Low interest rates and stock valuations

On Wednesday last week the Australian Bureau of Statistics (ABS) reported that inflation for the June quarter was 0.4%, down from 1% in 2015. This is watched very closely by the market, as it is a key measure used by the Reserve Bank of Australia (RBA) in making their decision on the official cash rate and increases the probability that the official rate will be cut to 1.5% in August.

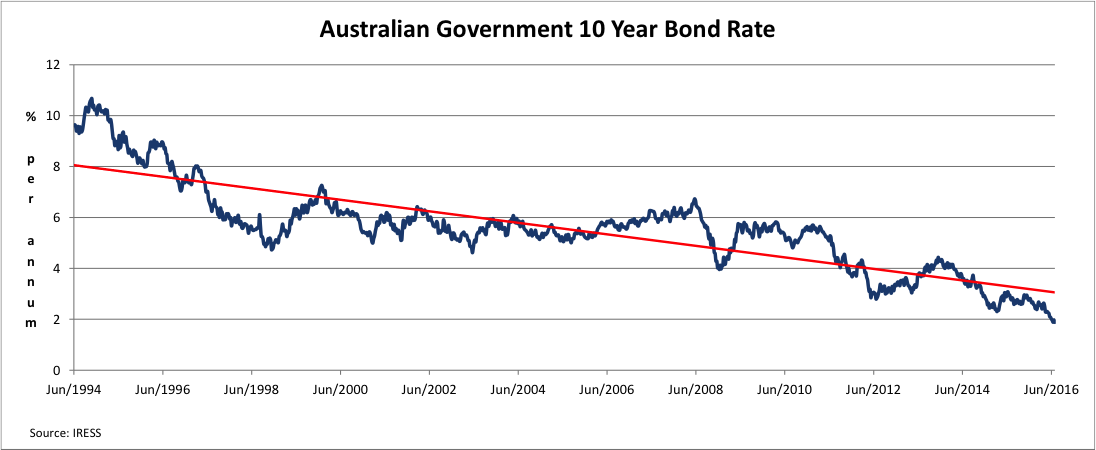

Low interest rates not only impact retirees looking to live off the income but also contribute to asset price inflation. While this might not be the most exciting of topics, it is important to investors, as assets from shares to real estate are currently being priced with the anticipation that historic low interest rates will continue into perpetuity! In this piece, I look at how the steady twenty-year fall in the 10-year bond rate has contributed to this current asset price bubble.

Valuing a Company

Share prices can move wildly day to day with changes to market sentiment, for example in 2016 we have seen Westpac’s share price average $30.30, but the price has oscillated between highs of $33.50 and lows around $28. These swings represent a change in the overall valuation of Westpac in the magnitude of A$18 billion. Over this short period, the bank’s core business of providing residential mortgages has not changed greatly, just sentiment towards the company.

The father of value investing Benjamin Graham famously said 'In the short run, the market is a voting machine, but in the long run, it is a weighing machine.‘ Determining a value for the expected returns from owning a stock helps investors retain some sanity and guides buy and sell decisions, as it forces you to think about the actual prospects for the business such as cash flows and debt levels away from market noise.

The most common valuation methodology used is a PE multiple, which compares a company’s market capitalisation to its annual income. Here the lower number is, the better as it represents how many years of current profits are required to cover the purchase of a share today (Commonwealth Bank at PE multiple of 12 times represents 12 years of profits, whereas Facebook at 60 times represents 60 years). However, the weakness in this method is that it influenced by market sentiment, with minimal connection to a company’s future earnings or dividends.

Discounted Cash Flow

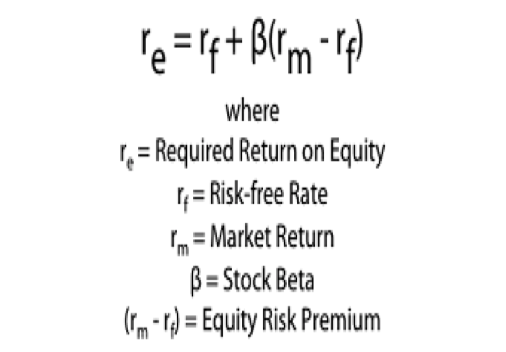

The two most common valuation methodologies used by institutional investors are the discounted cash flow (DCF) and dividend discount model (DCM). Here a stream of expected free cash flows or dividends from owning a company are discounted back to obtain a present value, which is then used to justify a buy or sell decision. This methodology requires the analyst determining the appropriate discount rate used to calculate the net present value of these cash flows. This discount rate is the rate of return that is required to invest in a company or business venture. Investors will want a higher the discount rate for riskier investments.

The discount rate used is the weighted average cost of capital (WACC), which is the average rate of return a company expects to compensate both its debt and equity investors. The weights are the fraction of each financing source in a company’s capital structure. The cost of equity is the rate of return that investors require to make an equity investment in a firm. This is calculated using a) Risk-free Rate b) the company’s share price volatility (beta) and c) a premium that investors require to invest in stocks over risk-free assets (equity risk premium).

Garbage in Garbage out!

Discount rates are a critical ingredient in discounted cash flow valuation and mistakes made in estimating the discount rate or mismatching cash flows and discount rates can lead to serious errors in valuation. Intuitively the discount rate used should be consistent with both the riskiness and the type of cash flow being discounted. The twenty-year fall in Australian interest rates has not only impacted returns from term deposits but has exerted an uplifting force on the valuation of all assets that generate cash flows.

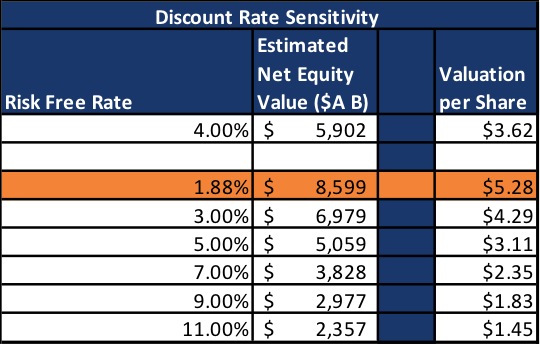

In the table above is the output of a discounted cash flow valuation for Incitec Pivot a large chemical company that is currently in the Aurora Dividend Income Trust (AOD) portfolio. In this table I have kept the all the variables constant, other than varying the risk free rate. Normally an analyst will use the prevailing Government 10 year bond rate, but if this was used I would have come up with a valuation of $5.28 or 45% above my current valuation! From observing this stock over the past decade it is hard to see this company generating sustainable earnings that would support a valuation above $5 per share.

Rates will rise, someday

Additionally, the valuation table above shows the impact of rising interest rates on the valuation of this industrial company. Whilst buying the income stream represented by owning a share in the company is attractive to me today with Incitec Pivot trading just below $3 per share, sharp upward moves in interest rates would convert what appears to be an undervalued stock today with interest rates below 2%, to wildly overvalued using this very common valuation measure at 7%.

Our Take

Falling rates combined with quantitative easing have stimulated demand for hard assets globally, as these declining risk-free rates have acted to boost valuations. However, it would be a mistake for investors to think that the current environment of ultra-low interest rates globally is a permanent fixture, as the average interest rate on Australian government bonds over the period 1975 to 1995 was over 10%! Rising rates may make current projects and investments uneconomic in the future. In our valuation methodologies, we stopped using the Australian government benchmark bond as the risk-free rate when it fell below 4%, and I feel that this may turn out to be insufficiently conservative.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

5 topics

3 stocks mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment