likes BOE and initially sees upside above 10c.

Boss Energy (BOE) Chart

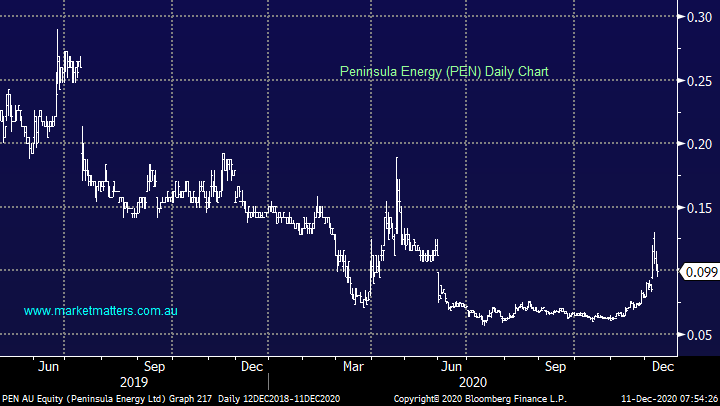

3. Peninsula Energy (PEN) 9.9c

Another WA based uranium exploration business but this time with a market cap under $90m but it’s the only company that has an existing contract book. The company’s flagship in situ Lance Projects (PEN 100%) in Wyoming, USA, requires low upfront capital (US$6m for 1.1Mlb/yr operations restart) and can restart 6 months post a Final Investment Decision. However, we believe the company requires a slightly higher uranium price ~US$48/lb for a restart. Importantly following the successful completion of a fully underwritten A$40m share entitlement offer in June, the company is term debt-free.

MM likes PEN with stops below 8c.

Peninsula Energy (PEN) Chart

Conclusion

MM likes the risk/reward the uranium sector offers the aggressive trader/investors, but we need higher spot prices before these mines become operational. Buying any of the companies is like buying a speculative call option on the Uranium price, so position size accordingly.

Get regular market updates

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them. Click here for your free trial.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 topic

3 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets