A retest of the March lows? The bears are kidding themselves

In Why you should fear the big bad bear my colleague Patrick Poke and popular Livewire contributors Jerome Lander, Kate Samranvedhya, Anton Tagliaferro and Donald Amstad made a compelling argument about why the market's sharp rebound is too good to be true.

The possible re-imposition of economically crippling lockdowns, soaring unemployment, fiscal/monetary policies supporting zombie companies and, as Kate highlighted, governments are now "in a super debt cycle – on turbo”. All scary stuff; they certainly have valid reasons to worry.

But as they say, differing views make a market. Here, in part 3 of Livewire's exclusive Bulls vs Series, three bullish experts will contest why despite the bears' negativity, markets will continue to transcend the "wall of worry". Read on for views from Emanuel Datt, Managing Director at Datt Capital; Jun Bei Liu, Portfolio Manager at Tribeca Investment Partners, and Shane Oliver, Chief Economist at AMP Capital on why markets will keep charging higher.

Why markets won't collapse again

The sharemarket’s behaviour is certainly difficult to fathom. On March 23, the S&P/ASX 200 fell to 4403 – its lowest point so far this year – and investors sold out at a rate of knots. Since then, despite there still being no COVID-19 vaccine and with the economy under great stress, the market has rebounded, rewarding those who bought in March.

Our bulls are adamant a major relapse is unlikely to happen, at least in the short term, largely because of the huge amount of cash sitting on the sidelines. Emanuel says those who were cashed-up or went to cash when the downturn occurred, did not increase their equity exposure at the opportune time and missed out on the subsequent recovery in equity markets. Therefore the cash is still available to support the market.

“We also believe the market has already digested the worst news,” he said. “For the market to retest its lows, unexpected and materially dire news would need to occur, such as a sudden withdrawal of government support and subsidies.”

Indeed, the federal government’s income and debt-deferral initiatives have been key in keeping the economy afloat and the government has stated it will do whatever it needs to, to support the economic recovery.

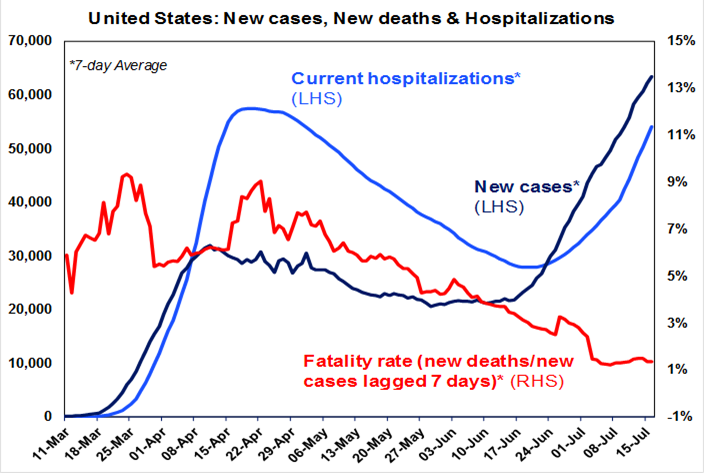

Shane from AMP says there is a number of reasons why we’re unlikely to see the market revisit its March lows, with one being the positive news on the health front regarding treatments for COVID-19. “While hospitalisations and deaths are escalating in the US, both are continuing to run proportionally well below what was seen in the first wave,” he says. “The fatality rate of new cases is still running around 1% compared to around 7% in April.”

Source: The COVID Tracking Project, AMP Capital

Shane also attributes China’s improving economic activity – which is a support for Australia’s export earnings – and the ongoing downtrend in the “safe haven” US dollar and rising commodity prices (with metal prices back to their pre-coronavirus levels), as evidence the market strength is here to stay.

“Easy monetary and fiscal policy is also continuing to support markets in contrast to the situation when the first wave started in developed countries in late February,” Shane says. “There is still lots of cash sitting on the sidelines, and investor sentiment is cautious, all of which provides some support for the market.”

Source: AMP Capital

Shane says another way of looking at the situation is to consider COVID-19 and its impact on the economy back in February and March – when shares plunged – was a big new unknown and there was nothing to offset it.

“Now we know that it can be contained; that this does not need an indefinite shutdown, that there is hope for medical solutions and that the government policy response is providing a huge offset. None of these things were evident or in place in March," he said.

Meanwhile, Tribeca’s Jun Bei says she can’t see the markets reverting because earnings in many lockdown-affected sectors, such as retail, will be stronger than expected.

“While some of the stimulus payments have been spent through various channels as consumers were forced to stay at home, a lot of it hasn’t yet because the country has been in lockdown,” she said. “As some of those restrictions ease in the next few months, we will see more spending coming through, particularly as we are also expecting the government to increase stimulus through the Jobmaker program.”

Are credit markets/bonds telling a different story?

Analysing what is happening with bonds and credit markets is generally a good indication of where equities are heading. At the moment, credit yields have declined from their March highs, just as shares have rallied, so according to Shane, bonds are not telling a different story – they are just reflecting different parts of the same story.

“Bond yields remain low despite the rally in shares and credit but bonds often lag in the initial recovery,” he said. “Shares have moved higher on the back of the fiscal stimulus, ultra-easy money, low interest rates and bond yields boosting the fair value of shares, and signs of recovery and hopes for a medical solution.”

But he says bond yields are being kept down by massive amounts of spare capacity in factories and labour markets – that is high unemployment.

“This points to ongoing very low inflation at the same time as central banks appear set to keep short-term interest rates down for a long time,” he said. “Many central banks are also buying bonds, which has the effect of keeping their price up and yields down.”

Source: AMP Capital

Credit markets are currently skewed by a record low interest rate environment and accommodative monetary policy – and the hunt for yield in real terms has led to compressed corporate debt yields despite larger financial risks.

Emanuel says government intervention in the sovereign debt markets has caused an influx of capital chasing yield in the private debt markets, despite larger risks resulting from COVID-19-induced business conditions. “It is very difficult to justify the risk/reward equation on offer in today’s credit markets. We have seen a number of corporate bond issuances lose portions of their principal recently, and we believe the risk of default remains elevated," he said.

Justifying the valuations on risk assets

Low interest rates and extreme levels of liquidity have boosted valuations, leading to calls by our bears that the market is overvalued and a market decline must be on the cards. But Tribeca’s Jun Bei says there are two elements to this argument: how you value growth assets and the lower bond yield.

"There is plenty of cheap money around the world at the moment and it should theoretically push up asset prices, equities included: that’s one element," she said. "The second is that, as an asset class, equities offer rare dividend return and capital growth opportunities in today’s world."

While value investors often comment that some of the growth sectors are too expensive, Jun Bei says the fact is that analysts often are not great at estimating future earnings appropriately, and that is partly why high-growth businesses look perpetually expensive.

"Now, with lower returns across almost every asset class, there is so much money going after assets that can generate above-trend structural growth and this makes those assets much more valuable compared to a year ago. Over the next few years, returns are going to be very difficult to generate and growth is going to be very difficult to find," she said.

Emanuel agrees the current depressed interest-rate environment is conducive to elevated equity prices as investors hunt for returns. “Cash in a bank account or invested in a nominally ‘safe’ asset like a bond will barely achieve a real rate of return. Consequently, this has skewed investors’ risk appetite to chase higher returns via participation in the equity markets,” he said.

He adds that while it is quite difficult to project future earnings from an array of industries, equally there are those industries and companies that are benefiting from the current circumstances. “In all these cases, the market is looking past the short-term outlook and projecting a recovery in the medium term going by current valuations.”

Why the bears are wrong

In Why you should fear the big bad bear, the experts say the prices of risk assets are being driven up because of the extraordinary liquidity the central banks are providing. They say the “bull case” will need to play out perfectly to justify prices, but that many of the central assumptions of the bull case face significant challenges over the months ahead.

However, our bullish experts disagree. Emanuel says the bear case assumes things will get worse before they get better. “But we as a species have survived far worse conditions, circumstances and pathogens than COVID-19, despite what we are told by our government and the media,” he said. “Humans are adaptable creatures and usually recover far faster than expected. We only need to look at present conditions in China, which is now back to business and life as usual despite being one of the nations most affected by Covid-19.”

Jun Bei believes the bears are just trying to be conservative. “There have always been bears in the equity market; at every point in the cycle, there will be people talking about how it should be lower,” she said. “While, equities are a risky asset, and shorter-term there is likely to be volatility, over a long period of time, equities by far generate the best return relative to other asset classes. In addition, equity market looks extremely attractive once you take into account their average dividend yield and capital growth opportunities.”

Meanwhile, Shane says bears aren’t necessarily wrong – they are just offering another possibility, which should be respected. “Shares could go back to their March lows or lower if we have a return to a full-blown lockdown or President Trump escalates tensions with China in an economically debilitating way,” he said. “But the more likely outcome is that we learn to live with the virus and if a medical solution is found, the recovery will be faster.

Either way, the pick-up in economic activity combined with ongoing low interest rates and bond yields as inflation stays down in response to spare capacity, is more likely to see sharemarkets ultimately resume their rising trend, expects AMP Capital.

Upside risks not being priced in

While the bears claim downside risks are not being accurately priced in by markets, the opposite is also true. There are reasons why markets could "melt-up".

Shane says in this environment, there are two big upside risks: a medical solution to COVID-19, and a full-blown resumption of the search for yield on the back of low interest rates.

“If a medical solution is found involving a treatment or preferably a vaccine, this could drive a sharp bounce in economic activity. This, in turn, would likely drive a sharp rebound in profits. If this occurs, shares are likely to re-rate higher as investors resume the search for yield," he said.

Meanwhile, Emanuel says an interesting aspect of the latest rally is that it has occurred despite business and social confidence being so low. “This begs the question ‘what happens when business and social sentiment begin to recover?’” he says.

He believes sentiment over the next six months will be driven by three factors:

- The recovery of political stability and certainty following the US election, which will have a significant influence on markets post-November, with significant volatility expected prior to the election.

- The development of more accurate COVID-19 tests that assist with the perception that governments are able to manage the spread of the virus, in the case of nations that are taking a harder line towards prevention.

- The progress towards a COVID-19 vaccine that will boost public confidence.

Jun Bei agrees finding a vaccine is one key upside risk that will help keep the market strong and once one is found, the equity market can move on without worrying whether the near-term earnings impact due to the global pandemic is truly a one-off event. “Forget about the near term earnings hit, because with a vaccine the market can finally move on from the uncertainties caused by the pandemic,” she said. “This will be a significant catalyst, and potentially it's not too far away.”

Where to invest $10,000 right now?

Our experts have presented their case for why the strength in the markets is continuing - so what's the best way to play it as an investor with $10,000 to spare?

In part 4 of this series, my colleague Bella Kidman will publish the top investing ideas from our seven bears and bulls. Follow her profiles by clicking on her name, then the “follow” button, to gain first access to the wire, which will come out shortly.

The Bull versus Bear series so far

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Featuring

Kate Samranvedhya,

Jamieson Coote Bonds

Kate oversees a range of investment strategies for JCB clients and is based in Singapore. She is a career fixed income portfolio manager, and specialises in High Grade Bond portfolio management across all major global regions.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

2 topics

5 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management