Australia’s infrastructure boom is coming

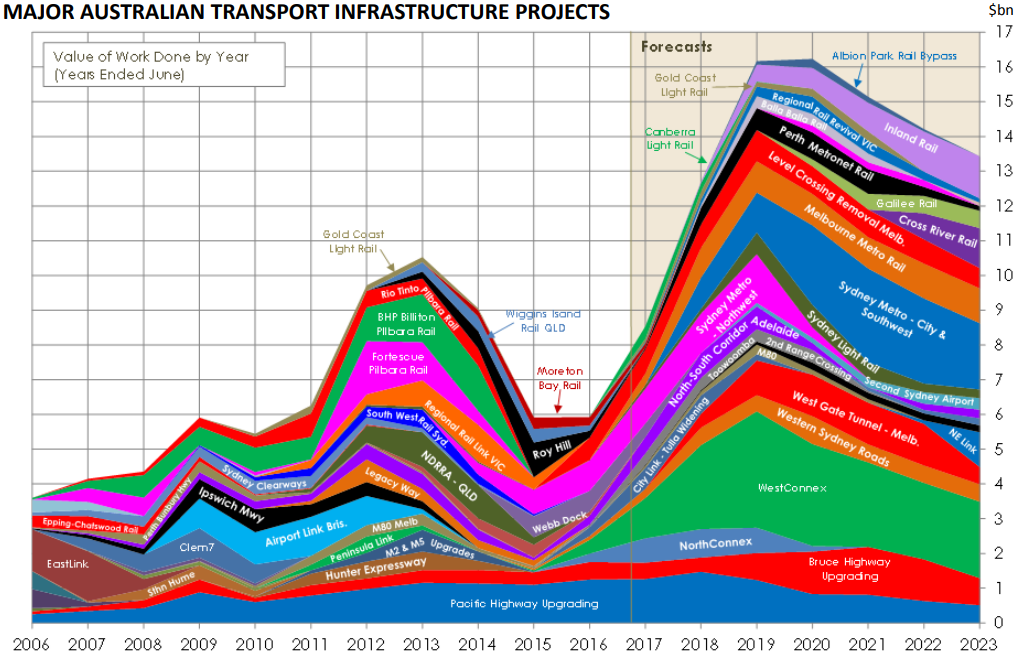

As the housing construction boom comes to an end, the obvious question for investors is ‘where next?’ One potential opportunity lies in transport infrastructure construction, which is poised to double over the next few years. Between roads and rail, annual spend is expected to increase to $16B by 2020.

Source: Macromonitor, CIMIC Group

Infrastructure is a more competitive space than it was a few years ago. In the wake of the mining boom (and bust), many mining services contractors diversified their business into other areas of construction and development. With mining development beginning to pick up again, this has created dual tailwinds for some companies. David Allingham from Eley Griffiths Group recently told Livewire:

"Companies that are exposed to investment in mining and construction are very well positioned to deliver earnings growth into FY19. Australian businesses took a 5-year capital expenditure holiday from 2012, but it is now clear intentions have changed."

As a starting point for further research, I’ve identified seven companies with some level of exposure to this thematic.

Disclaimer: This article is not an endorsement or recommendation for investment of any of the companies mentioned, either by Livewire or the author personally. Investors should undertake their own research and talk to a financial advisor before making any investment decisions. The author does not hold positions in any of the companies mentioned.

Adelaide Brighton (ABC) – Adelaide Brighton is an importer, supplier, producer and manufacture of construction materials, with market leading positions in cement, lime, and concrete. In their recent investor newsletter, CEO Martin Brydon described higher revenues on the back of “the continuing strength of the Victorian, NSW and Queensland construction and infrastructure sectors.” Adelaide Brighton is capped at $4.1B and is up 16.2% YTD.

Boral (BLD) – Boral’s Australian division accounts for ~59% of overall group revenue. Boral’s products on offer include concrete, asphalt, and cement. Boral is capped at $9B, up ~40% so far this year.

CIMIC Group (CIM) – CIMIC has a number of divisions that could potentially benefit, including construction (CPB Contractors), public private partnerships (Pacific Partnerships), and engineering (EIC Activities). According to their latest market update, CIMIC is currently bidding on $23B worth of tenders to be awarded this year, including WestConnex in NSW, and the Cross River Rail Project in Queensland. CIMIC is capped at $16.5B and is up ~46% this year.

Downer EDI (DOW) – Downer has a broad range of services, but their Transport division is the largest by both revenues and EBIT. Transport accounted for 28.6% of revenues, and 44.9% of EBIT in 2017. In their recent update, the CEO said transport is performing well, “with strong increases in both revenue and EBIT.” He believes the outlook for the sector is “very positive”. Downer EDI is capped at a touch under $4B, and the share price is up 9.2% this year.

Seven Group Holdings (SVW) – Seven is an interesting conglomerate that includes heavy equipment (WesTrac), equipment hire (Coates Hire), generators and pumps (AllightSykes), and traditional media (Seven West Media). All of these, apart from Seven West Media, would appear to be exposed to increased infrastructure spending. Seven Group is capped at $4.5B and has rallied over 82% so far this year.

Veris (VRS) – Veris is a microcap surveying company, formerly known as OTOC. It’s capped at a touch under $60M, making it the smallest company on this list. The company has had a tough year, following poor results in February and the resignation of its CEO and MD in March. However, things appear to be improving, with a recent market update from the company, stating that “Infrastructure investment in New South Wales continues to be the main driver behind increased revenue, in particular, investment in transport infrastructure. Veris is down ~27% this year.

Worley Parsons (WOR) – Infrastructure forms a relatively small part of Worley Parsons’ business. The sector accounted for 19% of revenues, and 5.6% of EBIT in FY17. The remainder of the business is made up by hydrocarbons (oil and gas), and minerals, metals and chemicals. Worley Parsons is capped at $4B, and has rallied just under 60% YTD.

A number of Livewire contributors have previously written on this topic. I’ve shared a quote and a link back to each of them below.

East coast exposure at Perth prices

Perennial Value

“We are confident of an improved 2H17 result and positive outlook for the company. We consider director buying announced on the 4th and 11th of May as being supportive of our view. Further, we note the limited amount of organic growth in consensus forecasts, which appears conservative versus the infrastructure expenditure pipeline above and anecdotes of increasing rates in the industry.”

Getting onto the next big trend

Harness Asset Management

“We have pivoted the HAM portfolio to gain exposure to the strong trend in infrastructure spending… We have established ownership positions in companies across areas covering: high strength steel, large tank construction and maintenance, wharf and bridge building, cladding, energy consulting and solar construction… We suspect that it is early in this cycle and we will do well over the next few years as “tendering work”, “work in progress”, “pipeline” all convert into strong profit growth and margin expansion.

Boral: Growth at a reasonable price

Leyland Asset Management

“The expected continuing growth in the US economy (in particular, housing and infrastructure) and the Australian infrastructure segment (Boral’s exposure being 20%), leaves the company in a very strong position to continue its impressive trajectory over the coming years.”

Exposure to infrastructure, mining pick-up

OC Funds

“We view Seven as an excellent exposure to an expected pick-up in both the Australian infrastructure investment cycle and the mining cycle, both of which appear to be in the early stages of a recovery which could run several years.”

The beneficiaries of the East Coast infrastructure boom

Tamim Asset Management

“There will be some significant winners from this increase in infrastructure work, the question investors have to ask is who they will be and is it already in the price. Obvious beneficiaries such as Cimic have seen their prices run hard but there is one value opportunity that we have initiated a position in recently, which is Veris.”

If you've got thoughts on this thematic or any of the companies mentioned, we'd love to hear from you in the comments below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for Mining.com.au.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium.

3 topics

7 stocks mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for Mining.com.au. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for Mining.com.au. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment