Back to the future – interpreting yield curve indicators to forecast the risk of a US recession

Much has been made over whether the flattening of the yield curve is signalling an increased risk of recession in the US. Yet the key is not whether the yield curve is flattening but, as events in the 1990’s demonstrated, whether a central bank is ahead or behind the inflation curve.

Flatter yield curves are consistent with anti-inflation credibility

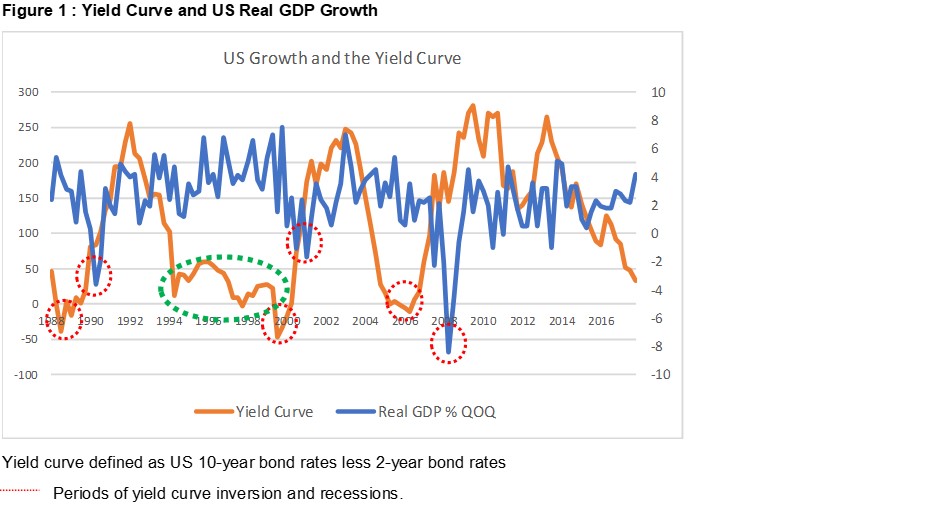

To demonstrate the link between yield curves and recessions in the US, Figure 1 plots the yield curve and quarterly percentage growth in real GDP. As demonstrated by the red circles, it is evident that an inversion of the yield curve has preceded each of the last three recessions in the US since 1988. Yet what is often overlooked, and is potentially highly relevant, is the period circled in green. This is the period from 1995-1999 when the yield curve remained historically flat, sub 50 bps, for an extended time. The question therefore is whether the recent flattening of the yield curve is a harbinger of recession or simply a move back to a relatively flat yield curve? To better appreciate any parallels it is worthwhile going back and recapping what actually occurred in the 1990’s.

Though over time Alan Greenspan came to be held in near reverence by the financial community, it is easy to forget that in the early 1990’s there were considerable doubts as to whether, as Volker’s successor, he would hold the line on low inflation. The key actions by Greenspan, which finally cemented the US Federal Reserve’s (‘Fed’s’) anti-inflation credibility, was the pre-emptive tightening of monetary policy in 1994-1995 which dealt with the last material ‘inflation scare’ in bond markets. Following this successful pre-emptive move against inflation the economic commentary started to shift to the ‘death of inflation’ and inflation expectations became more solidly anchored. What the relatively flat yield curve seen in the second half of the 1990’s demonstrates is that, once a central bank has established its anti-inflation credentials, yield curves can remain quite flat for extended periods. It is in this context that investors need to consider the more recent flattening of the yield curve. As cash rates have increased from the emergency levels associated with the quantitative easing post the Global Financial Crisis in 2008 the curve has moved back to levels consistent with a ‘credible’ Fed.

Is the Fed ahead of or behind the inflation curve?

As a relatively flat yield curve is consistent with a ‘credible’ central bank, the key to interpreting a flattening of a yield curve is not the movement itself but whether it signals that the Fed is ahead or behind the inflation curve; i.e. assessing the inflation pressure in an economy.

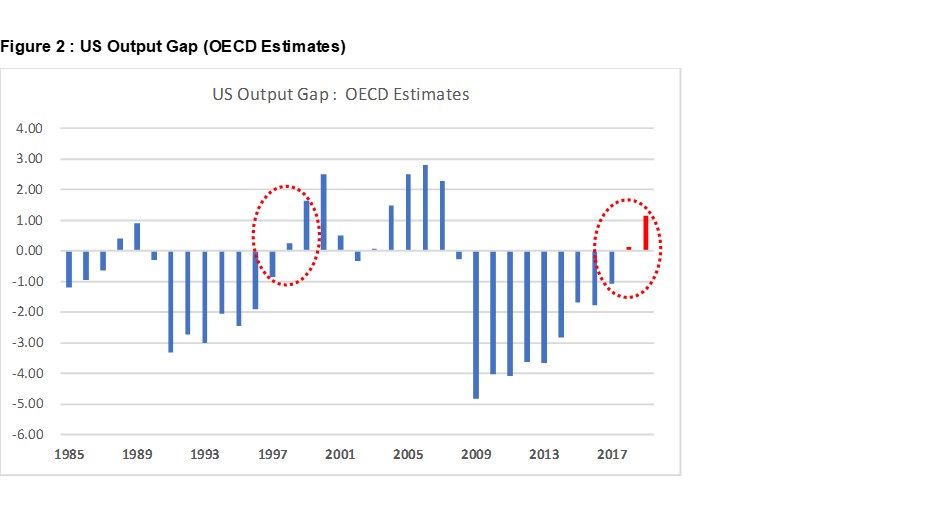

Quantifying the inflation pressure within an economy is difficult but one of the more common measures used is the ‘output gap’, i.e. how far cumulative economic growth is from potential. The OECD calculations for the output gap, with projections for 2018 and 2019 in red, are plotted in Figure 2. When considering ‘output gaps’ the parallels between the 1990s and the last decade are quite striking. Most notably both periods exhibited nearly a decade of material negative ‘output gaps’; i.e. disinflationary pressures. But the most pressing question is whether the US economy is currently at a similar point to 1995 or more towards 1998? The projected output gaps for 2018 and 2019 do suggest that the US economy is currently, in terms of inflationary pressures, closer to 1998 than 1995.

Does this mean that, as in the late 1990’s, the Fed is once again behind the inflation curve? When addressing this question it is worth noting an important difference in terms of the behaviour of the Fed. In the 1990’s cycle, as the US economy was approaching capacity, the US Fed actually cut interest rates by 75bps in 1998 in response to the Russian default and collapse of Long Term Capital Management. The result of this easing of monetary policy was to trigger a boom in the stock market and provide extra fuel to a US economy which was already rapidly overshooting its potential. Effectively by cutting interest rates materially in 1998 the Fed put itself behind the domestic inflation curve. The result was a material tightening from May 1999 and a relatively mild recession in 2000 as the Fed moved to head off inflationary pressures. By contrast in this cycle the Fed is raising rates as the US economy moves into a positive output gap and is not actually taking steps to fuel the boom; i.e. is in the process of reducing liquidity within the system as the US economy approaches capacity.

Assessing whether in this cycle the Fed is ahead or behind the inflation cycle is made more difficult as having anti-inflation credibility can be a ‘two-edged sword’ for a central bank. When a central bank is successful in anchoring inflation and inflation expectations, it can often result in traditional indicators of excessive monetary stimulus communicating less information. This occurred in the 1990’s and allowed the Fed to run above its previously presumed non-inflationary potential. There is the risk that the same phenomena may be occurring in this cycle. With that said, if the Fed can remain ahead of the inflation curve by systematically raising rates, it is likely that the yield curve can remain relatively flat for an extended period of time without signalling an increased risk of recession.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

3 topics

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment