Short and Sharp: 2020 – The year when nothing really changed (for markets…)

This year, the hits have come hard and fast, with the global pandemic wreaking economic devastation and seemingly changing life as we know it. Fear and anxiety have become a permanent companion to many of us as we try to navigate our daily lives under the threat of social restrictions and public health concerns. 2020 is the year we would all like to forget—and somehow, equity markets have already done just that.

It’s not just that global equity indices have regained their pre-pandemic highs, erasing all the market havoc inflicted by corona crisis. They are also just as grossly disconnected from the underlying economic fundamentals as they were at the start of 2020. Indeed, global economic activity is still running some 5-30% below its pre-pandemic level, resulting in an equity market that is once again running far ahead of economic realities.

S&P 500 Price Return Index

Index level, January 2017 – present

Source: Bloomberg, Principal Global Investors. Data as of September 30, 2020.

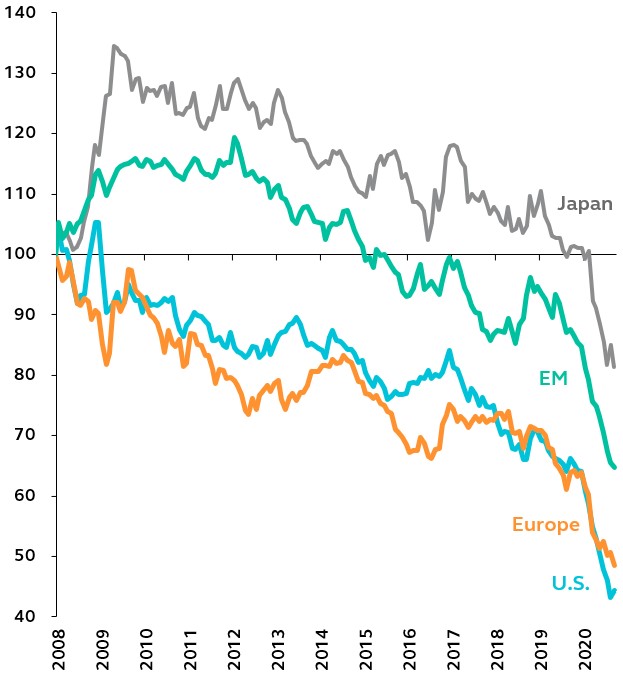

Valuations of most markets are once again extremely stretched, emboldened by ample central bank liquidity, and increasingly vulnerable to changing risk sentiment. Even the composition of the equity market performance this year looks familiar. Most of the S&P 500 gains have come from defensive sectors—particularly mega-cap technology stocks which had, incidentally, already been drastically outperforming the rest of the market for the last ten years. As a result, the dislocation between growth and value has continued to widen, In the U.S., the MSCI growth index has risen more than 25% this year, drastically outperforming the MSCI value index which has lost just over 10%.

MSCI Value/Growth Index Ratio

Annualised Returns Ratio, 2008 – present

Source: Bloomberg, FactSet, Principal Global Investors. Data as of September 30, 2020.

Indeed, just as it was in late 2019, fundamentals and valuations appear to be of limited relevance in this market. Technicals—that is, central bank liquidity—is still all that matters.

What lessons does this teach us for 2021?

Focus on the central banks. Don’t fight the Fed. Follow the money. Whichever is your preferred statement, the message is the same: central bank liquidity is likely to be the key determinant for capital markets next year. As long as the Federal Reserve and other central banks continue to inject liquidity into the financial system, financial conditions will remain extraordinarily loose, enabling risk markets to maintain positive gains.

However, the continued presence of the Fed does not assure economic recovery. Just as we have seen this year, monetary policy is hitting the walls of effectiveness and it is now the role of fiscal stimulus to encourage economic reflation. This suggests that the sustained disconnect between equity markets and economic fundamentals is likely to persist unless governments are willing to spend heavily. Bankruptcies and defaults may indeed rise as companies struggle with the prolonged effects of the pandemic—but this doesn’t need to mean capital markets are likely to suffer a significant correction.

Longer-term, the capital markets’ dependency on low interest rates is problematic. Once the economy is back to pre-pandemic levels, businesses are again thriving and inflationary pressures are building, governments will inevitably have to turn to the daunting task of reducing public debt, while central banks look to begin unwinding the extraordinary monetary policies. How markets will deal with the withdrawal of the liquidity that they have become accustomed to (and reliant on) will eventually be the key consideration for investors.

It seems that this year and next will mark part one of the pandemic narrative: actively addressing the recovery at hand, with central banks playing an invaluable role in upholding positive market performance. But part two of the story will involve dealing with the inevitable hangover of policy, debt levels and dependency on low rates. That’s when things will get a whole lot tougher.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

........

Unless otherwise noted, the information in this document has been derived from sources believed to be accurate as of October 2020. Information derived from sources other than Principal Global Investors or its affiliates is believed to be reliable; however, we do not independently verify or guarantee its accuracy or validity. This material contains general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, recommendation or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. The opinions and predictions expressed are subject to change without prior notice. Any reference to a specific investment or security does not constitute a recommendation to buy, sell, or hold such investment or security, nor an indication that Principal Global Investors or its affiliates has recommended a specific security for any client account.

Subject to any contrary provisions of applicable law, Principal Global Investors and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in this document or in the information or data provided in this document.

Past performance is no guarantee of future results and should not be relied upon to make an investment decision. Investing involves risk, including possible loss of principal.

Links contained in some blog posts may take you to third-party sites and Principal Global Investors makes no guarantees to the accuracy of the information provided. Principal Global Investors does not endorse, authorize, or sponsor any third-party content.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts or returns. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the viewer.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

Insurance products and plan administrative services provided through Principal Life Insurance Co. Principal Funds, Inc. is distributed by Principal Funds Distributor, Inc. Securities offered through Principal Securities, Inc., 800-547-7754, Member SIPC and/or independent broker/dealers. Principal Life, Principal Funds Distributor, Inc. and Principal Securities are members of the Principal Financial Group®, Des Moines, IA 50392.

1387800