The yield play looks very vulnerable

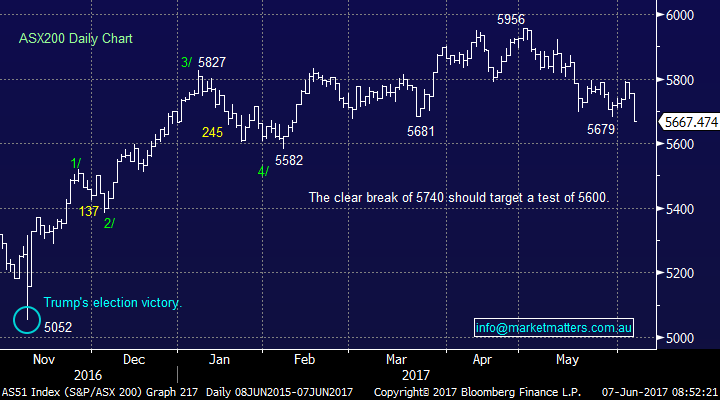

When we said yesterday that considering June’s seasonal weakness investors should keep some ammunition for buying opportunities later in the month, we didn’t imagine the market was literally about to fall off a cliff! Let’s stand back and look afresh at the statistics for May / June since the GFC so we can set some perspective on the markets position and hence generate some specific plans to start deploying the balance of our cash.

1. The average pullback over May / June is 6.9% which targets 5545 from the May 1st high of 5956

2. The average pullback during June since the GFC is a 5.7% which targets 5463 from the June 2nd high at 5793.

3. The average monthly range of the last 10-months is ~250-points but of the last 20-months its over 300-points. Assuming 5793 is June’s high this targets sub 5550.

4. The last major pullback was 559-points in 2016, this extrapolates to the 5400 area.

5. The average low-point in June has been in the last week and very often the last few days.

One of the obvious current concerns is the ASX200 has fallen 289-points (4.85%) while global indices have remained buoyant, hence any weakness overseas is going to make it very hard for our local stocks to get up off the canvas. When we combine the above 5 statistics we get 3 index levels where it becomes logical to commence accumulating further stock i.e. 5550, 5500 and 5450 – note we have pulled back our original 5600 pullback target area. Note, individual stocks may clearly give good entry levels before the index reaches these targets, they are simply used as a guide.

ASX200 Daily Chart

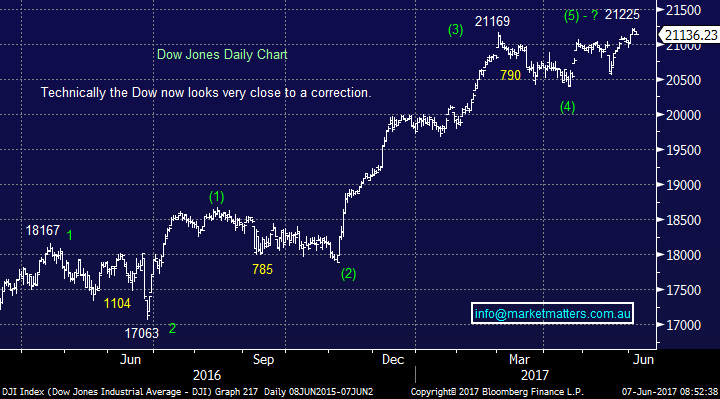

US stocks again drifted marginally lower last night with the Dow closing only 0.6% above the level where we see a technical sell signal being generated i.e. if the Dow closes back under 21,000. We still believe a 4-5% correction is close at hand for US stocks, after its impressive rally since the US election a negative catalyst is probably required but there are plenty of risks lurking in the shadows.

US stocks again drifted marginally lower last night with the Dow closing only 0.6% above the level where we see a technical sell signal being generated i.e. if the Dow closes back under 21,000. We still believe a 4-5% correction is close at hand for US stocks, after its impressive rally since the US election a negative catalyst is probably required but there are plenty of risks lurking in the shadows.

US Dow Jones Daily Chart

Yesterday we pointed out that the recently under pressure banking sector is usually ok in June with the selling more concentrated in the yield play / bond proxy stocks. Right on cue the selling that hit our market yesterday while not ignoring the banks was more directed at this end of town e.g. Real Estate sector -1.78%, Transurban (TCL) -1.49% and Sydney Airports (SYD) -2.2%.

Yesterday we pointed out that the recently under pressure banking sector is usually ok in June with the selling more concentrated in the yield play / bond proxy stocks. Right on cue the selling that hit our market yesterday while not ignoring the banks was more directed at this end of town e.g. Real Estate sector -1.78%, Transurban (TCL) -1.49% and Sydney Airports (SYD) -2.2%.

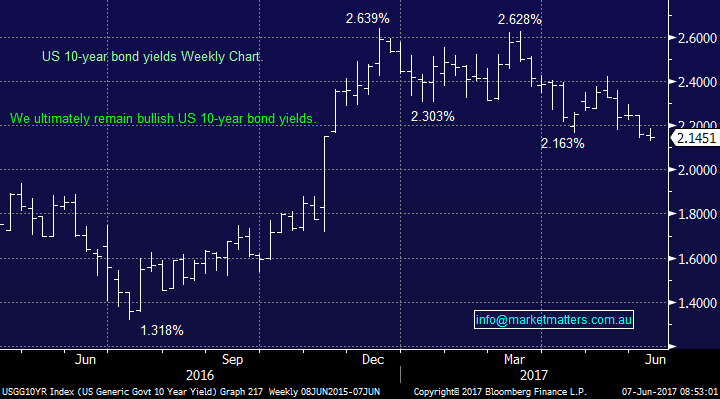

Over the last ~6-months bond yields have drifted lower following their explosive rally at the end of 2016, in short, the world has become less confident in a global economic recovery. This has been the perfect recipe for the bond proxy stocks who have soared, far higher than the “bounce” we anticipated. However we believe bond yields will regain their “mojo” in 2017 which is likely to benefit bank stocks but to the detriment of the yield play / bond proxy stocks.

US 10-year bond yield Weekly Chart

Today we are going to look specifically at the position of SYD and TCL to gauge what degree of correction we think is likely for these 2 headline yield play stocks.

SYD has made fresh all-time highs this month, it feels like it’s become a “go to” stock for fund managers who are very cautious the overall market but need to put some money to work. We believe the stock is now over valued and extremely extended while its 4.12% unfranked dividend is not compelling.

In the short-term we can see a pullback of ~3-4% but an eventual move over $8 remains a strong possibility until bond yields again start to rally. However, we have no interest in buying the stock at elevated levels and eventually do see a pullback towards the $6 region when interest rates resume their recovery higher. As it stands, the market is pricing just 0.79% worth of interest rate hikes out to January 2020 in the US – which seems very undercooked to us!

Sydney Airports (SYD) Monthly Chart

TCL similar to SYD has rallied very strongly as bond yields have drifted lower, making fresh all-time highs this week. TCL’s 3.8% partially franked dividend is not exciting and we would be selling into strength from an investment perspective. Investors should remember that markets move in cycles, TCL was hated in late 2016 dropping by ~25% but has been loved in 2017, the sentiment will eventually turn again but with the bearish move in 2016 still relatively fresh in investor’s minds.

Technically we can see a pullback under $12, around 5% lower, which would give us a trading buy targeting a test of $13 – however given our outlook around US interest rates and the markets current positioning around them, this would not be an investment.

Transurban (TCL) Weekly Chart

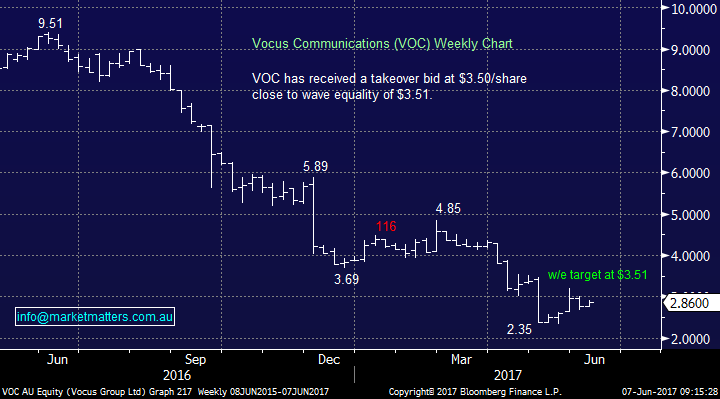

As an aside, Vocus Communications had received a takeover offer this morning at $3.50 per share, which is a +22% premium to the last traded price of $2.86 (however still below the level we sold the stock at $3.775). The proposal is interesting and it might be enough to get other suitors off the sidelines such as the James Spenceley led consortium that is reportedly circling, however the KKR offer at $3.50 is a conditional one, with the main risk being that earnings must be delivered inline with recent guidance of $365m to $375m and net debt cannot be greater than $1.1bn (net debt currently sits at $1.04bn) – implying there can be no further deterioration in the business.

As an aside, Vocus Communications had received a takeover offer this morning at $3.50 per share, which is a +22% premium to the last traded price of $2.86 (however still below the level we sold the stock at $3.775). The proposal is interesting and it might be enough to get other suitors off the sidelines such as the James Spenceley led consortium that is reportedly circling, however the KKR offer at $3.50 is a conditional one, with the main risk being that earnings must be delivered inline with recent guidance of $365m to $375m and net debt cannot be greater than $1.1bn (net debt currently sits at $1.04bn) – implying there can be no further deterioration in the business.

Interestingly, one of the many things we look at in terms of markets, is wave equality. In terms of Vocus, the last rally in the stock from $3.69 to $4.85 was $1.16. Given the bid price of $3.50 and the recent low of $2.35, this equates to a move of $1.15! Markets tend to have an uncanny ability to repeat themselves, and Vocus is another example of this.

Vocus (VOC) Daily Chart

Conclusion (s)

We are short-term bearish the yield play stocks looking for a ~4% correction from current levels. While we see a correction under $12 as a trading buy for TCL, any rallies to fresh highs we see as selling opportunities for investors in the bond proxy stocks.

Prices as at 07/06/2017. 7.50AM.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 topic

2 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment