TOL - 9th Dec, 2020

The global recovery will be its darkest before dawn

As 2020 nears an end, investors face a challenging combination of crosscurrents. On the positive side, the US election has passed with a market-friendly outcome and three COVID-19 vaccines appear to be within weeks of initial distribution, with more likely to follow. Typically, these events would be the all-clear signal investors need to shift out of defensive work-from-home beneficiaries into cyclical recovery plays.

However, major developed countries across the Northern Hemisphere are facing new record levels of COVID-19 infections, spurring new economic lockdowns and increasing the risk that many companies, particularly small businesses, might not make it to the other side of this pandemic. Investors face a timing conundrum, indicating yet again that it is likely to be darkest before the dawn.

Against this backdrop we believe it is fair to say that the global outlook for 2021 is mixed. As we reach the beginning of the end the pandemic, the process will be long and complex, considering:

- The COVID-19 vaccine distribution may further aggravate disparities between and within nations.

- The consequences of the lack of fiscal follow-through to support economic activity in the United States are likely to accumulate, dampening the pace of the recovery.

- Fortunately, European governments have enacted significant fiscal stimulus packages and are poised to benefit from the European Union recovery fund as it begins disbursing funds in 2021.

- China, by contrast, has rebounded rapidly from the pandemic and is on track to deliver growth in 2021 at levels not seen in years on the back of significant monetary and fiscal stimulus.

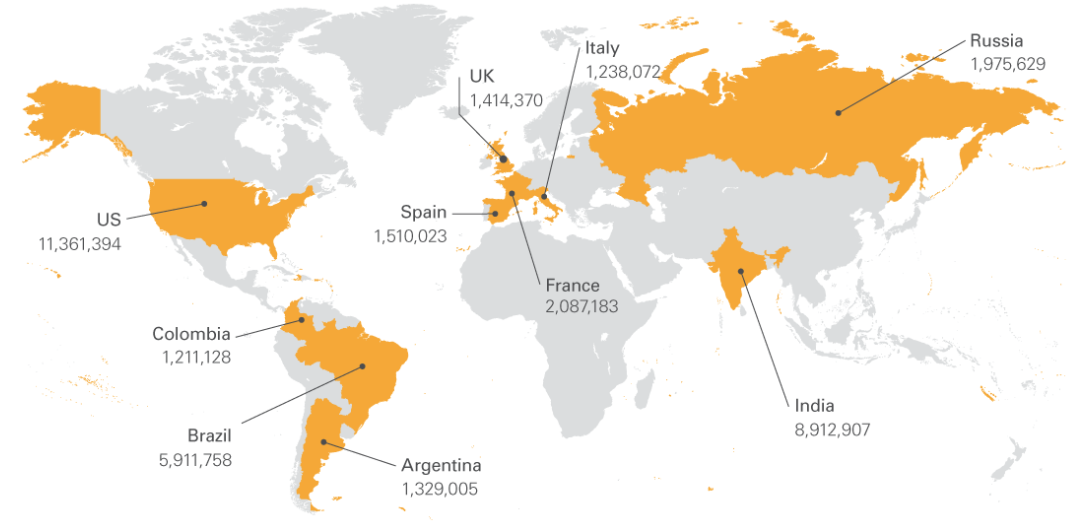

Exhibit 1: COVID-19 Infections Continue to Surge across the Globe

As of 18 November 2020

Source: John Hopkins University COVID-19 Tracker

Through these countervailing forces, and with equities appearing expensive by historical standards, finding attractive sources of income and diversification is challenging. Global central banks hoping to invigorate growth and increase inflation expectations continue to prop up the value of financial assets, but we appear to be approaching a point at which central banks can no longer drive the economy. If that is the case, security selection will be more important than ever as we wait for a paradigm shift to economic growth that gives rise to the next investing regime.

The COVID-19 Vaccine Could Result in Major Economic Divergence

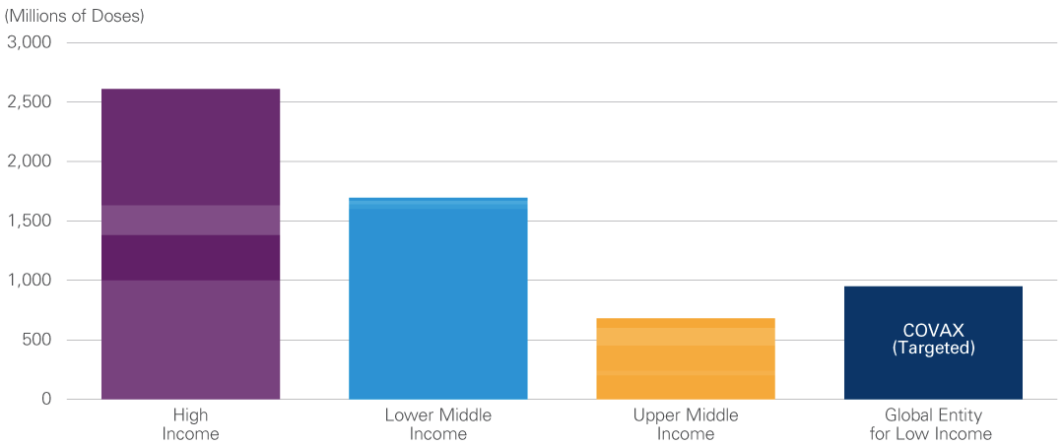

Higher income economies have already contracted 2.6 billion doses (Exhibit 2) of the vaccine, and some emerging markets countries, including Brazil, Argentina, Indonesia, and India, have negotiated contracts for about 1.7 billion doses directly from manufacturers. Lower income countries, however, have been unable to make direct deals with manufacturers. Instead, these countries will be relying on COVAX, a facility led by the Global Alliance for Vaccines and Immunisations (GAVI), and organisations like the Bill and Melinda Gates Foundation to partner with vaccine manufacturers to provide doses on a non-profit basis. Current estimates suggest, however, it will take until 2024 to produce enough doses for the whole world. The AstraZeneca/University of Oxford vaccine will be critical in ensuring emerging markets have access to the vaccine, as they have agreed to sell doses to developing countries at cost in perpetuity. AstraZeneca has agreed to supply India with 1 billion doses and GAVI/COVAX with 300 million—nowhere near enough to cover the developing world but an important start.

Exhibit 2: Wealthier Countries Will Have More Access to Vaccines

As of 11 November 2020

High Income regions represent: UK, US, Japan, and the EU.

Source: Launch and Scale Speedometer COVID-19

Even once a country does gain access to doses, logistics and delivery problems could create severe bottlenecks that will widen inequality and create long-lasting damage to economies. The Pfizer vaccine requires a -70° centigrade (-68.4° Fahrenheit) temperature while being transported. Pfizer has developed a proprietary shipping container that can carry 5,000 doses, be recharged with dry ice, and reused. The Moderna vaccine requires a temperature of -20°C, which is more comparable to a typical household freezer. AstraZeneca’s vaccine, meanwhile, can be stored at -3°C, which could be vital to the success of distribution in many rural parts of the world. The logistical challenges involved in getting this vaccine to small towns in the United States and Europe and into developing countries are severe. In the early phases of deployment, the US military will play a central role in managing logistics alongside private sector partners. The vaccine producers have indicated that in many countries, they will sell the vaccines directly to governments who will then manage deployment and allocation to recipients.

Therefore, it is difficult to predict the path of the COVID-19 recession and whether a pandemic recovery necessarily leads to an economic recovery. Beyond the challenges of transportation logistics, administering the vaccine will require key political decisions in every country. The first decision will be which populations get access to the vaccine first.

Although the devastation from COVID-19 has been felt nearly everywhere, its effects are likely to persist much longer for emerging markets waiting at the back of the queue for vaccines. Moreover, many emerging markets do not have the same capacity as their developed peers for expansionary fiscal policy. The starting point for an economic recovery in emerging economies will be lower as a result. An economic and pandemic divergence is conceivable—one in which developed countries can vaccinate citizens and recover, while the virus continues to rampage across developing countries. The World Bank projects that as many as 150 million people in developing countries will be pushed down into the "extreme poor” category by the end of 2021.1

The creation of new vaccine techniques could herald a new dawn in vaccine technology which could mean humanity is less at risk from pandemics in the future. And yet, the politics of vaccine distribution may be the most challenging part of the process. How, when, and who gets access to the vaccine may exacerbate the inequalities that have marked the last few decades, create new forms of bio-inequality, and result in long-lasting imbalances. Policy makers can ensure the vaccine is distributed equitably, but if they fail, citizens may not forget.

United States: New Leadership in a Polarised Nation

While Democrats celebrated making Donald Trump a one-term president, Republicans rightly cheered chipping away at the Democrats’ majority in the House of Representatives, while likely holding on to control of the Senate, albeit narrowly. At best, the Democrats can hope for 50 Senate seats, if they take both of the ones up for grabs in the Georgia run-offs in early January, which would allow Vice President-Elect Kamala Harris to break ties.

Although the election drew a record of nearly 157 million voters, the results showed a country that rejected Donald Trump, but did not reject his party. For the incoming administration of President-Elect Joseph Biden, this poses a serious challenge, as the most visionary plans are unlikely to gain traction, with a weakened House majority and a Senate that, at best, can still block legislation through filibusters. The likely outcome is some degree of gridlock. Biden’s key decision is whether to try to convince centrist Republican senators to break ranks and agree to measured legislation or to take a more aggressive position of painting the Republicans as obstructionist and ideologically rigid to the detriment of American voters, effectively kicking off the 2022 campaign right out of the gate. This decision will not be an easy one given the toxic backdrop of US politics

Ultimately, the Biden Administration’s success or failure will likely be determined by three things: COVID-19, climate change, and China.

- Centring on COVID-19 — another fiscal package, if one is not passed during the remainder of President Trump’s term, test and trace initiatives, and vaccine distribution and logistics management. Case counts are rising in virtually every state, as the United States is regularly recording nearly 200,000 cases per day (Exhibit 3). The recovery from COVID-19 will involve multiple policy levers—immediate fiscal relief will need to be complemented with longer-term investment to strengthen the rebound after the pandemic and address challenges that existed well before the virus, in particular, income and racial disparities. Although Biden supports another expansive relief bill like the $2.2 trillion CARES Act passed in March 2020, hopes for this have faded in the lame-duck session. Employment for low income workers has already been hit hard, and the damage to the economy over the next two months could be deep as the virus continues to rampage across the country (Exhibit 4). While Biden is likely to be able to marshal bipartisan support for another stimulus, the delay until he takes office and can get a fiscal package enacted could cost many in the country dearly. Meanwhile, with three vaccines to be approved before the new year, delivering the vaccines across the country and around the world will present myriad challenges..

Exhibit 3: COVID-19 Cases Are Rising in Nearly Every State

As of 12 November 2020

Source: The Covid Tracking Project, 14-day average of new cases. 5 November 2020. States with populations over 2m

Exhibit 4: Employment for Low Income Workers Is Down 20% This Year

As of 22 October 2020

Source: tracktherecovery.org

- On climate, the likelihood of Republican support is far more limited. Instead, the Biden Administration has already indicated it will rejoin the Paris Accord through executive order and overturn the vast majority of the 100 climate-related orders that the Trump Administration reversed. Biden has consistently underscored the importance of climate to his economic plans and an infrastructure package could contain climate-friendly proposals such as greening and weatherising existing buildings and ensuring new builds are energy efficient. Passing anything resembling the $2 trillion climate package that Biden campaigned on will be extremely difficult, however, due to Republicans’ overall reluctance to tackle climate change. To make serious progress, the Biden Administration will need to be creative in how it engages with stakeholders and coordinate with states to advance its climate agenda.

- Finally, on foreign policy, Biden will have a chance to reset several key relationships. On China, US policy is unlikely to change meaningfully, though the approach will. Biden is known to be a China hawk on both economic and humanitarian grounds. A key early decision he will face is what to do about billions of dollars in tariffs on Chinese producers. Rather than eliminate them wholesale, Biden’s team is likely to use them as leverage to accomplish other negotiated policy objectives. Additionally, Biden has already expressed his disapproval of the treatment of Uighurs in Xianjing. One thing a Biden Administration is likely to be able to provide China, and investors broadly, is greater stability and predictability in decision making. However, those expecting a more dovish approach to China may be in for a rude awakening.

Two other major foreign policy questions involve Iran and the European Union (EU). The Trump Administration exited the Joint Comprehensive Plan of Action (JCPOA), which was the Obama Administration’s agreement with Iran to limit Iran’s ability to accumulate fissile nuclear material. Biden has already pledged to re-engage diplomatically with Iran, but that will take time, not only because Iran has been building up enriched uranium after the Trump Administration exited the agreement, but also because of Iran’s mid-2021 presidential elections. However, if negotiations succeed and sanctions are lifted once again, a result could be up to 2 million barrels of oil per day returning to global supply.

The EU, meanwhile, was subject to harsh treatment, including tariffs, during the past four years. Biden’s engagement with Europe is likely to be much more straightforward and resolving trade disputes with Europe will likely be a high priority. Rejoining the Paris Accord will be the first step for the United States to return to multilateralism and rebuild credibility abroad. Just as for China, predictability should be one of the biggest upsides of a Biden presidency: Decisions will take place through traditional channels and are unlikely to be announced on Twitter.

Other policy priorities are likely to target the growing wealth and income gap in the United States. Raising taxes appears to be virtually impossible because of resistance from Republicans in the Senate, meaning any government spending will likely come from further borrowing. Healthcare reform, ever the priority for Democrats, may have a complicated path forward. While the Affordable Care Act looks set to survive yet another Supreme Court challenge, neither expanding healthcare via a public option nor lowering the Medicare age limit from 65 to 60 is likely to win Senate approval. Other executive actions that are being discussed include canceling some fraction of student debt and limited immigration reform, including a potential path to citizenship for Deferred Action for Childhood Arrivals (DACA) recipients.

US Outlook: Positives and Negatives

Positives

- Vaccine approval and rollout will likely accelerate an economic recovery

- Continuing expansionary fiscal policy is likely, though it may be smaller than Democrats hope

- Extremely accommodative monetary policy will last for several years

Negatives

- Potential policy gridlock from a divided government

- Lack of meaningful additional monetary policy tools could limit effectiveness

Europe

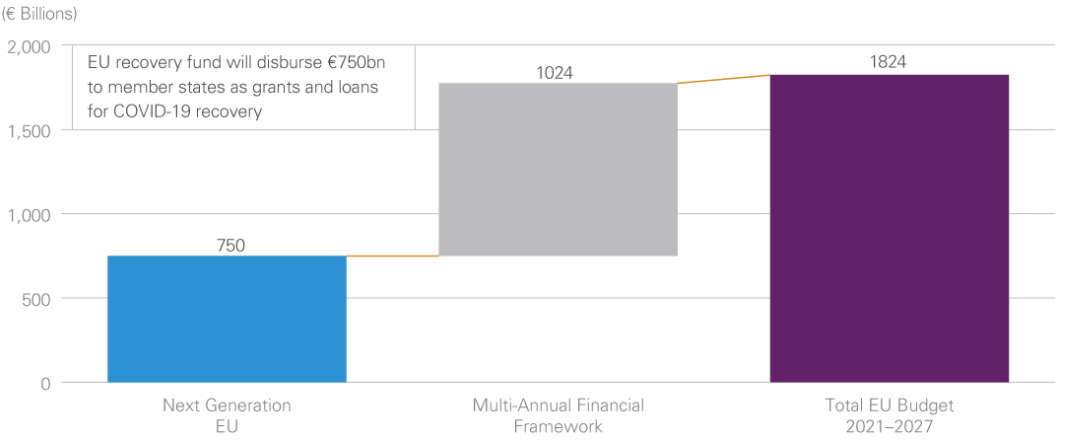

Europe continues to struggle with record numbers of infections across the continent that have led to new restrictions on economic activity. The EU recovery fund, worth €750 billion, will disburse most of its funds in the second half of 2021. The fund is a major agreement, as it enables Brussels to borrow from financial markets by issuing bonds with maturities through 2058 on behalf of the EU and then disburse funding to member states. Half of the funds will be distributed as grants and the other half, the Recovery and Resilience Facility, will be allocated based on member states’ national recovery plans (Exhibit 5). The EU has underscored that the facility will be used to achieve an economic recovery consistent with its climate change objectives. Grants and loans will be prioritised for green industries and investments, as Europe seeks to pivot its economy to more sustainable production processes.

Exhibit 5: The EU Recovery Fund Could Mark an Important Milestone

The fund could herald a major recovery in the EU, but key questions remain. The first is political: Can the EU maintain unity in one of its largest and most complicated undertakings? With any one nation able to wield veto power over an agreement, keeping members in line is a huge organisational challenge. Hungry and Poland have already indicated that they may be willing to veto an agreement if funding schemes are linked to a rule-of-law mechanism. Both the Budapest and Warsaw governments believe such measures are biased against them.

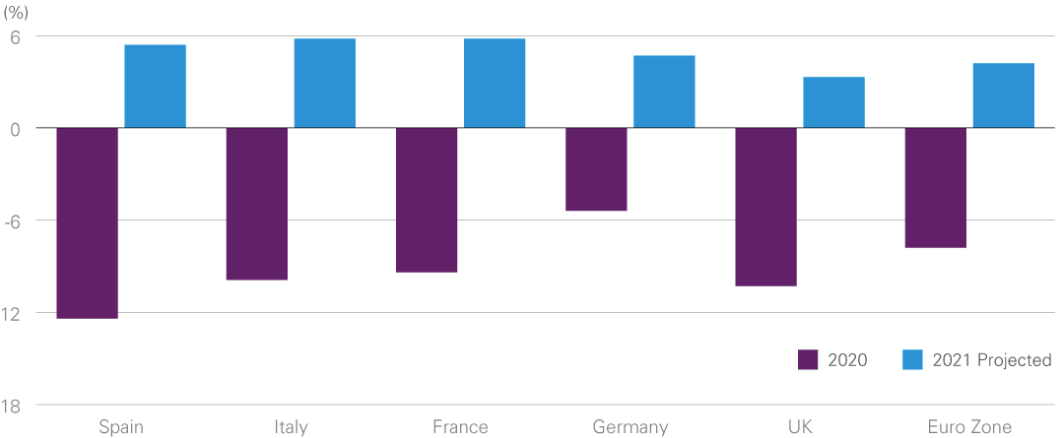

A second challenge is that funds do not actually begin flowing until the second half of 2021. Until then, member states, who are already mired in recessions will have to fend for themselves (Exhibit 6). As cases surge across the continent, whatever economic recoveries had been occurring over summer appear long gone. The European Central Bank’s (ECB) chief economist, Philip Lane, recently highlighted how some euro zone countries will be especially vulnerable, particularly those that rely on tourism and the service sector. Spain, for example is projecting an economic contraction of 12.6% this year.

Exhibit 6: European Economies Are Not Expected to Recover until the Second Half of 2021

As of October 2020

Note: UK forecasts do not assume a "no deal” Brexit—such an event would likely result in lower growth for 2021 than projected here.

Source: European Commission, Statista 2020

Complicating these questions will be federal elections in Germany and the retirement of Chancellor Angela Merkel, who has been the longest serving head of state in Europe. Her successor will be determined at leadership elections at the Christian Democratic Union party’s convention in January.

Finally, the ever-constant Brexit confusion continues as mixed messaging and personnel changes at 10 Downing Street create a lack of clarity over what the future of the United Kingdom’s relationship with the EU will look like. Even if major fault lines can be resolved—most importantly Northern Ireland—it appears as though the incoming Biden Administration will not be prioritising a US-UK trade agreement. The United Kingdom itself is currently in the middle of a second national lockdown and is likely to emerge from that weaker geopolitically and more fragile domestically.

Europe Outlook: Positives and Negatives

Positives

- Major fiscal stimulus could greatly assist the economic recovery

- Stimulus targeting green investments could be critical in diminishing carbon emissions and catapult Europe into the lead on green technology

Negatives

- Political fragility, from Brexit to Hungary and Poland, could hamper recovery efforts

- A change in German leadership could bring uncertainty to the union

China

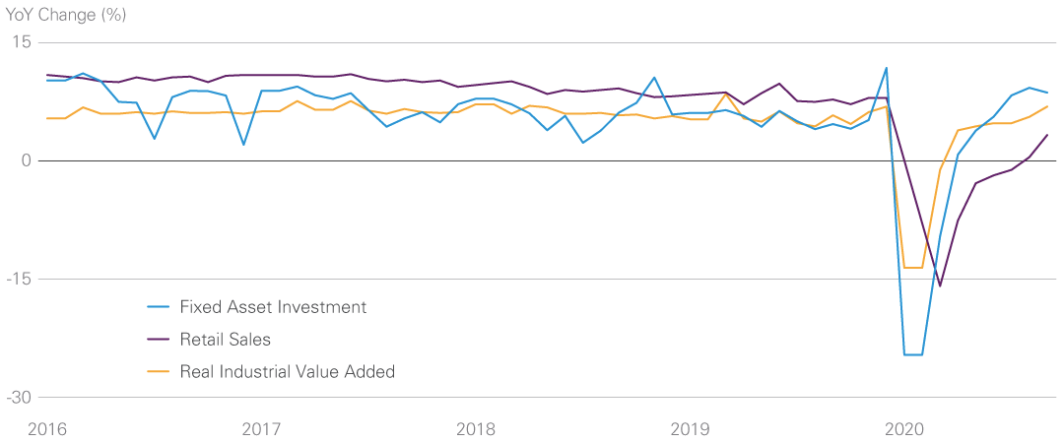

Though China was hit first and hardest by COVID-19, the Chinese economy has recovered rapidly, and the World Bank expects it to grow by 2% in 2020 and 7.9% in 2021. Factory output rose faster than expected in October 2020, and strong end-of-year growth is predicted.

Chinese efforts to re-centre the economy on a consumer-led model are expected to continue (Exhibit 7), but COVID-19 complicated these efforts by producing both domestic and foreign downturns. Unemployment appears to have already peaked and returned to pre-pandemic levels, and industrial production has also resumed (Exhibit 8). The service sector might soon follow since China has, at least officially, crushed its COVID-19 curve.

Exhibit 7: China Continues to Transition from an Industry- to a Service-Based Economy

Exhibit 8: Industrial Activity Rebounded Faster than Services in China

As of June 2020

Source: China National Bureau of Statistics, Haver Analytics

As of September 2020

Fixed asset investment data are monthly values calculated based on year-to-date series. January and February data are interpolated.

Source: National Bureau of Statistics Haver Analytics

Services in China

President Xi recently signed the Regional Comprehensive Economic Partnership (RCEP), a pan-Asian trade pact that gives China increased economic leverage and confirms its role as the preeminent economic power in the region. The agreement includes tariff reductions and regional supply chain facilitation, both of which could create major boosts to participating economies. The RCEP is the first trade agreement between Japan, South Korea, and China, and 12 other Asian and Oceanic countries and represents 30% of global GDP, making it the largest trading block in the world–a key achievement of President Xi’s tenure.

At the policy level, the Fourteenth Five-Year Plan (2021–2025) is currently being drafted after the Communist Party of China held its Fifth Plenary Session in October. No major surprises are expected from the full plan, which will be published in March; key themes emphasised during the plenary process were:

- Shifting emphasis from "high-speed” growth to "high-quality” growth

- Rebalancing the sources of economic growth with supply-side reforms

- Expanding domestic demand and enhancing foreign exports

- Greening production processes

Economic development remains the priority for the Chinese government. However, a shift to high-quality growth and green production reflects increasing concern with pollution and climate change. It is therefore expected that, unlike prior five-year plans, 2021–2025 will not have a numerical GDP growth target. The emphasis on the domestic economy is continuing evidence that a "dual circulation policy,” introduced by President Xi in May to increase both exports and domestic consumption simultaneously, is likely the future of China’s economy.

At the geopolitical level, how China adapts to the Biden Administration will be the biggest question. China is increasingly hardening its rhetoric on Taiwan and has effectively ended Hong Kong’s status as a separate entity from China. The "greater predictability” from the Biden Administration could well come in the form of continued objections to these actions. Chinese geopolitical ambitions in the South China Sea will continue to be major points of tension, as will ongoing support for North Korea’s Kim Jong-un. Domestically, the internment camps detaining Uighurs in Xianjing have been drawing greater attention and scrutiny, but whether the Biden Administration can do anything about any or all of these issues remains to be seen. An upside to President Trump’s actions in China is that they may have given Biden space to be more confrontational on some matters, even as there is greater cooperation with China on others, particularly climate change.

While China continues to wield greater influence in the global economy via trade agreements and its Belt and Road Initiative, tensions around several themes will doubtless rise. As we progress into what some political scientists’ term "the Chinese century,” agreements such as the RCEP underscore Beijing’s growing influence and the re-orientation taking place in the global economy.

China Outlook Positives and Negatives

Positives

- A strong economic recovery could help keep the global economy afloat

- A greater emphasis on quality of growth could reduce pollution and health problems

Negatives

- Ongoing dependence on credit raises risks of excessive leverage

- The country’s human rights record will draw greater criticism and pressure

Investment Implications

The next six months are likely to represent a choppy transition to the post-pandemic investing environment later in 2021. We would urge investors to remain focused on the long term rather than trying to time the ups and downs of short-term market gyrations.

Monetary policy may continue to be a focal point for investors, but central banks have few tools left at their disposal. We believe much of the developed market sovereign debt universe is unattractive; we would either rely on an actively managed global fixed income strategy that can tactically allocate to attractive opportunities.

We have seen in the past that extended periods of extraordinarily low interest rates can lead equities to appreciate as investors choose the "lesser evil” in their asset allocations. We expect 2021 to be no different. Our base case is that equity valuations continue to climb. The conundrum we face within the equity market is the tension between the cyclical impetus to invest in stocks that tend to outperform as their returns on capital improve after economic downturns versus the structural benefits from persistent ultra-low interest rates for quality and growth stocks. The stocks that are likely to benefit from cyclical improvement are not limited to those traditionally viewed as being value stocks.

There are many companies across a range of subsectors that have traded materially lower as investors seem to have concluded that the decrease in demand and the subsequent decline in returns on capital caused by the pandemic are permanent rather than temporary. In some cases, we disagree and would argue that the arrival of vaccines should lift those shares higher. On the flip side of the story, the market has also priced other stocks that have benefited from the pandemic as if the gains are permanent and returns will remain elevated for years to come. In some cases, we believe this optimism is well placed as structural trends were accelerated and pulled forward. In others, however, it is not, and we expect meaningful downside moves in some shares as the pandemic winds down.

While the jury is out on factor allocation decisions, considerations around the level and trajectory of financial productivity relative to the valuation of shares are critical from a security selection basis. In this case, we would caution against chasing companies that depend on cash flows far in the future as they are susceptible not only to the risk of failing to deliver on their business plans, but also to seeing their valuations compressed severely if interest rate trends change and discount rates increase vis-a-vis future cash flows.

Quality stocks, on the other hand, have a long history of outperforming markets through the cycle, albeit with short punctuated periods of relative weakness. We would focus on capitalising on near-term anomalies to position in these quality companies, complemented by companies that can improve returns to pre-pandemic levels as we exit this crisis.

Summary

This year has left an indelible mark on many families that have lost loved ones, jobs, and so much more. The pandemic has exposed fragilities that had been overlooked for decades and that will now need to be addressed. At the same time, we saw that governments can respond to a crisis with both fiscal and monetary policy tools that can be very effective. The key, in our view, is sustaining the use of those tools long enough to exit the crisis, rather than misinterpreting the success of the policies to mean the stimulus is no longer needed. In the United States, we expect significant policy changes from President-Elect Biden, but also expect legislative gridlock. The EU recovery fund and stimulus programs in China should help lift growth locally, but the United States will have to wait for a cyclical recovery after the pandemic. We expect central banks will continue to try to stimulate growth, though they have few remaining tools.

Investors will still face difficult decisions regarding sources of income, diversification, and capital appreciation. We would encourage focusing on bottom-up fundamentals for each individual security, while also avoiding the instinct to move too far out on the risk curve. The past year has been tumultuous, but there is a light over the horizon. Moreover, as a result of the pandemic, the power of scientific innovation has been demonstrated and should give us optimism as we seek to address other big challenges such as chronic health issues and climate change.

Learn more

For further insights from Lazard Asset Management's global group of experts, please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with Lazard’s Geopolitical Advisory group to assess economic and market implications of key geopolitical issues globally. Ron also advises clients of Lazard’s Asset Management businesses regarding macroeconomic and market considerations that are important to achieving their objectives. Previously, Ron was the Head of US Equity and Co-Head of Multi-Asset Investing for Lazard Asset Management. In this role, Ron was responsible for overseeing the firm's US equity strategies, Multi-Asset investing, as well as several global equity strategies. He was also a Portfolio Manager/Analyst on various US and global equity teams.

.png)

4 topics

.png)

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with...

Expertise

Ronald Temple is the Chief Market Strategist for Lazard’s Financial Advisory and Asset Management businesses. In this role, Ron provides macroeconomic and market perspectives to Lazard’s investment teams on a firmwide basis and works closely with...

Expertise

Comments

Comments

Sign In or Join Free to comment