Looking for opportunity in LIC land

William Gormly

Bell Potter Securities

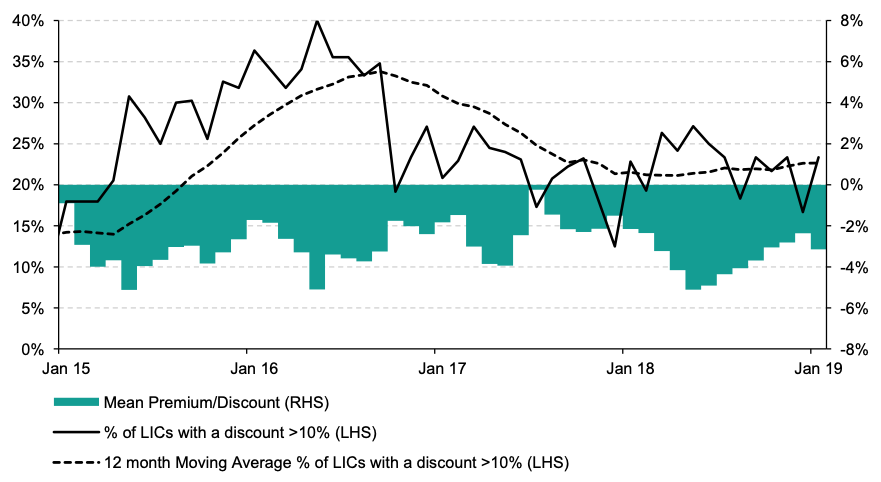

Listed investment companies (LICs) can provide investors with an interesting opportunity; purchasing a portfolio of securities below the intrinsic NTA value. However, 30% of the 114 LICs were trading at a discount greater than 10% at the end of January.

In comparison, 23% of the 60 securities covered in the Bell Potter LIC reports were trading at a discount greater than 10%. These LICs represent ~90% of the sector and are generally the largest and most liquid securities whilst providing a range of mandates in an attempt to accurately represent the overall sector.

LICs with a market capitalisation less than $100m make up 50% of the sector, although they currently represent 74% of LICs with a discount greater than 10%.

An overwhelming 81% of LICs with a market cap below $100m trade at a discount. This is partly due to smaller LICs commonly holding smaller share registries, having lower trading liquidity and higher fixed costs per share.

Analysing the 60 LICs in the Bell Potter universe, the current level is trading around the 12 month moving average and lower than what has been experienced over the past 4 years. On an equal-weighted basis, the average discount to NTA has gradually declined over the past 6 months.

Source: IRESS, Company Reports, Bell Potter Research. Data as at 31 January 2019

LIC's trade around their historical average premium (or discount)

A common misconception surrounding the discount is that it will return to trading at par or even at a premium. Whilst purchasing a LIC at a discount to NTA can provide an added windfall of gains from the discount reducing over time, this should not be solely relied upon.

If we look at the 14 LICs in the Bell Potter universe that are trading at the discount greater than 10%, there is an average of ~2.5 years since they last traded at par. And there are 2 LICs have consistently traded at a discount over the past 5 years.

A more observable trend is that LICs will trade around a mid-to-long term average premium/discount to the NTA.

Changes in manager performance and investor sentiment are two factors that cause the premium/discount to trade away from the historical average, potentially providing buying opportunities.

- Changes in manager’s performance from month to month is likely to have a more sustained impact on the long term premium/discount due to the higher correlation of performance in one month occurring in a future month.

- In contrast, changes in investor sentiment in certain LICs can rapidly change. From 21 Dec 18 until 10 Jan 19, the L1 Long Short Fund (LSF) share price rallied 19% whilst closing a discount to the NTA of 10% to 0%. The discount has since widened out to 9% as at 1 Mar 19, as the positive NTA return of 6% coincided with a -4% change in the share price.

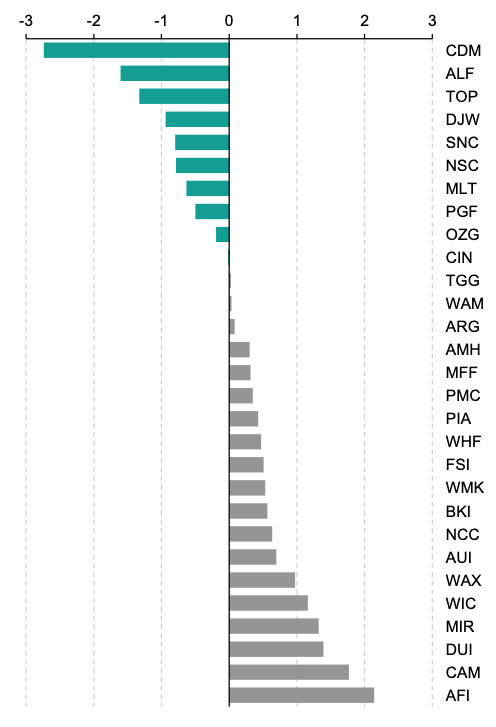

Using a Z-score to track the premium/discount to NTA

Readers of the Bell Potter LIC Weekly Report (You can access the latest weekly report here) may be familiar with the process of analysing a LIC’s Z-score to determine whether or not the current deviation from the long term average is significant. This is calculated by dividing the difference between the current premium/discount and the historical average by the standard deviation of the same period.

A Z-score calculates how many standard deviations the current premium/discount is away from the historical average. A positive Z-score indicates a current premium/discount that is less attractive to the historical average in terms of value, and a negative Z-score would be considered more attractive.

For example, in Figure 2 below, Cadence Capital’s (CDM) Z-score indicates that the premium/discount of -10.7% is approximately 2.7 standard deviations below the 5 year average premium/discount of 6%.

Carlton Investments (CIN) premium/discount of -11.6% is close to the 5 year average premium/discount of 11.5%, with a low monthly standard deviation of 1.6%. Investors speculating that the CIN discount to NTA will reduce in the short term may need to rethink their investment strategy if solely looking at the Z-score. That being said, CIN has a share price return of ~8% p.a. over the last 5 years. Another limitation is that the Z-score calculation assumes that the data is normally distributed which may not be the case in reality.

Figure 2: 5-year Z-scores

Source: Company Reports, Bell Potter Research. Data as at 31 January 2019 and includes LICs covered by Bell Potter with 5 full years of performance history.

In theory, and often in practice, purchasing a LIC at a discount can provide the added gain from effectively obtaining a portfolio of stocks at below the market rate. As we’ve seen, this isn’t always the realised outcome.

The most important decision in buying an LIC is choosing the right investment manager. You should seek to choose a manager whose investment beliefs and objectives are closely aligned with your own. You are trusting them in preserving your capital and financial interests. Above all, managers are expected to provide value by delivering a total shareholder return in excess of the benchmark over the investment timeframe.

New competition for LICs

The rise of low-cost index-tracking ETFs has increased the pressure on LICs to outperform.

In a similar way, a new popularity around the emergence of Active ETFs and Exchange Traded Managed Funds will inevitably continue to push for greater transparency in LIC products.

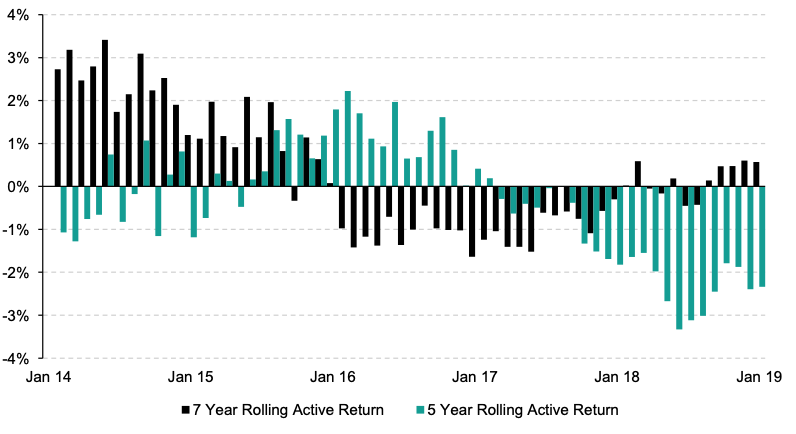

With recent commentary over Australian fund manager’s poor 2018 performance against the market index, it is worth mentioning how difficult it is to accurately judge a LICs performance based solely on a calendar year. The majority of managers seek to outperform the benchmark over the mid-to-long term (3-7 years). As at 31 January 2019, AFIC (AFI) had underperformed the benchmark (S&P/ASX 200 Accumulation Index) by 2.3% p.a. over the past 5 years, calculated on monthly compounded share price return (incl. dividends). Looking at the past 7 years, AFI has outperformed the benchmark by 0.6% p.a.

Figure 4: Rolling active return of AFI with ASX/S&P 200 Accumulation Index

Source: Company Reports, Bell Potter Research. Data as at 31 January 2019.

Selective timeframes can complicate performance analysis of a manager’s ongoing ability to deliver value to shareholders. It is worth noting that even the SPDR S&P/ASX 200 ETF (STW), which seeks to closely match (before fees and expenses) the returns of the S&P/ASX 200 Index, underperformed the benchmark by 0.3% p.a. over the past 5 years. This low-cost ETF also has a higher management cost compared to AFI’s management expense ratio, 0.19% and 0.14% respectively.

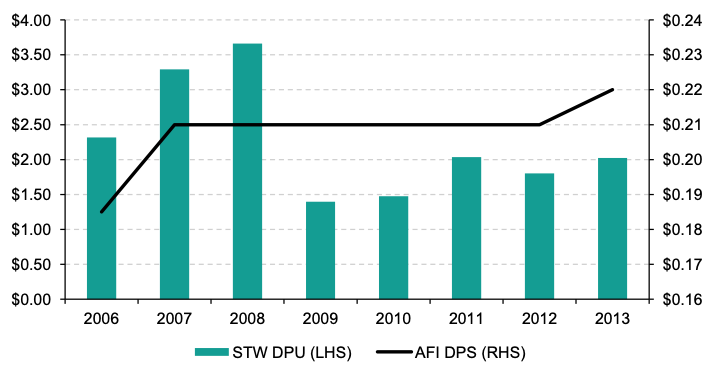

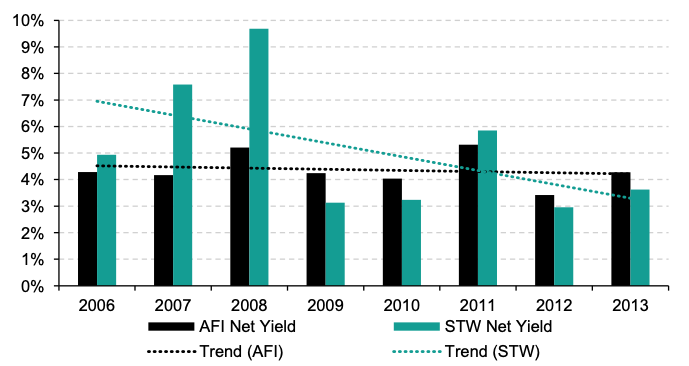

An added benefit of a company structure over a trust is the ability to retain earnings over periods and maintain franking credit accounts. This can enable a LIC to pay out smooth and sustainable fully-franked dividends over a long term, including periods of poor portfolio performance. This is highlighted below by AFI’s ability to deliver a constant dividend during the GFC whilst the distribution from STW more than halved. This feature has been vital for the many investors who rely on regular income streams.

Figure 5: Comparison of distributions paid over the GFC

Source: Company Reports, Bell Potter Research.

Figure 6: Comparison of yield over the GFC

Source: Company Reports, Bell Potter Research.

How will Labor’s proposed franking credit policy affect the LIC sector?

Franking credits are obtained by LICs via two sources, received from the distribution of underlying holdings and from paying company tax. These can be held over periods in order to be smoothly distributed to shareholders in the form of fully-franked dividends, where the franking credits can be used to offset tax payable. And, if in a low tax bracket, shareholders will receive a cash refund when franking credits exceed tax paid. Labor’s proposal is to remove the cash refund.

Looking outside of the impact of this proposal on the many LIC shareholders classified in a low tax bracket, it may ultimately make a listed investment trust (LIT) structure more appealing for managers and shareholders.

LITs won’t pay tax and will be required to distribute all profits to unitholders, which may lead to a higher yield. However, the volatility in distributions between periods will also increase which increases uncertainty over future income inflows.

One exceptionally well-managed LIC over the short-and-long term

Bell Potter recently released its top stock picks for 2019, in which we highlighted 3 LIC's to consider.

As an investor, you should seek to choose a manager whose investment beliefs and objectives are closely aligned with your own.

An example of one exceptionally well-managed LIC over the short-and-long term has been MFF Capital Investments (MFF). The company primarily invests in large listed international companies that have attractive business characteristics at a discount to their assessed intrinsic value.

It also has the ability to invest in domestic securities, despite not currently holding any significant positions, and to add leverage to the portfolio, with net borrowings limited to 20% of investment assets. For the 10 years ending 31 January 2019, MFF has returned 18.4% p.a. (incl. net dividends) compared to the MSCI World Net TR (AUD) return of 10.1% p.a.

Whilst we acknowledge that past performance may not be an accurate representation of future returns, the company has a strong track record of maintaining a relatively condensed portfolio of high quality companies and delivering double digit returns. The Board has also announced its goal to increase the half-yearly dividend from 1.5cps to 2.5cps. No timeframe has been provided.

Under a service agreement, the company pays research and service fees of $1m per quarter to Magellan Asset Management (MAM) and a performance fee of $1m p.a. to MAM if the total shareholder return exceeds 10% p.a., annually compounded. An amendment to the agreement was made to remove MAM’s entitlement to receive a performance fee for periods after December 2019. Annualising the ongoing expenses from the 1H19 results, the company’s management expense ratio is very competitive at ~0.50%, or ~0.43% after the removal of a performance fee payable.

--

Disclosures:

L1 Long Short Fund (LSF): Bell Potter Securities was a Co-Manager for this IPO in April 2018 and received a fee for the service.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Will provides comprehensive coverage of the ETF and LIC sectors, producing a range of highly regarded reports covering investment fundamentals, asset class structure and cost, and the role of managed investments in portfolios.

1 topic

9 stocks mentioned

William Gormly

ETF/LIC Specialist

Bell Potter Securities

Will provides comprehensive coverage of the ETF and LIC sectors, producing a range of highly regarded reports covering investment fundamentals, asset class structure and cost, and the role of managed investments in portfolios.

Expertise

William Gormly

ETF/LIC Specialist

Bell Potter Securities

Will provides comprehensive coverage of the ETF and LIC sectors, producing a range of highly regarded reports covering investment fundamentals, asset class structure and cost, and the role of managed investments in portfolios.

Expertise

Comments

Comments

Sign In or Join Free to comment