Can’t Trump this sector

Michael Doble

APN Property Group

It’s getting predictable isn’t it? The Donald tweets, the rest of the world reacts and equity markets shudder. Blame the 24-hour news cycle, event driven macro traders, fake news or almost anyone with an opinion (in my opinion).

Why tariffs?

Some believe that if the US manufactured more of the goods that their consumers demanded (directly or indirectly) then everyone will benefit – particularly the “middle Americans” who voted for Donald Trump at the last election.

In June, Trump announced a blanket 25% tariff on ‘industrially significant technologies’ imported from China. This includes components used in industrial machinery, electric motors, television & camera components, among many others.

UBS Economist Seth Carpenter said of these actions: “The first list of $50 billion in imports was carefully chosen to avoid economic harm. … but to reach $200 billion, the list must include some imports for which the US does not have ready substitutes. ….expect the economic harm to be larger, (with) disruptions of supply chains to manufacturing.”

By increasing the price of an imported product by adding a tariff, the theory is that consumers will simply substitute with an alternative, locally produced product.

Trump’s political strategy has been to revitalise the country’s manufacturing base by raising the cost of imported raw materials, which are easily substituted by domestic materials. He wants the US to remain a world leader in technology and stifling China’s home-grown industries by crimping exports is one way to do this.

It all sounds logical. But unfortunately, things are never that simple.

The tariff strategy ignores the reality of comparative advantage

As UBS alluded to, the logic also fails when there is no locally made substitute available.

Unlike steel and aluminium, technology goods aren’t easily substitutable. Raising tariffs on high spec machinery that the US cannot produce itself could have serious adverse impacts on US business.

Winners and losers

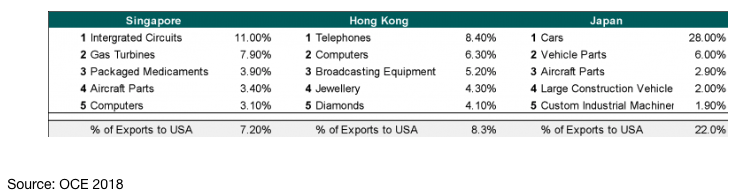

Japan, Singapore and Hong Kong all run current account surpluses, meaning their economic growth is export-led. Potentially, this could make them vulnerable in a Trump-led trade war.

Either Trump targets each country directly by imposing trade tariffs, or he keeps his focus on China, with the reverberations felt across the Asian region, causing an indirect impact. It all started with a warning shot; Trump kicked off trade negotiations by announcing tariffs on steel and aluminium.

This caused a collective shudder across the entire Asian region, those type of products are the staple of developed Asia’s exports. To illustrate, here are the top five exports to the US from the three countries which are the focus of the Asian REIT Fund:

However, this needs to be viewed in the context of Trump’s geopolitical strategy. These tariffs are specific to China as Trump views China as a threat to its economic power.

So where to source it? Perhaps from countries that Trump isn’t politically at war with. Rather than be crimped by a trade war, perhaps we might see the rest of Asia increase their exports to the US to pick up the slack.

The one outlier is Japan, with its emphasis on vehicle exports. With a well-established auto industry, it’s possible that Trump could impose tariffs to give the country’s ailing industry a leg up, a threat he has recently made.

Whilst tariffs may appeal to populist politicians and to domestic workers who receive the benefit of increased demand, a tariff is unlikely to be the friend of middle America in the long term.

Short term winners are the politicians “selling the dream” and the workers in the subsidised sectors who get the “sugar hit” of added demand. Longer term winners are the bureaucrats who administer the fiasco.

Short and long-term losers are consumers (aka: all of us)

Tariffs and its impact on Real Estate

Running a Fund focused on real estate investment trusts (REIT), we often get asked our view on how a trade war will affect Asian commercial real estate. The short answer is “not much”.

Real estate is a local game. The primary determinant of rents, whether it be a new shopping centre, office building or industrial warehouse, is supply.

This is what makes commercial real estate cyclical. Whilst demand is dynamic, supply, at least in the short term, is static. A new office building can take upwards of three years to complete. In the meantime, if other buildings are being released to market, landlords typically respond to an increase in supply by reducing rents.

As for demand, it is very much linked to GDP growth. Falling exports can inhibit economic growth, and with it rental growth. Given this theoretical background it’s tempting to draw an adverse conclusion about the impact of a US/China trade war on commercial property in the Asian region.

Of course, we’ll continue to see bumps in the stock market as the Trump Trade narrative gets rehashed for the umpteenth time.

What we can confidently say is that the commercial property market isn’t buying into the short-termism.

Right now, commercial rents are on an upswing in Singapore, the Hong Kong office market continues to break transaction records and Tokyo recorded a low commercial vacancy rate of 2.57% in June.

We’ve long argued that investing in Asian commercial property offers exposure to Asian growth without much market volatility. Recent events support that thesis.

Further Insight

For further insights from our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

1 topic

Michael Doble

Chief Investment Officer, Real Estate Securities

APN Property Group

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

Michael Doble

Chief Investment Officer, Real Estate Securities

APN Property Group

Michael is highly regarded in the real estate funds industry, with 31 years experience. He's held various senior roles specialising in real estate valuation, consultancy and funds management

Comments

Comments

Sign In or Join Free to comment