Pilbara Nuggets: Too early to Novo?

There is little more exciting in mining than a discovery. “Discovery” companies (as opposed to “exploration” companies) are rare, the phase characterised by investors speculating on how big a find could be, as inevitably the market has to digest each new drill hole as it is delivered. In this time there are generally far more investors wishing to purchase shares than wishing to sell – classic case of demand far outstripping supply.

You don’t need a supportive market to capture investor imagination for a discovery. Recent Australian examples such as Sandfire (re-rated 54x, May 2009 - Dec 2010) occurred in the market recovering from the GFC, Sirius (re-rated 87x, Jul 2012 - Mar 2013) on the other hand took place well after the market peaked. Even so, investors’ willingness to embrace upside does tell us a fair bit about risk appetite in the market, and the recent reaction to a find of gold nuggets in Australia speaks loud and clear to that.

Gold nuggets and racing pulses

Novo Resources is a Canadian listed company exploring for gold in Australia’s Pilbara region, currently capitalised at C$1.1B. What makes Novo quite enigmatic is this capitalisation has been achieved prior to any drilling taking place. A discovery re-rating, on modern standards at least, is accompanied by drilling results which adds fuel to the speculative fire with each fresh batch of numbers making the find bigger.

$1.1B buys a lot – for the same amount you would get all of Saracen Minerals. Add together Dacian, Beadell, West African and Ramelius and you’ve still got some change for a coffee (or a whole café) inside the market cap. That the market is valuing the company as highly as a medium sized local producer suggests the buyers have conviction of a substantial prize. It is unthinkable that this could have occurred in an un-supportive market, and a great snapshot of investors willingness to take on risk – a clear signal that the “wholesale speculator” is back, which is the type of attitude that helps raise money to explore and draws the cycle further into boom.

According to Macquarie, the market was valuing Australian listed gold companies at around A$70/Resource ounce during September 2017 – applying this metric to Novo, the market is pricing discovery of something like 16 million ounces. Pick your own more aggressive or modest metric – it will still be pricing a large number of ounces. Whilst Novo does not have any drilling results to speak of, there has been plenty of evidence presented to whet the appetite of punters – in the form of gold nuggets.

Novo is targeting gold hosted in a conglomerate horizon. Gold nuggets have been extracted from surface pits so the unit is without doubt mineralised to some extent, and Novo control a vast strike extent – perhaps some hundreds of kilometres. The geological analogue offered is the South African Witwatersrand – a conglomerate hosted accumulation of gold which has been the source of around one-quarter of all the gold ever mined. This analogy sets the scene for huge potential. So if, and it’s a big “IF”, the Pilbara conglomerate unit is reasonably mineralised, it’s a big prize.

Nearology

Nearology is the practice of attributing high value on the basis of proximity to something genuinely valuable. In the case of Novo, perhaps this is quasi-nearology, as we don’t yet know what they have. Nevertheless, Novo has sparked somewhat of a “modern era” gold rush, which plays out on the stock market involving listed exploration companies. The rush has seen explorers pegging ground in the region, others already holding ground have been awakened, and all of the neighbourhood re-broadcasting the conglomerate potential of the region. Investors have bought up shares in these companies, and prominent amongst these is Canadian listed miner Kirkland Lake who are a major shareholder of Novo and De Grey, having invested in excess of $60m in fundraisings undertaken by the pair. The presence of Kirkland no doubt provides reassurance for investors looking for some sort of technical tick of approval.

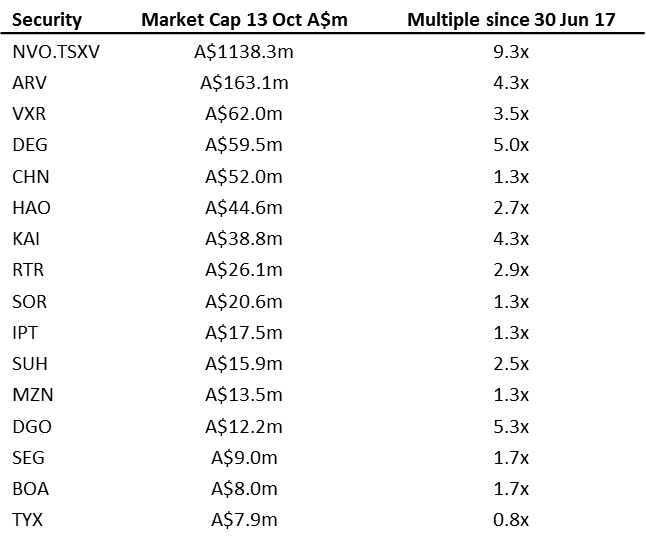

The nearology plays are listed below – not as a watchlist, merely to demonstrate the share price appreciations that have taken place since June 2017. Given these companies are all explorers, their starting capitalisations were all minimal – so something like A$1.5B of capitalisation has been created in a space of under 6 months!

What’s with the big “IF”?

Allow me to point out right from the start, I have no interest in Novo-knocking – the market anomaly it has created is of much greater interest.

Because there is so little sub-surface evidence yet, opinions are polarised between wildly optimistic and highly sceptical. Many Australian geologists have gravitated to the latter and whilst many Australian stockbroking analysts have circulated commentary on the “Pilbara gold rush”, they are notably cautious in tone and conspicuously omit a conviction call on the upside. No one can rule out a discovery being made, but equally, there is an obvious pride aspect for Australian geologists if a Canadian company makes a sizeable discovery under all our noses.

The big “IF” derives from the severe mismatch between the market capitalisation now at stake, and actual data supporting the potential – Novo is valued for a big discovery, but is cum all the work to prove that up. This is expensive work, and usually hit and miss. The prospectors’ adage toward gold goes something like “it is where it is”. No prospector ever said “it is where you think it is”. Until mineralisation is detected down dip of surface occurrences, it remains theoretical.

Whilst the prospective conglomerate unit host is substantial in size, it is unlikely to be uniformly mineralised. Rough expectations of what is down dip are often based on what exists at surface. Gold is quite commonly concentrated at surface by weathering, but if that were pushed to one side there might be sufficient reason to think that gold distribution along strike would mimic that down dip. Surface work is hardly “blanket coverage”, the highlights, however, are shallow pits, many developed by prospectors, containing patches of nuggets. Novo wowed the mining investment world with a live video demonstration for the audience at a recent gold mining conference, extracting nuggets in spectacular fashion from one such pit – this occurrence is certainly not expected to be characteristic of the “average”! Prospectors are generally tenacious and persistent. If they are onto a good nugget patch, they tend not to leave until it’s done. Given there has been no extensive extraction by prospecting, the conservative assumption is that gold is patchy, so the challenge will be in detecting similar patches beneath the surface.

Economics?

Don’t be silly – it’s far too early for this. So far the biggest “sensitivity” in the “valuation” for Novo is size. If ounces found down dip of surface are in any way analogous to the surface occurrences, then some scale of open pit workings don’t appear out of the question. However, to justify the price this needs to work at depth too. Underground mining of Witwatersrand conglomerates is labour intensive, and historically has benefited immensely from a locally available cheap labour force. Did I already say it’s far too early for this?

Before anyone considers mining, the biggest challenge will be reliably intersecting and sampling gold. Coarse gold is difficult to measure in any lithological setting, because of the concentration of metal into nuggets, which a drill sample either hits or misses. The intersection of a nugget produces an anomalously high sample grade, disproportionately higher than the grade of the area it came from. To obtain the best estimate of gold abundance, it is necessary to take large samples (which is what Novo is endeavouring to do).

Priced for perfection, but waiting to know

It’s too early to determine what sort of gold abundance exists in the conglomerate unit causing all the excitement. Geologically, this is an exciting play – the scale potential is huge given the extensive nature of the prospective host, and it’s hard not to be a little aroused (geologically speaking) by handfuls of gold nuggets. However, investors in Novo and neighbours are banking a great deal on potential right now.

How can investors justify paying what they are? Clearly, buyers are pricing a big find. The lack of drilling evidence yet from Novo and its neighbours is a cause for concern given the capitalisations they have achieved so far – this is the aspect which is most historically anomalous. Investors will often pay far more for something they don’t understand than what they do, especially as a market gathers collective greed. The conclusion that is immediately evident is that risk appetite has returned to mining, which is essential for the boom to progress. We have not seen conditions so supportive of highly speculative exploration concepts for many years.

The worrisome aspect now is how risk appetite would be affected if drilling evidence doesn’t deliver what the market expects to see.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

2 topics

4 stocks mentioned

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Comments

Comments

Sign In or Join Free to comment