Resource Sector Momentum Building

Gavin Wendt

MineLife

Commodity prices have defied pessimism and rallied solidly over recent months on the back of improved Chinese economic prospects, stability on the European political front, some degree of acclimatisation to Trump-related government volatility in the USA - and a weaker US dollar.

The rally in commodities also corresponds with the International Monetary Fund's (IMF) latest estimates for world economic growth – it sees the global economy expanding by 3.5% this year, despite a reduction in its US outlook.

With the exception of a slide in the prices for wheat and natural gas, virtually every major commodity has posted solid returns. The best-performers have been industrial metals and oil, along with some agricultural commodities like coffee and soybeans. However, most eyes have been focused on the rally in copper, which has coincided with stronger economic data emanating from China.

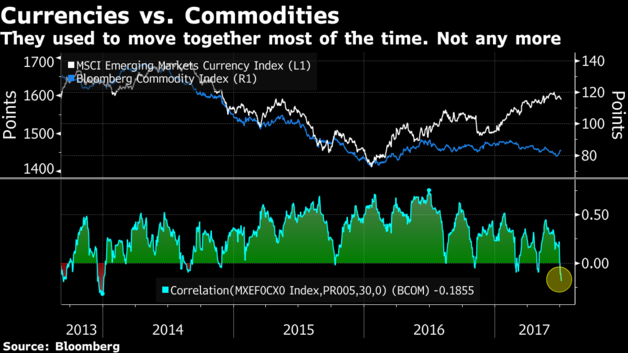

The evidence tells us that July marked the first month so far in 2017 that the Bloomberg Commodity Index (BCOM) (+2.3%) outperformed the S&P 500. Bloomberg analysis shows that the BCOM in fact is showing a similar recovery pattern as 2009, in the immediate aftermath of the GFC.

Higher commodity prices and a weaker dollar are important inflation indicators that have until this point been notably absent in the recovery so far. A peaking dollar should mark an inflection point for sustained commodity recovery, supported by demand exceeding supply and multiple years of price declines.

Iron Ore

Positive price movements (up a third since 30 June) will have a big impact on heavyweight miner earnings and treasury revenue forecasts. There doesn’t appear to be one single factor driving the recent gains – rather a combination of influences. This has seen the Platts Steel Index hit its highest level since early April and iron ore trade above $75/t.

Contributing factors include the Chinese steel industry’s purchasing manufacturers’ index (PMI) rising to its highest level since April 2016, renewed Chinese commitment to cut steel capacity, along with environmental inspections of domestic iron ore mines, plants and steel mills that are causing supply disruption.

Vale, the world’s biggest iron ore producer, believes prices will probably hold near present levels. It estimates that the break-even price for some Chinese marginal suppliers is around $US70/t. Goldman Sachs has also recently upgraded its 2017 forecast price from $US55/t to $US70/t.

Gold

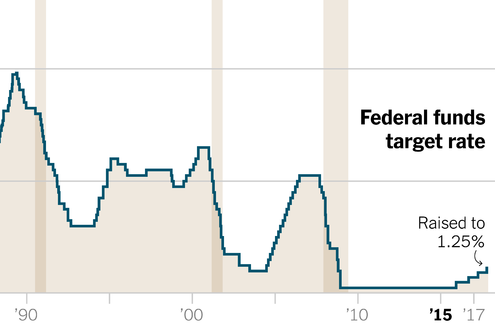

After trying to convince the markets all was well as it looked to adopt a more hawkish and aggressive economic stance over recent times, the US Federal Reserve has reverted back to its dovish persona. Rate rises are done for 2017, with tepid economic data spooking the Fed – although it won’t admit as much. As readers will know, I’ve had my doubts regarding the reliance of US growth for some time.

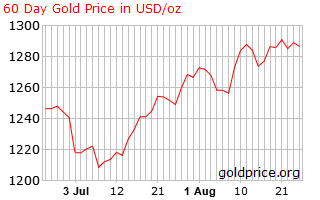

This recent economic data and the Fed’s dovish stance have combined with geopolitical uncertainty in Venezuela and North Korea, to reignite gold buyers. Given that US equities have continued to rise in value and continue to create a risk-on environment in financial markets, precious metals have not only held their value well - but have continued to appreciate.

With the potential for the current geopolitical hotspots in North Korea and Venezuela to deteriorate further, combined with a weak dollar and static interest rates, I strongly believe that the current rally in gold will continue.

Copper

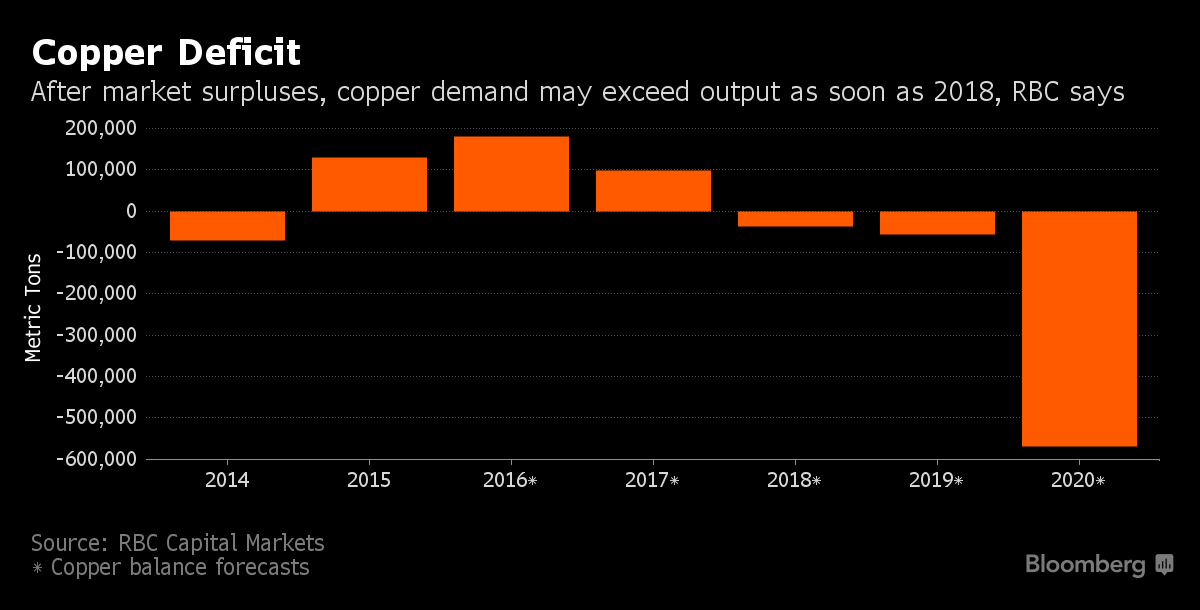

Copper bulls are optimistic – and so they should be - as China’s improving economic outlook and labour disputes at mines in Chile and Indonesia, continue to drive prices higher. The latest statistics show that copper futures are trading at their highest level in more than four months and prices at two-year highs.

The world’s biggest consumer reported faster-than-expected economic expansion during Q2 2017, signalling that the Chinese government’s full-year growth target could be met. This is significant, because demand optimism is growing just as another labour dispute is brewing in Chile, the world’s biggest copper supplier. In fact, supply disruptions have helped drive the copper market into deficit, with global stockpiles dropping during four out of the past five weeks.

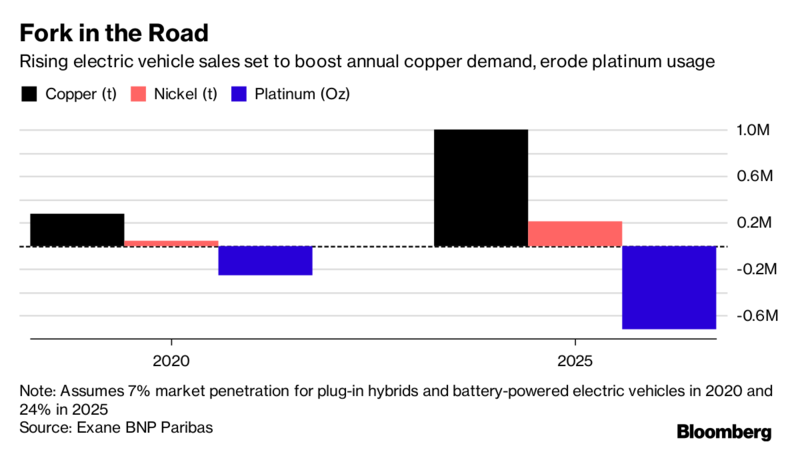

And let’s not forget the electric vehicle (EV) revolution – with electric cars set to contain about three times more copper than a regular vehicle.

Not surprisingly, this tightness is drawing the interest of hedge funds, which are the most optimistic on the metal since February – boosting their net long positions accordingly.

Summary

Commodity prices have defied pessimism and rallied solidly over recent weeks on the back of improved Chinese and international economic prospects, stability on the European political front, some degree of acclimatisation to Trump-related government volatility in the USA and a weaker US dollar. H2 2017 looks set to be a strong period for commodities right across the board.

We’ve also seen the positive impact on the A$, which has trended higher as many raw materials have recovered from their multi-year lows reached in early 2016. Logically, this positive price trend will flow through into resource equity prices via enhanced levels of investor interest.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

8 topics

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Gavin Wendt

Founding Director

MineLife

Gavin has been a senior resources analyst following the mining and energy sectors for the past 25 years, working with Intersuisse and Fat Prophets. He is also the Executive Director, Mining & Metals with Independent Investment Research (IIR).

Expertise

Comments

Comments

Sign In or Join Free to comment