Notable themes and stocks this reporting season

JCP Investment Partners

JCP Investment Partners

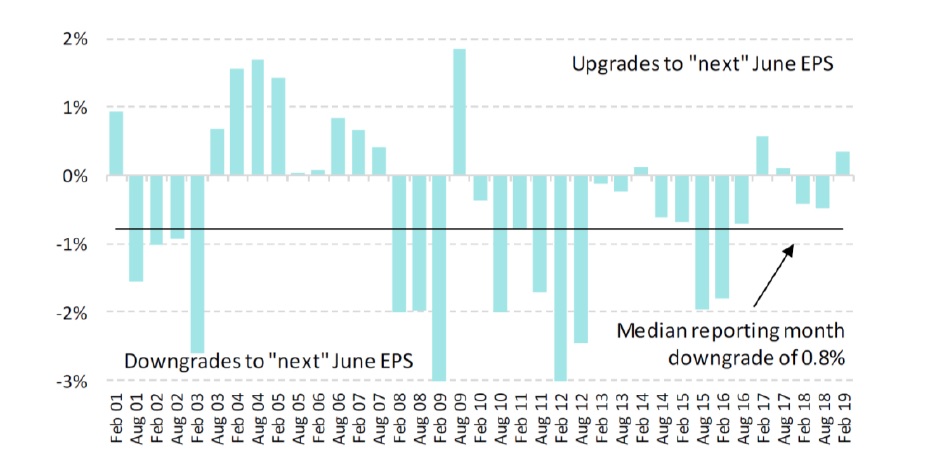

The reporting season in Australia completed in February. Overall, reporting season exceeded low expectations, with consensus June 2019 forecasts being upgraded marginally (aggregate revisions to June 2019 profits were upgraded by 0.3%). Consensus bottom up eps growth forecasts for the June 2019 year now stand at 6.3%. This is dominated by commodity producers, (ex-commodities the forecast falls to 2.4%). Commodity producers saw the largest upgrades (due to stronger commodity prices), whilst other sectors generally experienced downgrades. Distributions were a key theme; with dividends increasing by 4.3% (June 2019 DPS) and an additional $3.5bn of new buybacks were announced. Stronger balance sheets and the potential for the ALP to form government whereby the value of franking credits will be diminished, influenced corporates to return capital to shareholders.

The low expectations leading into reporting season helped the market stage a reasonable rally in February. We expect the market strength to subside after fundamentals are fully digested and now view the market around fair value from a bottom-up valuation perspective.

ASX200 EPS upgrades/downgrades [12 months to June]

Source: Company Data, Factset. MST Marquee

The clear standout sector this reporting season has been the commodity producers, that have benefitted from stronger balance sheets and higher commodity prices due to Chinese stimulus and supply disruptions. The Health Care and Software sectors also experienced upgrades, benefiting from operational leverage.

Some of the stronger results at the company level included Goodman Group (GMG), Insurance Australia Group (IAG) and Magellan Financial Group (MFG).

The Banking sector enjoyed a relief rally post the release of the banking Royal Commission’s final report and trading updates that suggested that all things considered they are in reasonable shape. Credit is benign; however, revenue is soft with low asset growth, front book discounting, switching from interest only to P&I mortgages and lower fee income all providing headwinds. To offset this pressure, all institutions are focussed on managing costs well. Overall, we see very little growth in earnings per share for the banks. In our view, they trade near fair value with downside skew, due to the cyclically low level of bad debts and potential for further capital headwinds resulting from the RBNZ’s sectoral review.

Industrials generally reported lower sales and margins, with softer results from consumer exposed companies due to belt-tightening. Traditional Media and Food Retail also experienced weaker results. The weakness in supermarkets was surprising.

At the company level, some earnings misses were recorded by Carsales (CAR), Cochlear (COH), Whitehaven (WHC), Stockland (SGP) and Coles (COL)

Key Themes from reporting season

1: Capital management

Australian companies are enduring a low growth backdrop. Balance sheets and cashflows are strong enough to support large distributions. Across the market, dividend forecasts increased by $3.6bn or 4.3%, being the largest upgrades to dividends in 20 years. There were also seven new buybacks announced totalling $3.5bn. The stronger capital management tells us there are a lack of incremental investment opportunities that deliver a return higher than corporate’s cost of capital.

Some of the off-market buybacks were clearly encouraged by the likely change of government, given the ALP’s plan to remove refunds on franking credits. In addition, stronger cash flows from commodity companies was another key driver to return capital.

Some of the larger capital initiatives we noted were:

- Brambles (BXB) – $2.3bn return post the IFCO sale. The return of capital will be via US$300m in cash, with the remaining US$1.65bn through on-market buyback

- Rio Tinto (RIO) – $4.0 billion return of Grasberg and Dunkerque proceeds via special dividend

- Qantas (QAN) – $500m capital return including $305m buyback and $195 fully franked dividend

- Wesfarmers (WES) – $1.1bn special dividend

- Suncorp (SUN) – $600m return of capital to follow the completion of the Life Company sale, part of which will be a special dividend.

- Caltex (CTX) – $260m buyback announced

- Janus (JHG) – $200m buyback announced

2: Offshore growth exceeds domestic growth

Emphasising the lack of growth across the market, it was clear that Australian companies are more buoyant about their prospects offshore.

• CSL noted demand was strong for the company’s core immunoglobulin products, with sales for Privigen and Hizentra up 17% and 14% respectively. Growth in specialty products continues to track well, with sales up 13%, and 21% growth in the flu business has the unit on track to reach $1bn in revenue.

• Nanosonics (NAN) rallied strongly following an impressive first half yearly result. The install base in the US continues to grow and is on track for our forecast penetration rate of 42% for FY19. Importantly, the company gave its first indication of price rises for Trophon 2, as well as margin uplift from the new GE Healthcare contract that commences in July. Elsewhere, news on the install base in Europe and Japan are positive and tracking well. The company is doing a good job of managing costs while building a strong balance sheet with good cash flows. We remain comfortable with our position in NAN, especially with the market now gaining confidence that the company is in fact a consumables business.

• Magellan Financial Group’s (MFG) result again exceeded expectations. The company posted a strong interim profit, boosting performance fees and growing management fees driven by investment performance and organic FUM growth. We remain attracted to MFG, as a well-run funds management business that is leveraged to global equity markets.

3: Domestic risks have increased

Domestic risks have risen, particularly in pockets with large exposures to housing and discretionary spending.

• Stockland (SGP) fell following a downbeat full year outlook. SGP expects growth in annual funds from operations to be at the lower end of the 5-7% target range, while net profit for the half to December 2018 fell by 56%. While residential settlements are yet to see a significant impact from the property downturn, the company has seen a significant decrease in inquiries and deposits. However, with SGP significantly exposed to the retail sector via its commercial property arm, we believe risks are still to the downside. Mirvac (MGR) and Lend Lease (LLC) also have some settlement risk ahead with large 2H skews.

• Domino’s Pizza Enterprises (DMP) retreated after the company guided to full year earnings being at the lower end of guidance, between $227m – $247m. First half sales growth was at the bottom end of the 3-6% target range, as the maturing Australian business slowed, and franchisee profits were down.

• Supermarkets (WOW & COL) had weaker top lines, providing a realisation that the consumer is weaker than previously expected.

• Woolworths (WOW) fell after its first half result showed food sales in Australia slowed last quarter, as subdued domestic confidence and falling property values led to consumers adjusting shopping behaviours by buying cheaper groceries. We remain positive on WOW, as it continues to reinvest into its stores, supply chains and building an online offering for customers. With the $1.7bn sale of its fuel business now approved by FIRB, we expect a substantial return of capital to investors.

• Coles Group (COL) delivered a result that was 5% below market expectations. LFL sales were weaker than expected, margins were lower and CODB higher.

• Carsales.Com (CAR) delivered a disappointing result dragged down by their Display and Stratton divisions. The Display business experienced a 20% decline in display advertising.

4. Cost pressures

Cost pressures were evident this reporting season, particularly amongst Industrials. Gaming, Health Care and Materials also hinted at rising cost pressures, while Diversified Financials flagged higher costs associated with remediation, restructuring and compliance.

Examples of cost pressures included:

• James Hardie Industries (JHX) result was slightly soft, highlighting the tough operating environment in North America that was impacted again by input cost pressures. However, the market was encouraged by the company’s plan to strip US$100m of costs to optimise its operations in North America, while input cost pressures do appear to show some early signs of flattening.

• IOOF Limited (IFL) highlighted several operational challenges, such as revenue pressures as group margins trend lower and increased ongoing compliance and governance costs following the Royal Commission findings. There are still uncertainties around the provisioning required to redress ASIC reviews into quality of advice across the sector, however the company is comfortable it has provided for all known individual redress to this point.

• Brambles (BXB) reported softer US margins, which continue to come under pressure (now down around 450bp from peak). Better price realisation shows some progress in cost recovery and management talked to a disciplined market, however this was not enough to offset higher costs. The key cost impacting the business is transport, which is running at +9%.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

JCP is a research-driven, fundamental Australian Equities investment manager. With almost 20 years of organisational experience we have a proven performance record in both bull and bear markets.

12 stocks mentioned

JCP Investment Partners

JCP Investment Partners

JCP is a research-driven, fundamental Australian Equities investment manager. With almost 20 years of organisational experience we have a proven performance record in both bull and bear markets.

Expertise

JCP Investment Partners

JCP Investment Partners

JCP is a research-driven, fundamental Australian Equities investment manager. With almost 20 years of organisational experience we have a proven performance record in both bull and bear markets.

Expertise

Comments

Comments

Sign In or Join Free to comment