7 quality property and infrastructure stock ideas

Grant Mackenzie, Senior Portfolio Manager at Freehold Investment Management, summed up what’s unique about this crisis with a few, well-chosen words.

“We’ve never seen a government tell people to stop consuming.”

That simple observation is a big deal given retail spending accounts for 60% of the Australian economy. For property and infrastructure investors, the challenge is to navigate current conditions and extrapolate how the world will change on the ‘other side’ to work out the survivors and thrivers.

Mackenzie manages the Freehold Listed A-REIT & Infrastructure Fund and discussed the state of these asset classes and how Freehold is positioned at a recent webinar.

Caption: Grant Mackenzie, Senior Portfolio Manager, Freehold Investment Management

What’s happening in property?

In framing the overall issues on the property side of the ledger, Mackenzie said COVID-19 is different from the global financial crisis, which entailed stretched balance sheets and companies borrowing to pay “manufactured” dividends.

“This one is more a P&L issue where the real question mark is about the impact on incomes for a lot of these vehicles. Where will it be in the short term, how long will they take to come out of it and where will it settle going forward? I think they're the real challenges that people are struggling with at the moment.”

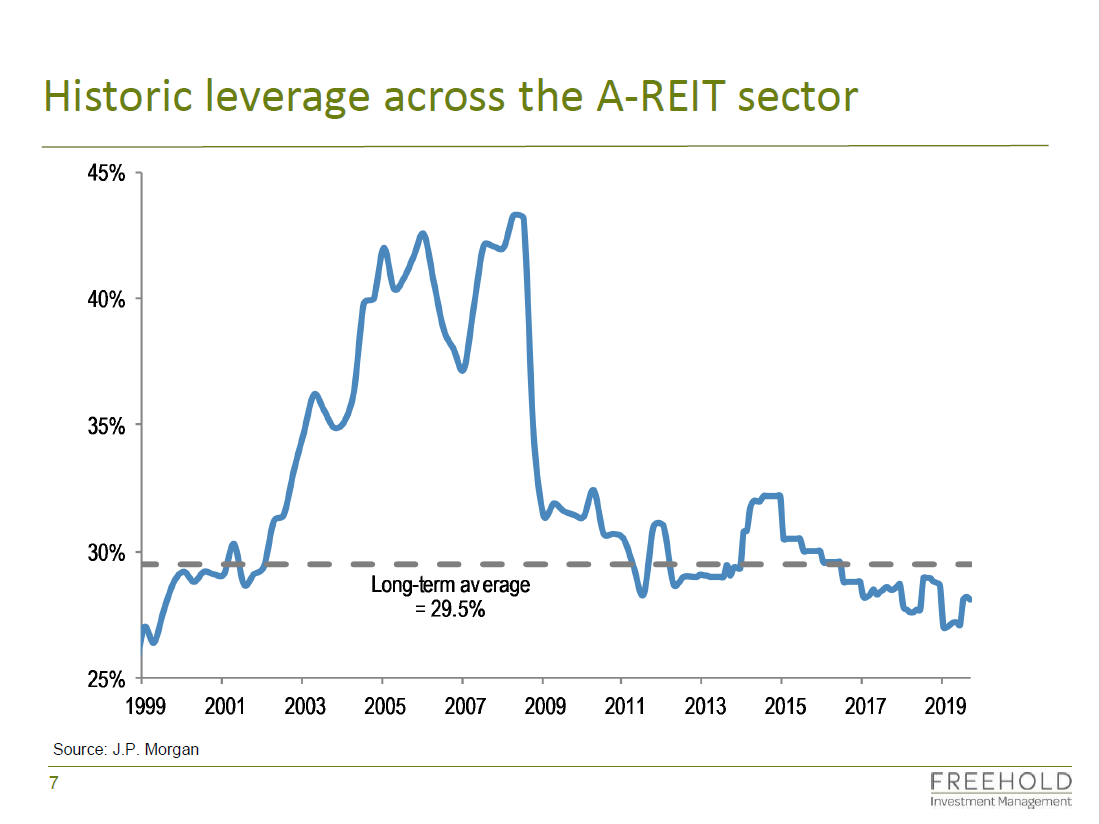

Leverage across the A-REIT sector at the end of 2019 was only 29.5%, compared to north of 40% during the GFC. Thanks to this level of conservatism, it doesn’t appear that any property stocks are about to breach debt covenants, nor are they crying out for capital. However, this could change as certain types of tenants start to feel the pain of the ‘stay-at-home’ economy.

For Mackenzie, his strategy is to focus on covenants and avoid value traps.

“We’ve had a massive underweight view on the retail sector for a while. I think retail has been undergoing some significant structural change over the last 5+ years where this 5% growth in rents every year, when sales are only going up 1-2%, have become quite unsustainable.”

In particular, foot traffic has plummeted at large department stores such as Myer (ASX:MYR), David Jones and other fashion retailers, threatening the viability of some of these businesses and exacerbating the shift to online shopping. As a result, “rental abatements are inevitable” for landlords with a large proportion of discretionary outlets in their tenant mix.

“I think what's happened over the last month is just going to accelerate that change in social behaviour and how these malls are positioned.”

The office sector’s prospects are also questionable, with employers and employees realising that working from home on a sustained basis is possible and productive, thus putting the value or need for renting office space in question.

“The office sector is one where I think people's initial reaction was ‘that'll be relatively immune from this’. But I don't think they are totally immune. While I like being in the office, you just wonder if this really does change people's behaviours.”

3 A-REITs to consider

Mackenzie, whose fund outperformed by nearly 9% in March, provided a snapshot of his positioning and the stocks he bought and sold in March below. The key with A-REITs is to be selective and buy only those assets providing surety of cash flows backed by long-term structured leases and high-quality tenants.

He provided a thesis for the following:

- Shopping Centres Australasia (ASX:SCA) – While this is a retail A-REIT, it’s important to distinguish that it owns a portfolio of neighbourhood shopping centres anchored by Woolworths (ASX:WOW), Coles (ASX:COL) and 10-15 speciality stores.

"I think you're seeing a lot of the retail traffic from the city and other locations and the malls really be directed back into these local supermarket anchored shopping centres. So, a pretty safe place in our view to the park our capital."

- Goodman Group (ASX:GMG) – The boom in e-commerce will underpin Goodman Group, whose properties play a key role in the logistics supply chain for these products.

"You're just going to see that e-commerce thematic continue and industrial is just going to continue to be one of the asset classes that investors really want to get access to."

- Viva Energy Retail (ASX:VVR) – Which dropped to a circa 8% yield during the March sell-off and is now mispriced. It owns over 600 service stations around Australia on 12-year leases to major energy powerhouse Shell.

“You could accumulate your dividends over the next 10 years and then basically get your money back. And even if they pull out at the end of the lease, you're left with over 600 assets around Australia that you'll own outright. To us there's very, very little risk in owning something like that over the medium to longer term."

4 infrastructure stock ideas

As for the infrastructure side of the equation, Mackenzie is taking a similar approach: buying quality assets that are either unaffected or have ample buffers to get to the other side. He laid out his thesis for the following names:

- Sydney Airport (ASX:SYD)

"It's a great asset, it's a monopoly asset and their balance sheet and their liquidity is in good shape as well."

- Transurban (ASX:TCL) – Australia’s largest toll road operator has done a “fantastic job” in securing ample liquidity to continue with its ongoing construction programmes as well as running the business.

"They've revised their distribution guidance to pay out their revised level of free cashflow, which is obviously going to be impacted by the lower traffic numbers out there, but that's okay. I think that's a very sensible approach. And as you can see there, their weighted average expiry for their debt is about 8.4 years."

- APA Group (ASX:APA) – The natural gas and electricity heavyweight has 90% of its revenue regulated and 93% of its customers are high-quality corporates.

"The crux of what the market was really valuing through March is the quality of the revenue and the likelihood that that revenue is going to be sustainable and not impeded through the period."

- Spark Infrastructure (ASX:SKI) – A similar case with Spark Infrastructure, which operates poles and wires infrastructure.

"You look at who the counterparty is paying the revenue and regulated growth, not the most exciting story, but in markets like this people are more than happy to own these things knowing the level of certainty involved with the returns."

To sum it up

In his conclusion, Mackenzie said markets are expected to remain volatile and investors would be best served by staying defensive, focusing on quality and not catching falling knives.

A careful analysis of the balance sheet, debt levels and liquidity should be undertaken to ensure that companies can survive, continue to pay predictable income and emerge from the crisis in a stronger position.

Access the full recording here.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Featuring

Grant Mackenzie,

Freehold Investment Management

Grant MacKenzie is the Senior Portfolio Manager for the Freehold A-REITs & Listed Infrastructure Fund. His responsibilities incorporate portfolio construction, co-lead real estate and infrastructure securities analyst and a member of the investment committee.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

4 topics

10 stocks mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment