Investing in the right place at the right time

The following is an extract from a note that was recently sent to investors in the Montaka Global Fund. There is a famous quote attributed to Ray Kroc, the founder of McDonald’s (at least as we know it today): “The key to success is being in the right place at the right time, recognizing that you are there, and taking action!” This sensible piece of wisdom is also the essence of successful equity-market investing, in our view.

Investing in the right “place” is being on the right side of major themes and industry changes. Whether it’s the increasing value of big data to large online technology platforms, or the rise of the Asian middle-middle class, for example. It is also about being on the right side of macro changes: tax cuts in the US or tightening monetary policies globally.

But while investing with these tailwinds is typically better than betting against them, being in the right place is entirely insufficient on its own to ensure success. One must invest in the right places only at the right times.

Now, when is it the right time to make an investment? It is only when the market-implied expectations built into a stock’s price about the key value drivers of the underlying business are unreasonably conservative, in our view.

You might be investing in a rapidly-growing industry like 3D printing, for example. Five years ago, 3D printing leader, Stratasys (NASDAQ: SSYS), was growing at nearly 50 percent per annum; and consensus expectations were for revenues to triple again over the subsequent three years.

Now, Stratsys did grow quite significantly over the subsequent three years – but by far less than what the market was expecting. Said another way, the market-implied expectations built into the stock’s price in 2013 were too high.

And the result? An 85 percent reduction in shareholder value. Investors buying Stratasys stock in 2013 were arguably investing in the right place, just at the wrong time.

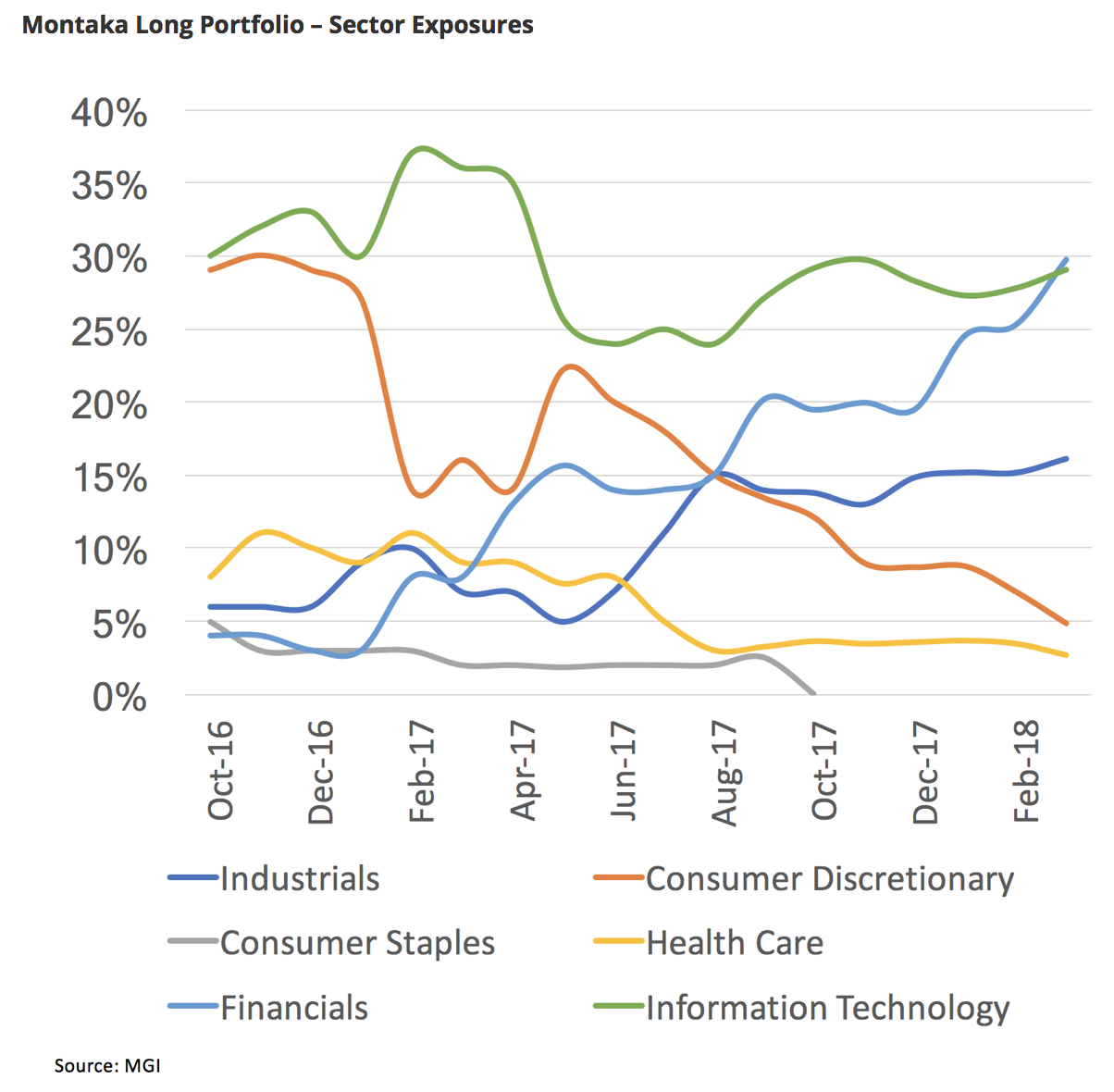

At Montaka, we seek to invest in the right places, at the right times. And this results in a very deliberate set of portfolio exposures that look very different to many other equity portfolios. Many equity portfolios – including index funds – invest in all places, at all times. As one can observe from the chart below:

Montaka is not exposed to sectors in which we cannot identify high-quality global businesses, with attractive future prospects, that are materially undervalued; and

In the sectors to which Montaka is exposed, the weightings will be significantly higher or lower when it makes sense.

This is what we believe investing in the right places, at the right times looks like.

If you would like to read more articles by me, please click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

2 topics

1 stock mentioned

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Comments

Comments

Sign In or Join Free to comment