Housing correction is political poison

Today I review research that shows if Labor eliminates negative gearing and increases capital gains tax by 50%, national house prices could fall 9-12% on top of the current declines; parse new analysis from CoreLogic highlighting a spike in the share of apartment owners realising losses when they sell their property, which is at its highest level since the 1990s; uncover data on the big increase in the proportion of off-the-plan properties that are being settled for valuations less than the price they were purchased at; and finally dive back into the debate we've started on the bogus claims about a negative fixed-rate bonds/equities correlation, which our research shows turns positive if you are living in an inflationary world (click on that link to read or AFR subs can try here). Short excerpt below:

Affluent Wentworth voters hoping to express discontent with the dissidents who removed their prime minister might inflict massive financial losses on themselves in what is one of Australia's most investment-orientated electorates.

According to the last census, the proportion of investment properties in Wentworth is 42 per cent higher than the national average (specifically, 44 per cent versus 31 per cent of all homes)…

Yet RiskWise Property Research predicts that if Labor comes to power, the situation will get much worse with house prices slumping a further 9 per cent in Sydney and Melbourne as a result of its policies to eliminate negative gearing and hike capital gains tax (CGT) by 50 per cent for anyone who holds assets for 12 months or more. "Extensive RiskWise modelling shows that, nationally, dwelling prices would fall 9 to 12 per cent should the proposed changes to tax legislation be voted through," the authors conclude…

The timing of Labor's policies could not be worse with the royal commission having wiped $42 billion off the value of the major banks – hammering super funds' equity portfolios – while limiting borrowers' access to credit.

Even though Australian lenders have consistently maintained among the lowest mortgage default rates in the world, they are rationing credit to home owners because they are worried about breaching Labor's byzantine responsible lending laws, which have entangled the royal commission's activists…

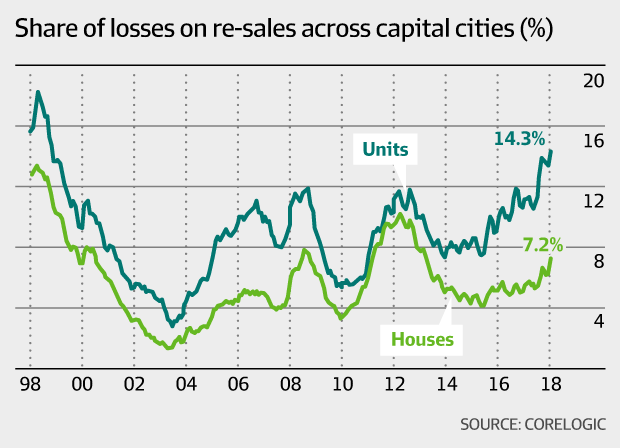

Research from CoreLogic shows the share of apartment owners – most of whom are investors – that lose money when they sell their asset has climbed to its highest level nationally since the 1990s before accounting for stamp duty, real estate commissions, mortgage repayments and maintenance costs.

More than 14 per cent of all apartment owners' resales are suffering losses, notably above the 11 to 12 per cent share evidenced during the two recent downturns between 2008 and 2009 and 2010 and 2012 (see chart)…

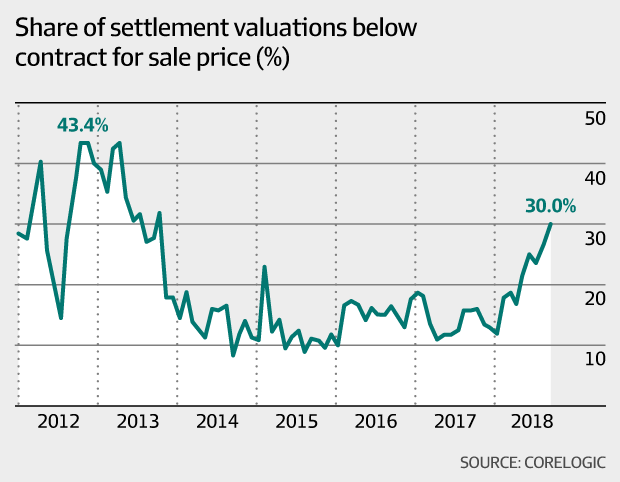

And with record numbers of apartments in Sydney, Melbourne and Brisbane still under construction, this pain is only likely to worsen. One leading indicator is the difference between the off-the-plan sales price buyers paid and the value of their property when it finally settles.

In April 2017, only 11 per cent of settlement valuations in Sydney were below the original purchase price. By September 2018 that had jumped to 30 per cent, although this is still less than the previous cyclical peak of 43 per cent in 2012 (see chart)…

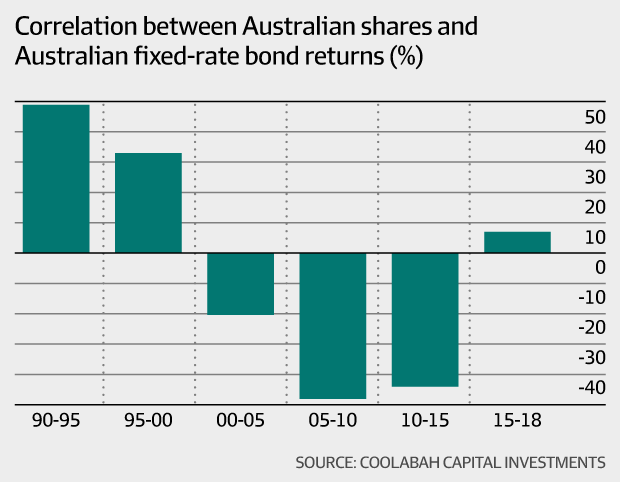

Last Friday I demolished the pervasive myth that investors should buy fixed-rate bonds as a hedge against equity losses. In particular, I showed that the long-term correlation between Australian equities and fixed-rate bonds has been on average zero since 1990 and punctuated by several periods when it was sharply positive (not negative).

One counter is that the mythical hedge fixed-rate bonds provide comes into play when equities fall. My response is that it depends on whether equity losses are being driven by an inflationary or deflationary shock.

To test this proposition, one of my quants looked at the correlation between Aussie shares (including dividends) and the fixed-rate Composite Bond Index over five-year intervals between 1990 and 2018. As the third chart shows, the correlation was clearly positive between 1990 and 1995 and 1995 and 2000 when central banks were still trying to convince markets they could be trusted to keep inflation within their target bands. (I believe this credibility will decay over time.)

The correlation turned negative in the first deflationary shock during the "tech wreck" in the early 2000s. This negativity increased over the next decade between 2005 and 2015, which spanned the GFC. Crucially, the correlation has swung positive again in the period since 2015 as global inflation has re-ignited.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

5 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment