Livewire readers' top stock ideas for 2017

In December, we asked Livewire readers for their view on a range of market issues for the year ahead. As part of this, you shared your best stock ideas with us. We received 601 responses to this question, with 276 unique stock ideas. The most popular ideas this year showed two clear themes; 1) The reflation trade continues, and 2) High-growth mid-caps recover. Only time will tell if these themes play out. Last year’s top ideas performed well, with an average price return of 12.4% for the year (dividends not included), with the most-tipped stock (BHP) putting on 36%. The ASX200 price index returned 8.8% over the same period. In this article, I’ll share the top 20 most popular stock ideas from their year’s survey, and some comments from fund managers and brokers on the top 5.

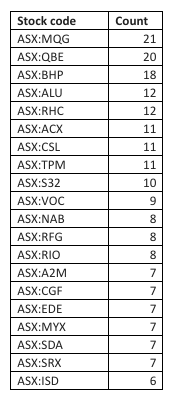

The list...

Macquarie (MQG)

John Murray from Perennial Value Management

In December, John put a ‘Buy’ rating on MQG in Buy Hold Sell.

“I like Macquarie. I think it's reasonable value at these levels. I think it's run by one of the best management teams in the country. In the longer term, I think there's a global infrastructure story which will come on the back on increased fiscal expenditure, and you may see that, for example, come out of the biggest economy of the world, being the US, on the back of Trump. So, I like the thematic of Macquarie over a five-year few from here as well.”

Source: (VIEW LINK)

TS Lim from Bell Potter

In December, TS Lim put a ‘Buy’ rating and a $90 price target on MQG in his “Bank Note$” report.

Source: (VIEW LINK)

Shane Fitzgerald from Monash Investors

In November, Shane put a ‘Hold’ rating on MQG in Buy Hold Sell.

“Macquarie’s one of the world’s biggest managers of long-duration assets: infrastructure and equity investments. So, backing up in bond yields has to have an effect. More fundamentally than that, the ROE of this business is about 13%. Its capital intensity has not changed. It’s a pretty fair value for us.”

Source: (VIEW LINK)

QBE Insurance Group (QBE)

Hugh Dive

In November, Hugh identified QBE as a stock likely to benefit from higher rates.

“QBE Insurance will be one of the biggest beneficiaries on the ASX from rising bond yields, though given the company’s somewhat tortured relationship with investors. As an insurer, the company holds US$23 billion in cash and short-dated debt as a “float” (this occurs as premiums collected before claims are paid out). While QBE has managed this float well. Nevertheless, it has generated meagre returns in this period of low rates. A mere 0.5% increase in interest rates will add over US$100 million to 2017 net profits or boost reported profits by 11%.“

Source: (VIEW LINK)

BHP Billiton (BHP)

John Murray from Perennial Value Management

In December, John put a ‘Buy’ rating on BHP in Buy Hold Sell.

“They have had a good run, but I think the really interesting thing about the resources is if the spot prices stay anywhere near where they are now, and they've come up a long way since earlier this calendar year. If they stay anywhere near where they are, whether you look at a BHP, or a South32 or Rio, the free cash flow generation is going to be unbelievable. It's going to be much stronger, ironically, at the bottom of the cycle now than what it was at the top of the cycle. Remember earlier this year Matt that the big companies, specifically Rio and BHP, they committed to payout ratios between fifty and sixty percent, broadly. If their earnings go way up, as we think they could well do over the next year or so, their dividends are going to go way up as well in terms of payout, just rising cash flow.”

Source: (VIEW LINK)

Andrew Fleming from Schroders Australia

In December, Andrew identified long-run commodity prices as a key issue for Australian stocks.

“The strong relative performance of recent months has seen the valuation case for BHP Billiton, Rio Tinto and South 32 diluted, albeit in every case we still have some upside to valuation.”

Source: (VIEW LINK)

Altium (ALU)

Ben Clark from TMS Capital

In December, Ben identified Altium as his best stock idea for 2017 in Livewire’s Outlook Series.

“Staying with the Small Cap theme I'll go with Altium. We thought it had one of the best results in the August reporting season with a meaningful upgrade on its long-term revenue guidance. Great management, structural growth in their industry, and they're growing faster and taking market share. A possible catalyst will be the continued alliance with Dassault Systems, the French software giant.”

Source: (VIEW LINK)

Roger Montgomery from Montgomery Investment Management

In September, Roger commented on the most recent results from Altium.

“[Altium’s result was one] of the reporting season’s best (and it might) be one of the best value propositions on the ASX.”

Source: (VIEW LINK)

Ramsay Health Care (RHC)

Ben Macnevin from Montgomery Investment Management

In September, Ben commented on the fund’s recent purchase of Ramsay Health Care.

“Ramsay is one of the top private hospital operators in the world. It’s been a stellar performer on the ASX and, in its recent financial report, signalled more solid growth to come.”

Source: (VIEW LINK)

Prasad Patkar from Platypus Asset Management

In September, Prasad put a ‘Buy’ rating on RHC in Buy Hold Sell

“We own it. We think it’s got a fantastic franchise, and a global footprint now. So, many years of low double-digit percentage growth in front of it.”

Source: (VIEW LINK)

Romano Sala-Tenna from Katana Asset Management

In September, Romano disagreed with Prasad, putting a ‘Sell’ rating on RHC in Buy Hold Sell

“The movement in France, while it’s good, does expose them to a lot more regulatory risk, as it does in Australia at the moment. Unfortunately, we see it as a Sell; it is a great company, but there’s a lot of risk now, and the balance sheet is stretched.

Source: (VIEW LINK)

What did last year's winner pick?

Jon Dixon from Dixon Financial Group in WA picked Galaxy Resources which was the top performing stock from the 2016 Outlook Survey. We jumped on the phone to hear a bit about his strategy and his pick for 2017. Given Jon is based in WA he says he is drawn to the resources sector, largely due to the flow of information he gets from being close to the industry. He describes his style as generally pretty conservative but he does like to take some small contrarian positions in out of favour stocks, which is what you get with Atlas Iron (AGO) - his pick for 2017. Atlas started the year at 2.7 cents and has already run up to 4.5 cents, and Jon concedes he has already sold down 50% of his position. He says that he perceived limited downside from the already beaten down price, however, it was one of the few iron ore companies that hadn’t yet rallied. He’s off to a good start, but it’s early days.

Dixon Financial Group: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

1 topic

17 stocks mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets