Political populism and the markets

Populism hit the headlines a year ago when the UK voted to leave the European Union (EU), and it has cast a shadow over many political events since then. My colleague, political economist Talha Khan, discusses what could be in store for Europe, considers the effects on the US with the Trump administration, and examines what this means for investors in this investment insight.

The Brexit referendum result has sparked fears of a political domino effect in the rest of the EU. Populist parties in France, the Netherlands, Italy, Sweden, Austria and Denmark have expressed support for referendums on EU membership. Even in countries without many elected populist representatives, populist parties can exert a great deal of pressure on mainstream parties and the policy agenda, as is illustrated by the UK Independence Party’s role in catalysing the UK’s exit from the EU.

If the UK can show that its economy can thrive outside of the EU, it may provide a further boost to populist forces in Europe and could stall or even reverse European integration. The 2016 US presidential election saw an outsider, Donald Trump, becoming leader of the largest Western democracy, thus potentially propelling other populists in Europe. That said, recent events may also have had the opposite effect, demonstrating the danger of ‘protest votes’, as well as of complacency. For example, according to YouGov on the recently held UK General Election, 57% of 18-19 year olds and 59% of 20-24 year olds voted, compared with just 43% in the 2015 General Election. Many populist parties have fared worse than expected in recent elections over the past couple of months, including in France, the Netherlands and in Austria. The pro-EU momentum generated by Emmanuel Macron’s victory in France, in particular, has provided welcome relief for mainstream parties looking to push back against populist forces.

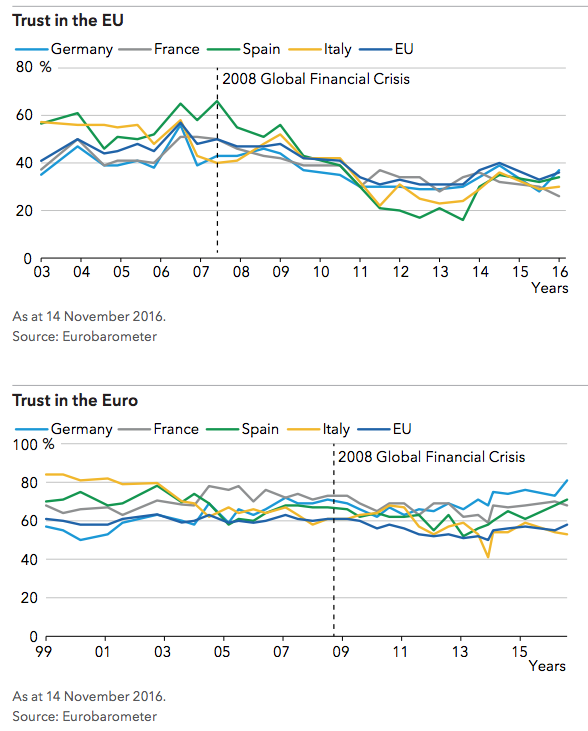

The factors leading to the rise of populism within Europe – including high unemployment and immigration – remain and support for the EU has been in decline since the global financial crisis in 2008. However, support for the euro area remains relatively stable. Moreover, trust in national governments lags that of the EU, which shows that while the Europeans are generally discontent with the direction of the EU, they don’t necessarily want to abandon ship (just yet). They want to effect change in the direction of the EU project both in the economic and political domains, and are willing to entertain a protest vote to achieve that. But according to surveys, the majority would still prefer to live in the EU (and in the euro area for those that are in it) than outside. It is important to note that while it is extremely hard to forecast catalysts for the disintegration of monetary unions, the breakdown is usually instigated when the core countries decide to leave; as such, in the case of the EU project, Germany, France and Italy remain the most important countries to monitor.

Still little clarity in the US

Since President Trump’s election victory, the investor community has been trying to figure out which parts of his agenda will be implemented and what that might mean for growth and the economy in general. Infrastructure spending, a reduction in regulation and tax reform could be positive, but trade and immigration restrictions combined with policy uncertainty can hurt growth. So far there has been little clarity on any of these fronts. The overall increase in infrastructure expenditure looks fairly modest in Trump’s 2018 fiscal year budget, which doesn’t actually propose any specific tax cut. Meanwhile, Trump has issued several executive orders to investigate or implement lighter enforcement of existing regulation, but so far new laws have not been proposed to reduce regulation. As for proposed immigration restrictions, these have come up against legal constraints, while the trade agenda has yet to move forward. One thing that this highlights is that once in power, populist politicians face practical difficulties of implementing their agendas and are generally forced to compromise.

Economic and cultural insecurities have driven the rise of populism

The current populist movement has its roots in economic and cultural insecurity. Since the global financial crisis, unemployment has been sticky in Europe, while wages have remained stagnant in the US. The working classes have felt their jobs threatened by globalisation and technology and their cultural identity threatened by immigration. Migration and terrorism have conflated in Europe to add to this resentment. Meanwhile, they see the governments of Europe as being made up of self-serving elites who oversaw the financial crisis and then bailed out those responsible for it, inflicting fiscal austerity and further misery on society instead.

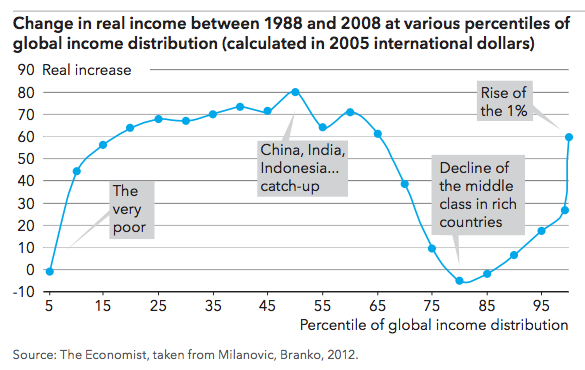

The chart below, produced by former World Bank economist Branko Milanovic, shows the change in real global incomes between 1988 and 2008. On the horizontal axis, people globally are ranked from poorest to richest while the vertical axis shows the percentage increase in real income over this period. It has been dubbed “the elephant graph” as the line has been compared in shape to an elephant, with the trunk pointed up on the right.

The chart shows that the very richest have gained a lot, and there has also been a significant increase in the incomes of the growing middle classes in emerging economies such as China, India and Brazil. It also identifies a group in the middle – largely made up of the low and middle classes of mature economies such as countries from Europe and the US – in which incomes have stagnated. Those at the very bottom of the global distribution have done poorly as well.

Along those lines, McKinsey Global Institute released a study on income inequality last year.1 The report found that from 2005 to 2014, household incomes across advanced economies (including the US and Western Europe) stagnated or fell for most income segments. It was a sharp contrast from the previous 12 years, in which growth was recorded across almost all income segments

So where does this leave investors?

Political events will often lead to knee-jerk reactions when they are unexpected, but seldom do they have a lasting impact. Underlying economic trends and monetary policy tend to be more important and create room for research-based investment to add value. Furthermore, not only are political events hard to predict, but it is not always clear what the market response will be to different outcomes. For example, with the US election, the markets seemed concerned about a Trump victory before the election, but rallied afterwards.

Our portfolios are invested in shares of quality companies with proven track records. We believe these businesses are likely to continue to make money regardless of what’s happening with the market. In fact, despite the current economic and political ambiguity, equity volatility has been subdued while European equity indices are close to all-time highs. We have to be aware of the risks and try to navigate them, but we believe that staying the course usually pays off and therefore we continue to invest for the long term.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience and has been with Capital Group for eight years. Prior to joining Capital, he was head of Australian and New Zealand distribution for Macquarie Bank’s fund management division. Before that, he was global head of relationship management for Macquarie Securities and CIBC World Markets in North America.

5 topics

1 contributor mentioned

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience...

Expertise

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience...

Expertise

Comments

Comments

Sign In or Join Free to comment