Afterpay: Boom or bust?

If there was such a thing as a fairy tale in an investment context, the ASX’s tech darling Afterpay (ASX:APT) would no doubt be a worthy poster child. For investors who had participated in the 2016 IPO and held on, the stock would be a ~90 bagger by now.

Livewire readers nominated Afterpay as their second most popular choice among the 10-most tipped big caps for 2020. They picked it when the buy now-pay later leader was trading at a market cap of under $8 billion. That number now is already ~$26 billion (that’s half the size of ANZ Bank by the way).

But the company’s warp-speed journey to nearly $100 has set off an explosion of divisive debates among investors. Will Anthony Eisen and Nick Molnar’s flawless execution continue into new markets, or will a tide of bad debts, rising unemployment and new regulation break the back of Australia’s hottest stock?

In this wire, I reach out to long-time holder Simon Shields of Monash Investors for the bull thesis, and Dean Fergie of Cyan Investment Management, who sold out of the stock, for the bear case.

THE BULL CASE

How long have you held the stock, and how big is your position currently?

We've held it for 3-4 years and first bought it when it was about $5. We held off buying it because we had in the first instance concerns about its bad debt experience. Clearly BNPL was a very new concept at that stage.

The other thing to overcome was the regulatory acceptance and that led us to get into and out of the stock and reduce our weighting quite significantly at times. But ultimately, we've had a pretty substantial weight in the stock, fluctuating between 4% and 8% most of the time, but at times selling it down, particularly when it's had very rapid share price appreciation.

What attracted you to the company?

There are two things that are incredible about Afterpay:

- Firstly, the attractiveness and acceptance from both merchants and consumers. It's such an easy sell and we can just see that it's penetrating markets wherever it goes.

- Secondly, what's different about Afterpay compared to a lot of stocks is the predictability of the usage over time. That is something that they highlight again and again. I mean, five years ago, this business had almost no sales, it was just starting out. In fact, there's a great chart (see below) that shows that. FY 16, zero underlying sales, FY 20 $11 billion of underlying sales. I mean, that is phenomenal.

Click to enlarge

Afterpay FY20 Results Presentation

What were the key points of the recent result?

There were some things that were very interesting.

- Firstly, they announced their first steps in Asia via a small acquisition of a Singapore-based company.

- Secondly, you've got the percentage of customers' subsequent spending compared to their first purchase and how that compares to other buy now pay later competitors (see chart below). This really goes through this predictability point about customer usage, but it's a huge contrast with competitors. That really is a key thing.

Click to enlarge

Afterpay FY20 Results Presentation

Why is that Afterpay is seeing more frequent usage than its competitors?

If you think about who the competitors are, my guess is the two competitors are Affirm, and Klarna. Those competitors tend to have higher dollar value transactions … so it’s more of special occasion spending.

Now what Afterpay also said on the call was in speaking to their retailers; their merchants, what they find is merchants who have put multiple BNPL alternatives on their platforms - they see that Afterpay is the one that the customers keep going back to.

How did the results compare with your expectations? And those of the broader market?

I thought it was broadly in line and quite frankly, I would have been shocked if it wasn't broadly in line. The market reaction has been very interesting because I think on the back of the new information about Singapore and perhaps just some of these little extra metrics, the stock price went up early and then it came back.

How do you justify the valuation on Afterpay?

Our view on the stock is when you look at the experience that Afterpay had in Australia; if you can extrapolate that to the United States, and more recently to the United Kingdom, it's very easy to come up with a valuation of the $70 to $90 range.

Afterpay has the right product at the right time and is replicating the success. However, what we didn't have in our numbers, and I don't think anybody really in the market had any of this in their numbers either, is the European expansion. Europe is a market that is a similar size to the United States. Then we have to go and make that assumption. Can we assume they're going to do as well in Europe as we expect them to do in the United States?

Caution would say no, but that entry, that business in Europe has got to be worth $10s of dollars to the share price, even if they only do half as well as in the United States. Now we see them going to Asia ... you wouldn't say that the Asian opportunity in the near term is going to be anywhere near as big as the European or United States opportunity, but it's still a significant value add to the business.

You're paying for $90 for success in these markets, but not a great deal of success. I think that at $90, the dilemma is in fact that if they executed to expectations in these new markets, the share price is worth a lot more than that.

Where there any other surprises?

There are a couple of things I noted in the report:

- Firstly, they've seen a major acceleration in usage from COVID and working from home and staying at home. You can see in the chart on the left the acceleration of e-commerce penetration from 16% to 27% due to COVID.

- Secondly, the other chart on the right is showing how the share of credit cards has been cut back. We've seen that in Australia recently with the numbers that have come out, there's been a real reduction in total balances of credit cards in Australia at the time as well.

Afterpay FY20 Results Presentation

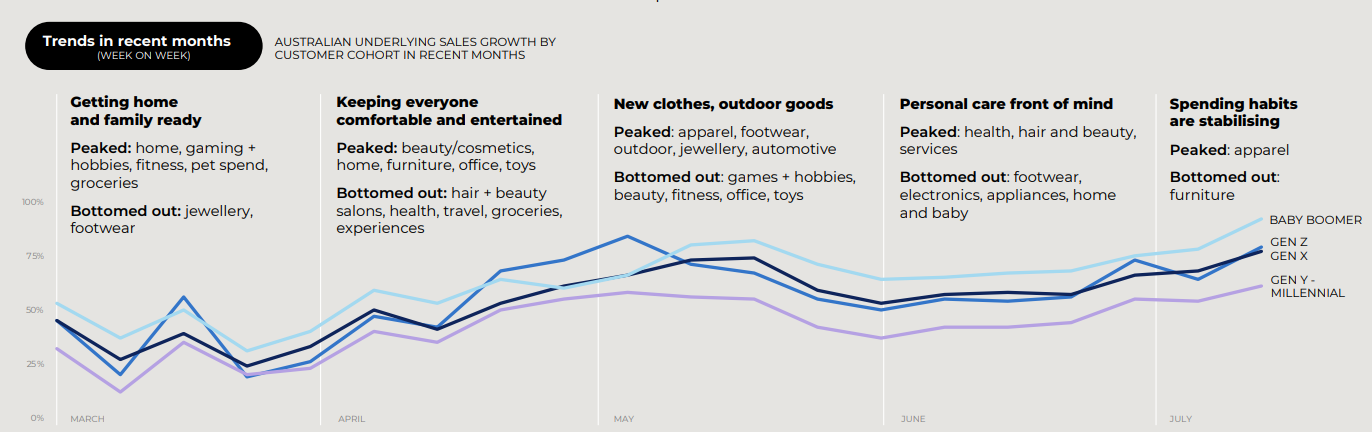

- Finally, they show how that trend has happened in Australia, by age cohort or generational cohort. The baby boomers are the oldest now of the cohorts. You can see, they are really picking up their use of this platform.

Click to enlarge

Afterpay FY20 Results Presentation

Has your position on the stock changed post results?

The largest stocks in our portfolio tend to have a weighting of between 5-7% and Afterpay is just one of the larger weights in the portfolio.

This result gives me a lot of confidence that everything's on track and we're more or less happy with our position.

THE BEAR CASE

(Ed’s note – Dean previously wrote about why he sold Afterpay when it was a 35-bagger. He builds on those thoughts, and why he would avoid the company even if his fund’s mandate allowed him to own it today).

What's your history in owning Afterpay?

We first bought into Afterpay at the IPO which was $1. When you have a business that goes from $1 to $35 over a quick period of time your weighting moves substantially. On average, it probably would have been around 3-7% of the fund.

What attracted you to the company?

I went into a shop 3-4 years ago to buy a hoodie for my son, using Afterpay, and thought that it worked seamlessly.

From a financial perspective, we love the fact that the velocity of the capital is so great; that they were literally getting money in the door and six weeks later getting it paid back and then doing it again. You have small amounts of money being paid back 12-15 times a year. They're clipping the ticket at 4% more or less every time, which just meant their capacity to generate large amounts of money was incredible.

The other benefit, which I think has taken the market a very long time to notice, is the very low credit risk they're taking on because the payback period is so fast and the dollar values are so small.

Why did you exit your position? Was it valuation or the fund’s mandate?

A little bit of both. We like to see businesses that can quadruple their business in a short period of time. We felt that it had got to quite a large size at around $10 billion.

We thought to expand that market capitalization by a factor of 100% or 200% was going to be more difficult. We thought there were risks in going into new jurisdictions. And for us, we're not a large fund. We don't need to be investing hundreds of millions of dollars. We can take that capital off a big company and put it back into a smaller one to make better returns.

I’d also flag that Afterpay has seen a lot of volatility in its share price. Today's a perfect example. You've got a nearly, a $25-$30 billion company that’s traded in more than 10% range in one day. There's just a lot of volatility in it, so it's a risky proposition from a share price perspective, to have a large weighting in.

What were the key points of the recent result?

The growth's extraordinary. The main positive is that their net margins are going up and their bad debts are going down. I mean, it's proven the business model incredibly well.

But when I look at sales, customer and merchant growth all being up by 70%-100%, last financial year those numbers were 130% and the year before they were in the order of 100-150%.

The business is still growing, but it's growing at a decreasing rate, and compounding says that this business cannot keep growing by 100%, not when you've got 10 million customers and $11 billion in underlying sales. That is going to slow down. You need to see this growing at extremely high double digit rates of 50-100% for the next five years in order to really justify the current valuation.

Would you buy, hold or sell Afterpay even if you could own it today? Why or why not?

We're a sell as we can't justify the current price, but people own this stock because it's a big part of the index now. And add to that the fact that every day trader and his dog are punting this stock, along with all the others – Zip, Sezzle, Splitit and OpenPay - there's a cohort of these businesses that are growing way bigger in terms of share price than anyone expected.

It's just this perfect storm ... I would take nothing away from the management, but I just think that for us, if you go back to fundamentals and fundamentals I reckon are maybe a little bit less relevant at the moment, it doesn't make sense.

And look the business still hasn't been completely proven yet. The business is not making money at the bottom line. Sure, their profit numbers look great, but the EBITDA is still marginal at $35 million. A $25-$30 billion dollar business, should be at the minimum at some stage, making $500 million after-tax. It's a long, long way from that at the moment. Lastly, there's a lot of merit to it but this business and its share price performance will live or die on how deeply and profitably they can penetrate the US market. That's all it's about.

If you're not a buyer of Afterpay, what are the other opportunities you're liking in the same space?

Our preferred pick in this space is QuickFee (ASX:QFE). They have a similar product, it's payment processing, but it's for professional services companies. It's a processing arm and also there's a bit of credit there and we think that that probably has lower credit risk than consumer credit.

But the thing is it's a small business. Our view is finding a $100 million business that can move to $500 million is a better investment bet than trying to find a $20 billion business that can move to $100 billion. That's the way we're looking at it.

What weighting do you have to QFE?

We've have a bit over 5-6% in the stock. I would qualify that we're a little bit wary about the whole space and just the fact that there's so much hype involved,

There's a lot of I think artificial tailwinds in respect to how this government spending is swirling through the economy and how that money's moving around. We think it's probably as good as it can get for the moment. The outlook is far less rosy for those businesses.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

4 topics

2 stocks mentioned

2 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment