Banks Report Card 2016

Over the last two weeks’ investors have had a wild ride with the markets fretting over the outcome of the US election. In the middle of this, the Australian banks reported their profit results, which gained very little attention. We have no intention of adding to the pile of “expert opinions”, nor commentating on what a Trump presidency means for Australian equities, as we see it as having a pretty minimal impact. Market pundits fretting over the impact of the US starting a trade war with China; ignore the fact that China holds 10% of the $10 trillion publicly traded US debt. Given the new government’s fiscal stimulus plans and the associated deficits and thus increased borrowing it makes little sense for the US to antagonize its largest creditor.

In this piece, we look at the common themes emerging from the banks’ results, differentiate between them and hand out our reporting season awards to the financial intermediaries that grease the wheels of Australian capitalism.

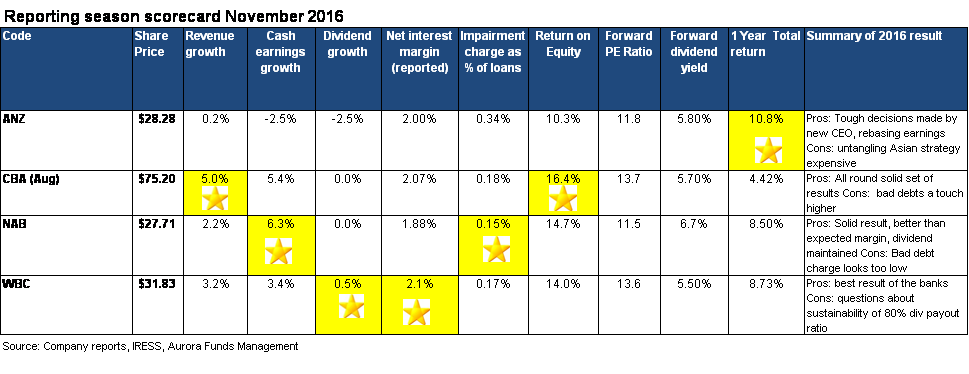

Across the sector, profit growth was mixed with NAB leading the pack and ANZ bringing up the rear as the new CEO moves to rebalance the bank and exit from Asia. While the cash earnings growth in the above table doesn’t look too bad, all four banks earnings per share were weaker thanks to the 2015 capital raisings which generally added 4.3% to the number of shares outstanding for most banks. Gold star - NAB

Bad debt charges low but rising: One of the key themes across the four major banks and indeed the biggest driver of earnings growth over the last few years has been the significant decline in bad debts. Falling bad debts boost bank profitability, as loans are priced assuming that a certain percentage of borrowers will be unable to repay and that the outstanding loan amount is greater than the collateral eventually recovered. In May 2016, we saw signs of increasing bad debts and it was expected that bad debts would continue to trend up in the second half of 2016. The biggest surprise for me was how benign bad debts were in the second half, compared with the first half where the banks reported impairments to large single name loan exposures such as Arrium, Slater + Gordon, Peabody Coal, Dick Smith and McAleese. For example, Westpac reported $471 million in new individual provisions in the first half, but this declined to $256 million in the second half. Gold star - NAB

Dividend growth stalled: Across the sector dividend growth has essentially stopped, or in the case of ANZ rebased downwards by new CEO Elliot. This is a function of both the capital raisings last year that increased the number of shares outstanding and minimal profit growth. Westpac was the only bank that grew its dividend in 2016 and indeed faced criticism from many analysts for its high payout ratio. Paradoxically the ANZ were rewarded for rebasing their dividends downwards, as it was interpreted as a hard-headed decision made by the new CEO. While dividend growth across the banks is likely to be meager in the near term, the major Australian banks in aggregate are sitting on a grossed-up yield of 8.5% a record premium to the current 180-day term deposit rate of 2.3%! Gold star - Westpac

Loan growth: In 2016 the banks on average achieved a meagre 4% growth in their loan book, while loan growth is improving particularly in housing; overall deleveraging continues to have an impact on the net demand for new loans especially to corporates. CBA and Westpac have been the most aggressive in growing their loan book, but loan growth has been capped by APRA guidelines designed to keep investment housing loan growth to less than 10% per annum and requiring banks to hold more capital against their loan book. Gold star - Commbank

Net interest margins in aggregate contracted slightly, though there was a dispersion of results with Westpac seeing expanding margins and NAB reporting a contraction. In 2016 CBA and Westpac had the highest and most stable net interest margins, whereas NAB and ANZ both delivered lower margins. This reflects the two Melbourne-based banks having greater relative exposures to business banking and CBA/Westpac greater weighting to housing.

One of the key things we looked at closely during this results season was signs of expanding net interest margin (Interest Received - Interest Paid) divided by Average Invested Assets). As expected, we saw the banks passing on some of the costs of increased capital that have been borne by shareholders onto customers. As the cash rate was cut twice in 2016, we see that maintaining a stable net interest margin of around 2% is a good result for bank shareholders. Gold star – Australia’s banking oligopoly.

Total returns: Over the last 12 months ANZ has outperformed the ASX 200’s return, whereas CBA has underperformed on a total return basis (capital gain plus dividends). While the Australian banks quietly delivered cash profits of A$29.6 billion, their share prices have been quite volatile over the past year due to concerns around European banks, additional capital requirements and yield stocks falling out of favour. As ANZ has been rewarded for rebasing earnings and cutting the dividend, it will be interesting to see if the other banks follow suit. Gold star - ANZ

Valuations: Currently the banking sector is trading a forward Price to Earnings ratio of 12.9x, which is roughly in line with its long-term average but at a 32% discount relative to the ASX Industrials. Looking across the sector NAB is the cheapest, trading on a PE of 11.5x and 6.7% yield. This represents a PE of 89% relative to the average of the major banks. Typically NAB has traded at a discount to the sector due to the issues with its United Kingdom based banks, however, with the spin of Clydesdale and Yorkshire earlier this year, NAB now has fewer issues and has a cleaner investment case. Looking at yields, the banks as a sector currently trades at a 5.8% premium to the one-year term deposit rate.

Contributed by Aurora Funds Management: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

3 topics

4 stocks mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment