How the rotation into unloved assets is boosting energy valuations

Nader Naeimi

AMP Capital

I’m going out on a limb and calling it now: 2018 will be the year of the unloved asset. In particular, investors in the oil and the energy sector will be well placed for a reasonably strong bounce back in the first half of this year, a shift that’s already begun to take hold.

Since trading started in January, US Oil Services and Global Energy indexes have risen 12 per cent and 7 per cent per cent, respectively, fuelled by a number of dynamics in the oil market we’ve been watching for a while.

Beyond watching, we’ve been allocating to this theme for some time.

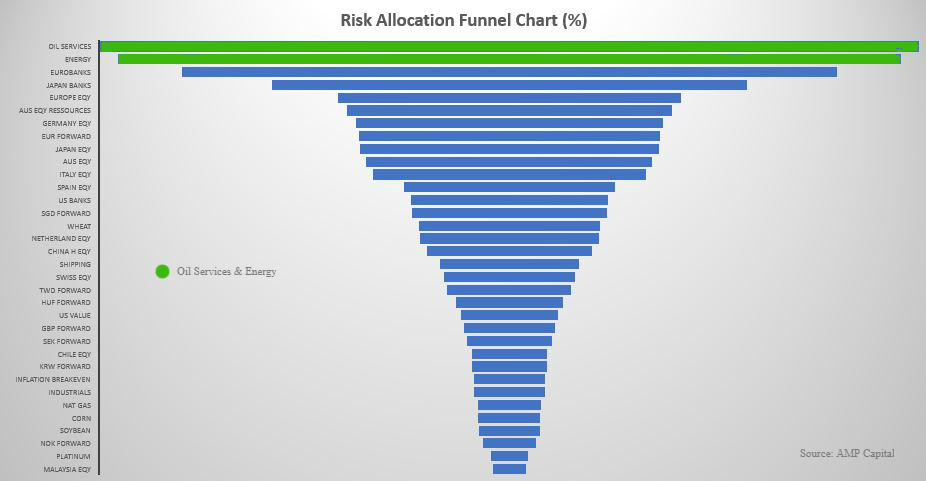

Currently, Oil Services and Energy accounts for by far the largest risk allocation in our Dynamic Markets Fund.

Late last year, I highlighted we’re about to see the return of inflation in the United States, a characteristic which has long eluded central banks and market watchers – despite almost full employment and with the help of easy monetary policy. I pointed to a fixed income exposure we’d taken in the fund to give us access to what’s essentially a break-even rate of inflation – so when inflation goes up, we don’t own duration but we maintain exposure to movement or the “spread” between nominal and inflation linked bonds.

Energy is another theme in the portfolio I’m particularly excited about and I believe our risk allocation in this area is about to start justifying itself.

Why oil, why now?

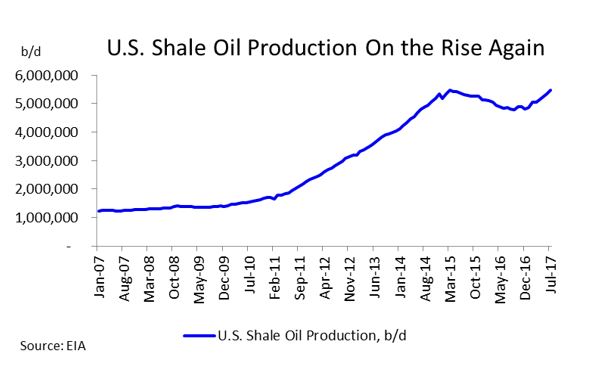

It is now almost a decade since the US shale revolution began. From almost nothing, production of oil and gas from shale rocks rose significantly over the earlier few years. Huge increase in oil supply, together with lacklustre demand led to a collapse in oil prices over 2013-2016 period – and resulted in a recession in the energy sector.

In 2013-14, the oil curve was in contango – a situation where the longer dated future prices were higher than the short term contracts or spot prices.

This unique situation allowed producers to dig more and more wells and sell more and more oil in the forward market.

Since the oil market has rebalanced, the forward oil curve has moved to what’s called “backwardation”, meaning spot prices are much higher than future prices. In this situation, shale producers can no longer hedge their production by selling oil in the futures markets because future prices are now much lower than spot prices.

Still, with oil prices on the rise, US shale oil producers are increasing their rig counts again.

Given the recent experience, investors in this market are looking ahead and worrying about the speed with which supply will come on like it did in 2013-14, leading to a derailing of the oil price recovery. As such, investing in the energy sector is still seen by many as a value trap.

But we actually see substantial opportunities in the energy sector. In fact, when you dig beneath the surface, the story is playing out very differently than the rest of the market expects.

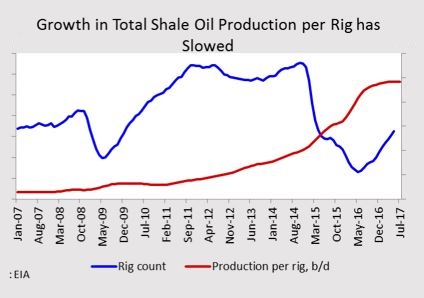

While a sharp jump in the rig counts in the past led to a collapse in oil prices, this was happening when shale producers began to maximise production by moving it to their most productive wells.

Many are missing the fact that that the 2016 recovery in oil prices and the jump in rig counts have come with falling rig productivity, Energy Information Administration data shows.

Indeed, it appears that oil productivity from newly drilled wells is declining. This is because shale producers have been forced to drill in less productive acreage. In other words, the low hanging fruit from the most productive wells has already been picked. From here, shale producers are going to chase their tail as any new production need to constantly offset the fall in production from existing wells.

The implication is that increasing new production from the current levels will be difficult. It seems likely, therefore, that US shale oil production will likely peak at least for now.

Peaking US shale oil production together with the synchronised global recovery that’s currently unfolding currently points to higher oil prices and significant upside potential in the energy sector in our view, a sector that has been so unloved and overlooked by investors for some time.

For the four years or so the energy recession has persisted, investors have been chasing other growth opportunities as well as allocating heavily to so-called “bond proxies”. The longer the equities bull market has continued, the more investors have gone for “quality” companies with the ability to grow or pay income. This flight to quality has become the most crowded trade in town.

Rotation from loved to unloved

Our bet on oil services and energy is two-fold, really: first, as mentioned above, we think the current supply-side dynamics for shale oil will prove less free flowing as it is widely believed. If this happens as we expect, the upside implications for energy and oil prices in particular are significant.

Second, we believe there will be a rotation out of some of the more favoured and expensive parts of the market and into areas that have been perceived to be a value trap and risky.

Related to this belief is the likelihood the market more broadly is overestimating the impact new technologies – such as solar, wind and water power generation – will have on traditional energy consumption.

People have bought the battery story pushed by the likes of Tesla’s Elon Musk, but it’s a two decade or more story while, in the short and medium term, our traditional energy demands still remain.

Finally, changing incentive structures for CEOs in energy companies is beginning to result in shifting management focus potentially dampening production and oil supply further.

After a significant loss of capital, US Shale investors are tired of “growth at any cost” and are demanding “return on capital” and “cash generation”. This has seen a profound shift of focus from “resource capture” to “value maximisation” by the management teams of energy companies.

All these factors bode well for energy investors who are more interested in quality corporate returns and less dazzled by the excitement of the shale boom.

For further insights from AMP Capital, please visit our website

Important note: Investors should consider the Product Disclosure Statement (PDS) available from AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) (AMP Capital) for the AMP Capital Dynamic Markets Fund (Fund) before making any decision regarding the Fund. The PDS contains important information about investing in the Fund and it is important investors read the PDS before making a decision about whether to acquire, continue to hold or dispose of units in the Fund. AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMPCFM) is the responsible entity of the Fund and the issuer of units in the Fund. Neither AMP Capital, AMPCFM nor any other company in the AMP Group guarantees the repayment of capital or the performance of any product or any particular rate of return referred to in this document. Past performance is not a reliable indicator of future performance. While every care has been taken in the preparation of this document, AMP Capital makes no representation or warranty as to the accuracy or completeness of any statement in it including without limitation, any forecasts. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. Investors should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to their objectives, financial situation and needs.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

As the Head of Dynamic Markets, Nader is responsible for leading the Dynamic Asset Allocation strategy for the Multi-Asset Group, as well as other macro strategies and asset allocations for several AMP Capital funds.

3 topics

Nader Naeimi

Head of Dynamic Markets

AMP Capital

As the Head of Dynamic Markets, Nader is responsible for leading the Dynamic Asset Allocation strategy for the Multi-Asset Group, as well as other macro strategies and asset allocations for several AMP Capital funds.

Expertise

Nader Naeimi

Head of Dynamic Markets

AMP Capital

As the Head of Dynamic Markets, Nader is responsible for leading the Dynamic Asset Allocation strategy for the Multi-Asset Group, as well as other macro strategies and asset allocations for several AMP Capital funds.

Expertise

Comments

Comments

Sign In or Join Free to comment