Jupiter reaching for the stars

We were recently asked what we see in Jupiter Fund Management (LSE: JUP), a UK-based business owned in the Montgomery global portfolios. Without giving away our entire analysis, the following note seeks to lay out, in simple terms, why we believe this is a high quality global business that is currently undervalued.

First, a reminder of what the global team at Montgomery look for in potential candidates: (i) high business quality – meaning an inherent ability for the business to earn above normal returns on invested capital for a sustained period of time stemming from assets owned by the business that are difficult for competitors to recreate; and (ii) undervaluation – which we articulate as follows: the expectations built into the market price of the stock are unreasonably conservative. We address each in turn.

High Business Quality

A simple place to start in the identification of potential business quality is to look for evidence in the returns that have been generated on invested capital historically. In the case of Jupiter, this business has consistently earned returns on equity north of 20 per cent, well above its cost of equity which Bloomberg estimates to be 12 per cent.

It should be noted, however, that these returns on equity have been generated with Jupiter consistently holding a significant amount of cash (which earns very little). Stripping out this cash from the denominator shows us that the underlying business (excluding excess cash) has earned returns on equity of around 40 per cent consistently. And if we exclude goodwill that has been sitting on the balance sheet for more than a decade, then these returns are north of 50 per cent.

Now, high economic returns are typically a necessary but insufficient condition for the business to be of high quality. (High returns can be generated by low quality businesses from time to time due to lucky exogenous factors, but they don’t last). We then need to make a qualitative assessment as to what it is the business has that is scarce, valuable and difficult to recreate.

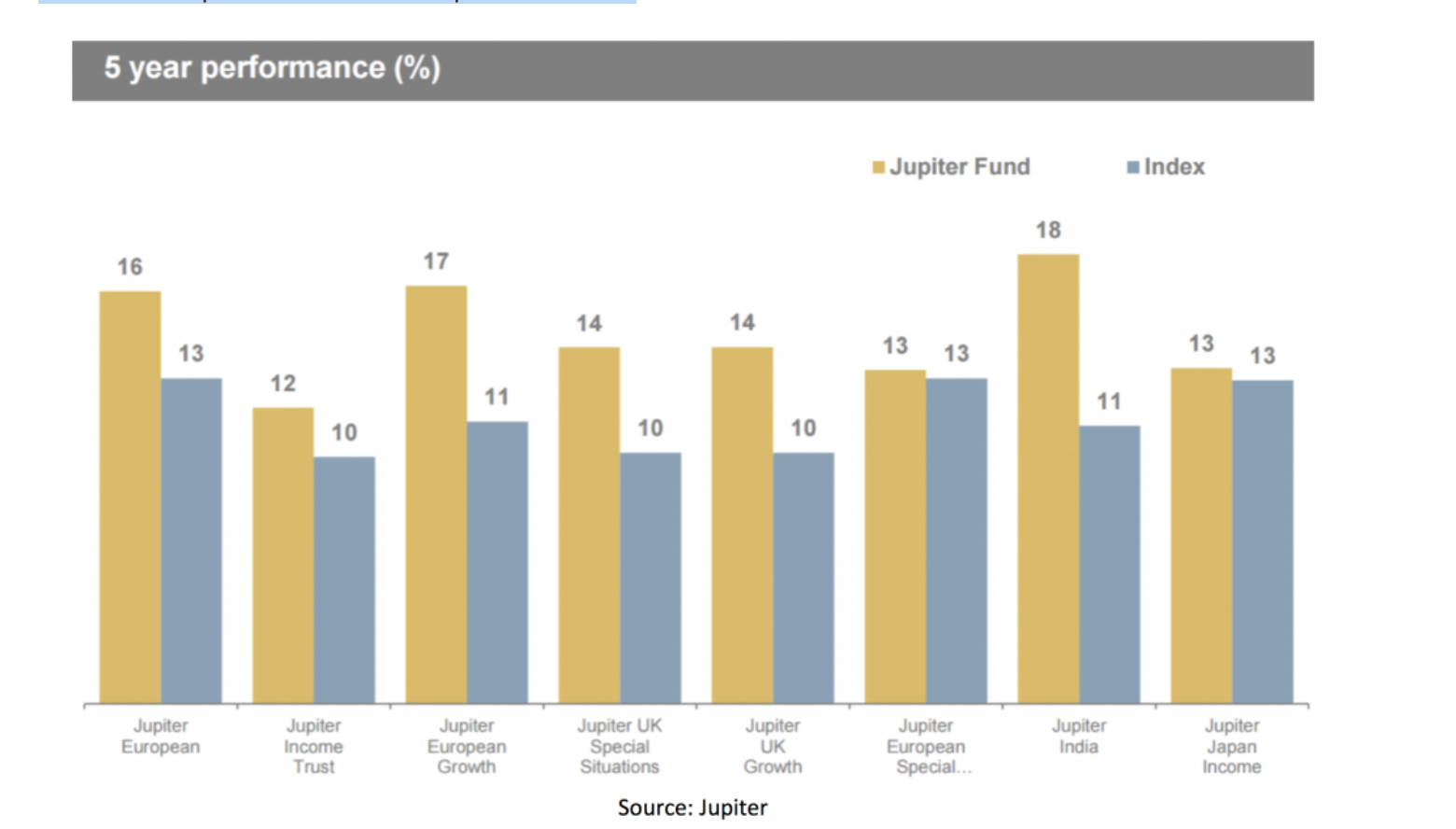

Jupiter is a high quality active manager of assets (equities, fixed income and multistrat) that started in 1985 as a boutique and has grown into a GBP44 billion fund manager. Over time it has built up a stable of high quality active managers (see below for evidence of performance); a significant multi-channel distribution apparatus (retail and institutional); and an institutional-grade operational back-end. This three-way combination of high-quality portfolio management, distribution and operations is required for success in funds management and is really not easy for competitors to recreate (something we know a little about, first hand). On this basis, we view Jupiter as owners of a high-quality asset that will be entitled to earn high returns on capital for a sustained period of time.

Undervaluation

Before we begin, let us again reiterate how we view stock prices: a stock price is simply a numerical representation of future expectations. These are expectations about key value drivers such as revenue growth, profit margins, capital intensity, etcetera. For us to conclude a stock is undervalued, we do two things: (i) we estimate what we believe are the expectations the market is building into the stock’s current price; and (ii) we make an assessment as to whether or not those market-implied expectations are reasonable or unreasonable – and why we believe our assessment to be true. As the saying goes: to outperform the market as an investor, you need to be different to the market and you need to be right. So we are always very clear about where we believe we are different to the market and why we believe we are right.

When asking what expectations are built into a stock’s current price, it is important to focus on which value drivers are the most critical. In the case of a fund manager, one of the key value drivers is new funds under management (FUM) inflows. New FUM inflows are also near-impossible to predict, other than to say they typically follow successful performance – which Jupiter’s funds clearly have.

Fortunately, with our approach to investing, we do not need to precisely predict what future FUM flows will be. Here’s why:

- When we recently added Jupiter to our portfolio, we analysed what expectations were built into the market’s current price at the time.

- By inputting assumptions we could reasonably predict with limited variability, we could back solve for the key assumption we have no ability to predict: new FUM flows.

- At the price we paid for Jupiter, the market was essentially implying no new FUM flows for the rest of time! The market was still implying revenue and earnings growth, but this was entirely stemming from the organic growth in equity markets, in our view.

- So to buy the stock and generate outperformance on this name, all we needed to be able to assert with confidence was that Jupiter’s net new FUM flows over time would be greater than zero. Given Jupiter’s track record of successful performance, this was an easy bet for us.

So there we have it: high business quality which we believe will enable Jupiter to generate high returns on capital for an extended period of time; and a stock price that was building in market-implied expectations that were unreasonably conservative. Or said another way: (i) high business quality; and (ii) undervaluation.

While this all sounds quite simple, and in a sense it really is that simple, it is not easy to identify these opportunities. We were “stalking” Jupiter for at least 18 months prior to our most recent purchase of their shares, biding our time for when the market-implied expectations became simply too conservative to pass up. And there were exogenous risks around Europe (think Brexit, the Italian Referendum and the French election) that rendered this business uninvestable, in our view, for a period of time. We believe these risks have now subsided and the quality/risk/reward equation is now right to own this business in our global portfolios.

The Montgomery Global Funds owns shares in Jupiter Fund Management

Are you looking for a simple way to invest in high quality global businesses? Applications to the new Montgomery Global Equities Fund are now open. To access the PDS and find out more, please visit the MOGL website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

3 topics

1 stock mentioned

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Comments

Comments

Sign In or Join Free to comment