The bear versus bull case for investing in banks

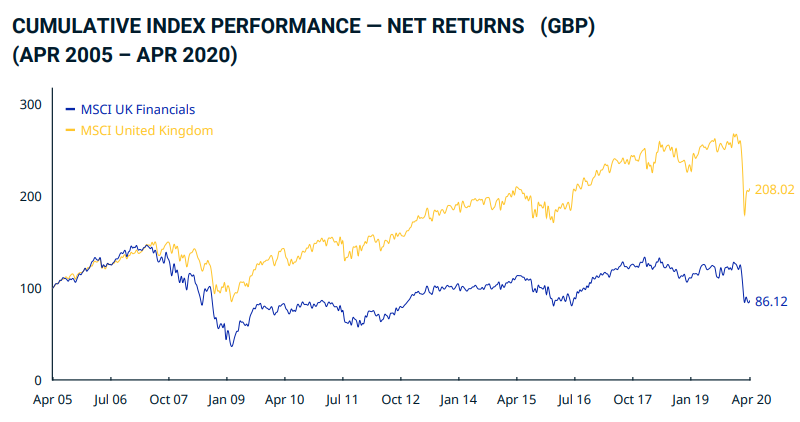

They say a picture tells a thousand words and the story for UK financial sector investors could not be more depressing going by the below chart. A theoretical $100 investment made in April 2005 in UK financials, as represented by the MSCI UK Financials Index, would be worth only $86 after 15 years.

SOURCE: MSCI (ASSUMES DIVIDENDS REINVESTED)

In the 2010s the UK economy and in turn, the transmitters of credit experienced major headwinds:

- Slow growth as a result of austerity since the GFC

- Eurozone dysfunctionality

- Record low/zero rates

- Vaporisation of profits from mis-selling and misconduct, and of course

- Brexit.

Enter 2020 and UK banks have had to scrap dividends due to COVID-19 and UK financials are languishing again. Intercontinental politics aside, many of those same elements now appear to be present in the Australian economy. The RBA slashed rates to 0.25% and introduced QE. Westpac and ANZ have deferred dividends while NAB made a significant reduction in their recent results.

Bank stocks and financials make up the largest component of the S&P/ASX 200 Index at 26% and are hugely important to investors, retirees, nonprofits and SMSFs who rely on dividend income to fund expenses. But does the UK experience portend what's to come for this all-important sector? Or are the Big Four Aussie banks built to be better?

To shed light on this topic, we've asked two of our contributors with strong views on the banks to produce bull versus bear reports, exclusively for Livewire readers. They provide an in-depth thesis for or against the sector, discuss portfolio positioning and how to navigate generating income.

- The bull case is written by Romano Sala Tenna from Katana Asset Management (out Monday, 18 May) in his piece titled "Bank on a 70% return: Why 'tis the season to be bullish on the Big Four".

"We need to remind ourselves that in a post-covid world, our country will have the lowest interest rates on record. The hunt for yield will be on in earnest. We, therefore, see no reason why the banks cannot regain their February 21 pricing over the next 18-24 months. This offers substantial capital growth from the current levels." - Romano Sala Tenna

- The bear case is written by Damien Klassen from Nucleus Wealth (out Tuesday, 19 May) in his wire titled "Banks perform badly with a flat yield curve or a debt crisis, Australia faces both".

"These are not company-specific issues, rather the banks are facing incredibly challenging macro-economic conditions on two fronts. The first front is the risk of a debt crisis coming either through business lending or a housing market crash. Even if banks somehow manage to avoid the effects of a debt crisis, they are facing a second front of an extended period of low interest rates.

Neither are attractive for banks. The acute crash of a debt crisis, or the chronic grind lower of low interest rates." - Damien Klassen

FOLLOW the managers to get their reports first

If you want to be the first to read their reports, click on each of the managers you want to hear from, and then click FOLLOW on their profiles. This way you will receive the report directly by email soon after it goes live. I hope you find them useful.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

2 topics

4 stocks mentioned

3 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment