How I’m playing the return of inflation

Nader Naeimi

AMP Capital

Contrary to the conventional wisdom, inflation in the United States is not dead. Far from it. We believe inflation is coming back in a meaningful way and we’re preparing for its return by investing a portion of our portfolio in a fairly obscure fixed income ETF.

While I acknowledge there could be a million different ways to bet on the “return of inflation”, depending on when and how you want to allocate to it, the position we’ve taken in my view perfectly captures the other side of the bet the broader market is making, that static or negative inflation surprise in the US is set to continue.

Before I go into the what, a little on the why

Like most investors with a global view I’ve been glued to data coming out of the United States relating to GDP growth, wages and employment, waiting for signs that inflation will return (as it always does)

Once we see inflation kick in, surely we can take that as a sign global growth is much more broad based, and the US Federal Reserve will resume raising interest rates again. We see the Fed ratcheting up rates again in December.

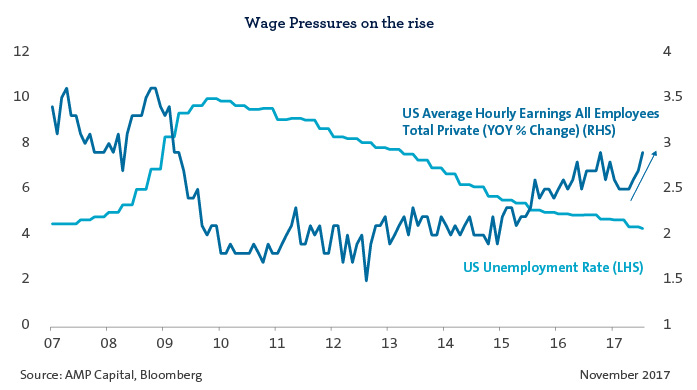

However, while all the signs of growth are there, inflation has so far been elusive: unemployment continues to come down, manufacturing is ticking up, but now there are signs wages growth is starting to come through.

Like most of you I’ve also been reading the commentary and listening to the momentum evangelists who are suggesting this time is different.

The “Amazon effect” has improved consumers’ price discovery so much it’s changed the state of play for companies which can’t earn the same margins – or so the narrative goes.

Disruption has knocked the wind out of pricing power as we know it and inflation could be a relic of an era when times were much simpler.

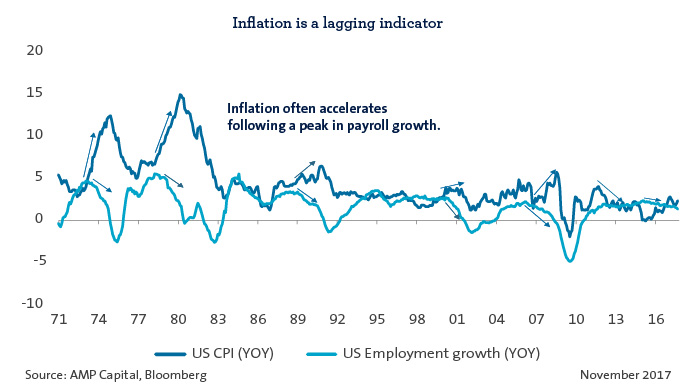

I don’t believe this time is different and I am already seeing signs that inflation – which people should be reminded is a lagging indicator – is coming back.

Look at the average hourly earnings among all employees in the private sector and consider the spending power that’s flowing back into the hands of consumers which will ultimately flow through to inflation.

After a number of years scrutinising the data, in between stop-start economic growth, I’m confident we’re reaching a point of escape velocity.

This phrase has been borrowed from aeronautical parlance and it’s perfectly suited to describing the behaviour of markets and economic indicators; escape velocity describes that moment when engine power has done all the hard work and the plane’s ascension into flight becomes a product of its aerodynamics.

The same thing is about to happen with economic growth in the US with inflation to follow.

Many thought we’d reach this point sooner; in 2014 the US unemployment rate dropped to 6 per cent by midyear, well below its great recession peak of 10 percent and other measures of labour market conditions continued to show significant improvement, US Fed Chair Janet Yellen points out in a recent lecture to the National Economists Club in Washington DC.

But inflation never really kicked in as most expected; inflation as measured by the change in the price index for personal consumption expenditures peaked at about one and three quarters of a per cent by mid-2014 after hovering around 1 per cent for some years. But remember, inflation is an incredibly lagging indicator and often emerges well after a peak in employment growth.

Projections for inflation continue to be modest with the Federal Open Market Committee predicting inflation could rise to 2 per cent in coming years.

Bond buying suggests the market is more pessimistic that inflation will return at all.

But our view is inflation will soon surprise to the upside and we’ve made an allocation in our Dynamic Markets Fund to take advantage of what we think the market is missing.

We’ve taken around 4 per cent or $72 million from our cash and nominal bond holdings and invested it in a fixed income exposure which gives us exposure to what’s described as the “break even rate of inflation”.

We’ve structured the trade such that when inflation goes we won’t own duration in our fixed income exposure.

Investing in this particular index cancels out duration but gives us exposure to movement or the “spread” between nominal and inflation linked bonds.

Since we started the Dynamic Markets Fund in 2011 there’s been market shifts – from the European debt crisis to the emerging markets banking crisis in 2014 – but this allocation represents the first portfolio decision directly tied to inflation.

Watch out, inflation is on the horizon!

For further insights about how we're thinking, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

As the Head of Dynamic Markets, Nader is responsible for leading the Dynamic Asset Allocation strategy for the Multi-Asset Group, as well as other macro strategies and asset allocations for several AMP Capital funds.

2 topics

Nader Naeimi

Head of Dynamic Markets

AMP Capital

As the Head of Dynamic Markets, Nader is responsible for leading the Dynamic Asset Allocation strategy for the Multi-Asset Group, as well as other macro strategies and asset allocations for several AMP Capital funds.

Expertise

Nader Naeimi

Head of Dynamic Markets

AMP Capital

As the Head of Dynamic Markets, Nader is responsible for leading the Dynamic Asset Allocation strategy for the Multi-Asset Group, as well as other macro strategies and asset allocations for several AMP Capital funds.

Expertise

Comments

Comments

Sign In or Join Free to comment