What are our strongest investment positions?

In our first monthly letter for the year, we highlighted that 2018 was unlikely to be a ‘set and forget’ year for investment strategy. As we approach the second half of 2018, macro uncertainty and cascading geo-political risks continue to impact markets and seem likely to befriend us for the rest of the year.

On the macro front, early-year inflation stresses have receded, yet bond yields (and oil prices) have lurched to new cycle highs, before settling lower. Global activity has lost momentum, yet recent data signal that a reacceleration in the back-half of 2018 remains most likely. We hold fast to our thesis of robust and synchronised growth. But there are early signs that global growth leadership may be shifting to the US, underpinning US dollar strength and creating angst for emerging markets (EM) and tactical positioning.

On the geo-political front, risk continues to ebb and flow. Its amplitude has increased, and so too the frequency with which risks come and go. From the US-China trade dispute to off-and-on-again talks between the US and North Korea. In Europe, UK Brexit uncertainty has returned and political unrest in Italy has spiked. Markets now seem more sensitive to these happenings, though we still doubt they will materially shift the end-game. The world’s evolution from hegemony to a multi-polar political landscape argues that volatile geo-politics will continue to have an impact on markets ahead.

This month we take a look at how markets have fared over the first half of the year and the extent our tactical calls have benefited returns. We also chart our course for the remainder of 2018, highlighting our key positions and why we choose to hold them. Our tactical positioning this month is unchanged.

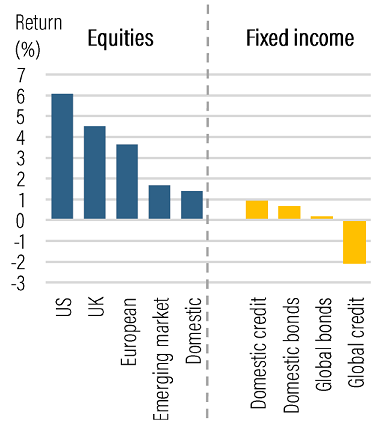

First half returns have favoured equities over fixed income

Through the volatility of the first half of the year, our core view held broadly true that the global growth cycle would persist, and inflation would rise but remain contained. To this end, leaning into equities and away from fixed income has been the correct approach. Since the start of the year, we have moved overweight global equities (but not emerging markets) and moved underweight government bonds and particularly high yield credit.

Source: Bloomberg, year to date returns (international equity returns unhedged)

Despite an outright decline in Q1 2018, equities have risen year to date. As the chart shows, there have been modest gains for EM where we held a neutral position, as well as Australia where we were slightly underweight. There were strong gains for the US and UK, where we were neutral and underweight respectively, and solid gains in Europe, which was our strongest overweight. Our non-consensus view that the Australian dollar would move lower to the mid-70s (from over USD 0.80) has also complemented our overweight global (unhedged) equities call.

Although fixed income returns have been soft, they have favoured our domestic over global tilt. Government bonds, where we were underweight, have returned close to zero, and international credit, where we were also underweight, has delivered negative returns.

Charting our course for the rest of the year

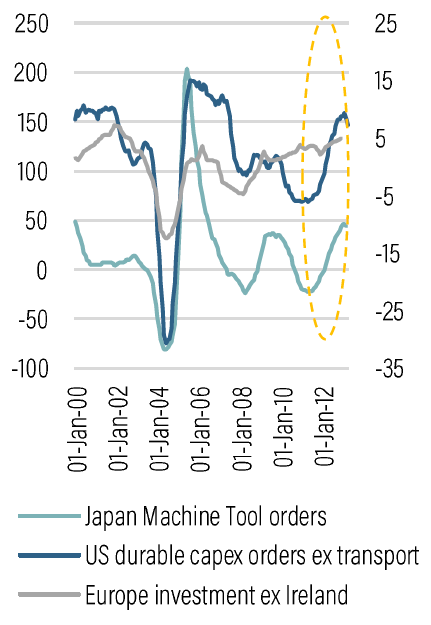

A global business investment upswing is now underway

Notwithstanding persistent volatility, our thesis of ongoing synchronised global growth reflects a belief that a global business investment upswing (beyond just energy investment in the US) is now underway. This should both extend the macro cycle into 2019 and limit the risk of a near-term break-out in inflation (that could drive more aggressive monetary tightening).

US, European and Japanese data point to stronger investment ahead

Source: Bloomberg

Our five signals for ‘staying engaged with risk’ from earlier this year remain universally intact.

- Inflation in key economies has not accelerated through 2%;

- wages growth globally remains contained;

- the global PMI has stayed above 52;

- corporate earnings have continued to rise; and

- China’s credit growth has stayed double-digit.

Still, the growth cycle is peaking as spare capacity across the world is tilting inflation higher, likely contributing to more moderate returns across growth and balanced portfolios.

What are our strongest investment positions?

1. We prefer equities over bonds

Growth momentum in the world economy has eased in H1 2018. However, it remains above trend, a positive backdrop for corporate earnings. According to the International Monetary Fund, fiscal stimulus will add 0.8% and 0.9% to US growth this year and next. Leading indicators continue to flag strong growth in Japan, while China is slowing glacially. Europe’s earlier stage in its recovery cycle, and ‘easy’ policy, should ensure solid growth ahead.

Equity valuations are still on the high side of ‘fair’ post the Q1 2018 correction, but less expensive than late 2017-early 2018. UBS analysis shows that in the past five cycles, MSCI world equities have returned over 5% on average in 12 months post a peak in global Purchasing Managers Indices (PMI). This is well shy of the gains last year where many markets rose by more than 20%.

For fixed income, in contrast, above-trend growth and gradually rising inflation is likely to continue to put upward pressure on global bond yields and raise financing costs, thereby constraining returns across bonds and credit. Of course, geo-political and trade war risks (stalling global growth) argue against too aggressively underweighting fixed income as yields rise.

Finally, recent data has added to the somewhat ‘goldilocks’ mix of firm growth and moderately rising inflation. While US inflation has trended higher after its early year pick-up, it has reversed in the UK, Europe and Japan, and remains broadly benign across the emerging markets. Further, the latest US Federal Reserve (Fed) minutes suggest a modest inflation overshoot would be tolerated, challenging early-year expectations the Fed may surprise with its intensity of rate hikes. A stronger US dollar could also limit Fed tightening.

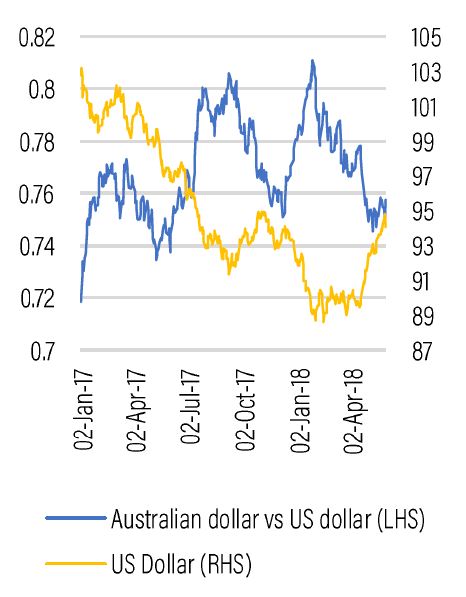

2. We don’t see a sharply weaker US dollar near term

The US’s deteriorating twin deficits—external trade and fiscal budget—should, overtime, constrain the US dollar to a weakening trend. Yet 2018 has not seen a repeat of the dollar’s 2017 weakness, when the market largely ignored widening interest rate differentials in the US’s favour.

The US dollar (DXY) continues to rebound

Source: Bloomberg

We continue to see a range of factors supporting the US dollar (against consensus for a weaker trend). Ongoing Fed hikes—at a time expectations for tighter policy in Europe, the UK and Japan are being reduced—is now supporting the US dollar. The US’s Q2 growth rebound is stronger than elsewhere, and recent policy changes are enticing capital inflow to the US.

A weaker commodity price outlook (with UBS forecasting a 7% fall over the coming year)—likely in part due to China’s focus on ‘cleaner growth’—also aligns with a stronger US dollar environment. With most forecasters staying bullish on the outlook for the euro, it remains plausible that EM exchange rates could weaken significantly, bearing the brunt of any US dollar strength.

3. We prefer developed over emerging equities

EM equities have typically performed well late cycle. However, several key factors that contributed to returns of more than 30% in 2017, as well as strong EM fixed income returns, are now reversing. The US dollar is strengthening and a peak in global production growth has formed. Elevated oil prices are constraining EM central banks from further easing and may now see faster-than-expected central bank hikes.

Brazil’s economic recovery has proved less buoyant than anticipated, with UBS recently trimming 2018 growth from 3.3% to 2.7%. Activity in Russia has disappointed, while rising oil prices have sharply heightened macro instability for Argentina and Turkey. On a rolling 12-month basis, net foreign selling is now 0.3% of market cap in emerging Asia ex-China and Malaysia (a higher oil price beneficiary). This reflects rising investor caution and liquidity risks.

4. We prefer global over domestic equities

The outlook for growth in Australia remains robust. Most forecasters see an acceleration from 2.3% in 2017 to around 3.0% in 2018. But this pick-up to ‘about trend’ compares poorly to above-trend growth in Europe and the US. This is also reflected in 2019 corporate earnings, where UBS puts consensus growth for global markets at around 10%, twice the 5% seen for Australia.

Australia also faces significant growth headwinds. Our major trading partner, China, is now on a slower path, consumers are debt-heavy (at the same time as risks of a sharp credit slowdown have risen in the wake of the banking Royal Commission) and the housing sector is ‘ex-growth’.

We also view global equities as presenting more opportunities to access some of our more favoured sector themes, such as technology, energy and financials, stronger EM population growth (as a driver of consumer spending) and markets less dominated by bond-sensitive equities.

Source: Bloomberg, MSCI, Ellerston

5. We prefer Aussie over global fixed income

With underlying inflation at or below the inflation target for two years, there is little near-term pressure for the Reserve Bank of Australia (RBA) to follow its global peers by starting to normalise rates. Indeed, both UBS and CBA have recently delayed RBA hikes, moving to Q1 2019 and Q4 2019 respectively.

Australian 10-year yields are now trading at an historic 20 basis points (bps) through US 10-year Treasuries. With the RBA likely to be out-hiked by the Fed over the rest of 2018, we look for further outperformance. This reinforces our view the Australian dollar is unlikely to return toward USD 0.80 (particularly if commodity prices move lower ahead) and may instead drift down.

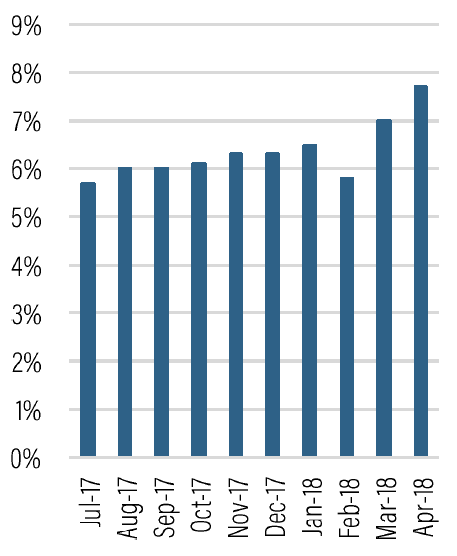

6. We recommend adding alternative investments

This year, we’ve been advocating clients consider the potential diversification benefits of alternative investments (such as hedge funds, private equity and global macro funds). These typically exhibit low correlation to traditional asset classes and can provide portfolio diversification in a maturing growth cycle where market returns are often lower, more volatile and more dispersed. Our clients continue to build positions here through April.

Alternative assets Crestone funds under advice

Summary

The current economic cycle has been long. The outlook is characterised by more uncertainty and volatility than evident in recent years. Our minds are also increasingly exercised by ‘alternative states of the world’, where US growth leadership, persistent high oil prices, and rising EM growth risks dominate investment markets.

Higher macro and geo-political volatility is also likely to be accompanied by more moderate returns, and a focus on capital preservation. Recently, BCA Research highlighted long-term valuation work consistent with total nominal returns of only 4% for equities over the next decade (reflecting current multiples), rising bond yields and an extension of the recent dollar rally.

But while the cycle is likely closer to its end than its beginning, the prospect of ongoing robust growth carrying into 2019, together with only moderately rising interest rates, encourages us to continue leaning into equites and leaning away from fixed income for the time being.

Further insights

Crestone Wealth Management provides wealth advice and portfolio management services to high-net-worth clients and family offices, not-for-profit organisations and financial institutions. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

5 topics

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment