Glenn Stevens' thought piece: The key takeouts

Livewire News

Livewire

In this thought piece for Ellerston Capital's new global macro fund, Glenn Stevens, the former RBA governor, has some fresh views on drivers of persistent low inflation in this fascinating read that also set this issue within a very long-term historical context. We distilled the highlights for you, and link to the original.

On Growth

“Over 2017, moreover, there has been an increasing sense of a more synchronised and robust global upswing. This is most easily observed in high frequency business survey data, which have generally remained positive in the US and have moved up noticeably in Europe. China’s economy has, if anything, gained a little speed this year – defying the pessimists yet again. Even in Japan, recent Tankan readings are the highest since the ‘bubble economy’ period in the early 1990s. The IMF upgraded its global forecasts at the Spring meetings in April – the first such upgrade for a few years and seems likely to do so again at the Annual meetings this month.”

On Central Banks And Rates

“The fact that the expansion has been moderate in pace thus far also means that inflation has, to date, remained quite low, unusually so for an upswing that, in calendar time, is now getting on. The US upswing, for example, is now 100 months old or more, one of the longest since business cycle records have been kept.”

“The expansion of central bank balance sheets undoubtedly bid down yields and alleviated financing constraints that governments and private borrowers would surely otherwise have faced.”

“Still, the question is: was this all the result of central banks?” Real yields have also been very low – below zero since late 2008 for the US policy rate, and at the long end the lowest since the short-lived inflation outbreaks in the mid and late 1970s. Can the actions of central banks have held down real interest rates for so long?”

“Maybe the very low rates have not been entirely due to central banks... Maybe potential real growth rates of economies have declined... Maybe animal spirits are chronically subdued."

These are variations on the ‘secular stagnation’ idea. Maybe risk preferences of the increasingly aged population in western countries, coupled with the peculiar demographics and particular social setting of the increasingly prominent Chinese population, have led to savings being allocated increasingly to bond-type assets. Maybe rates are low just because they are, and will be until they are not.”

“A reasonable guess would be a combination of the two explanations:

- structural forces, ranging from the persistent to the more or less permanent, have lowered real long-term interest rates; and

- central banks, in their efforts to provide stimulus, have lowered them some more.”

On Reasons For Low Inflation

“Plenty of observers have been pointing out that there are structural reasons for prices to be subdued.

- Globalisation of the labour market makes it harder for workers in any one country to push up their wages. There is evidence that global capacity pressures have become more important relative to local ones in a range of developed economies.

- Technological change in the form of disruption to supply chains – the ‘Amazon effect’ - takes out layers of costs. And technology also informs consumers much more fully about prices, effectively increasing competitive pressure, at least for ‘commoditised’ goods and services."

These are all important points, but it surely must also be true that a moderate upswing after a deep downturn has meant that good old fashioned cyclical spare capacity has been at work too, for an unusually long period. While it is fashionable to talk about flat or even broken Phillips Curve relationships, that fact is that those relationships were never that tight. Moreover, unemployment rates have only recently reached the neighbourhood of earlier estimates of NAIRUs in the US, and it can take some time for pressure to build.

Back in a world where there is little inflation?

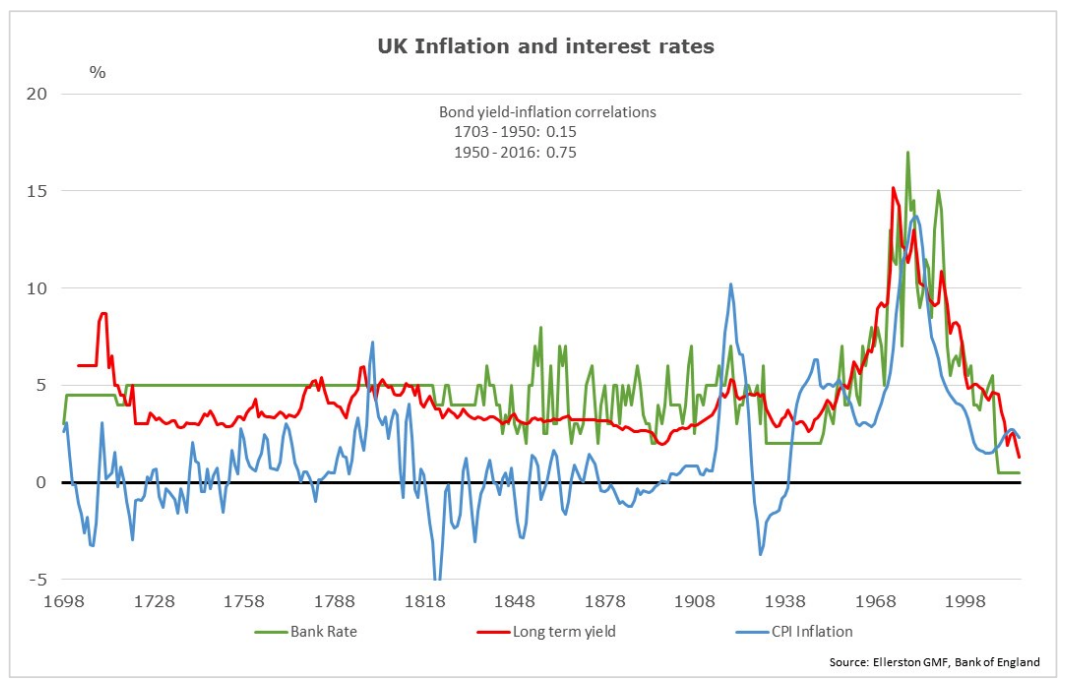

“The charts show some interesting things. Note that for about two hundred years or more, periods of high inflation were usually followed by deflation. The inflation line fluctuates around zero. The price level (in the second chart) had very little upward drift.

“…most of the inflation in human history (in anglophone countries at least) has occurred in the period since World War 2. And it was only once that had been under way for a while that people cottoned on and began systematically to have what these days we call ‘inflation expectations’.”

“For the first 250 years of the chart, there wasn’t actually much relationship between bond yields and inflation. Presumably there didn’t need to be. After all, if the long run expected rate of inflation was roughly zero, bond holders didn’t need to worry about the value of their wealth being systematically eroded by inflation – they presumably worried about other forms of loss.

"Now one interpretation of these facts would be that the period from 1950 or so until say 2010 was historically unusual – an outlier - and that we are now back in a world in which there is little inflation to speak of. "

To accept that view with confidence, though, we would want a good explanation of why that 60-year period was so inflationary, and why it has passed.

“For now, it is sufficient to observe that there is reasonable chance that a pick up in inflation could see markets flip from their current scepticism about inflation targets being approached from below, to worries about them being exceeded. This, if it were to occur, would put central banks in a rather difficult position – wondering whether to tighten faster to ‘catch up’ and retain anti-inflation credibility that was so costly to acquire 25 years ago, or to give more emphasis to a market led tightening in financial conditions slowing growth.”

Read more

You can read the original in full here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire News brings you a wide range of financial insights with a focus on Global Macro, Fixed Income, Currencies and Commodities.

3 topics

Livewire News

Livewire

Livewire News brings you a wide range of financial insights with a focus on Global Macro, Fixed Income, Currencies and Commodities.

Expertise

No areas of expertise

Livewire News

Livewire

Livewire News brings you a wide range of financial insights with a focus on Global Macro, Fixed Income, Currencies and Commodities.

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management