What APRA's announcement on dividends means for equities, deposits, bonds and hybrids (+ some stress-testing)

These are some exciting times for investors across the banks' capital structures, spanning equity, hybrids, subordinated bonds, senior bonds, deposits, and the safest AAA rated secured covered bonds.

On Tuesday APRA announced that it is encouraging banks to make "prudent reductions in dividends, taking into account the uncertain outlook for the operating environment and the need to preserve capacity to prioritise these critical activities".

I applaud APRA's differentiated approach to ensuring depositors are protected by the safest banks in the world. Importantly, APRA has been conspicuous in not blindly following its (inferior) regulatory peers overseas by banning dividends outright, which is necessary in jurisdictions where banks have been myopically allowed to operate on much skinnier capital ratios.

If APRA did adopt this lowest-common-denominator-approach, it would be bundling our banks with, frankly speaking, all their dud peers overseas with no acknowledgement at all of their world-beating capital ratios.

On Tuesday Bank of Queensland also announced that it was repaying its $150m Wholesale Capital Notes hybrid security that was due to be called in May with APRA's explicit approval. BoQ noted that it would issue a replacement security once market conditions stabilise. This is important given there was some apprehension that BoQ would not meet expectations, and follows the trend set by other banks, including Macquarie and NAB, which repaid about $1.74 billion of their hybrids in March (again with APRA's approval), even though they did not end up issuing replacement hybrids. Likewise, Westpac repaid a $1.1 billion Tier 2 subordinated bond last month without issuing a successor security. And, finally, Challenger has secured APRA approval to repay its CGFPA hybrid at a future quarterly distribution date when conditions normalise and it is able to launch a replacement instrument.

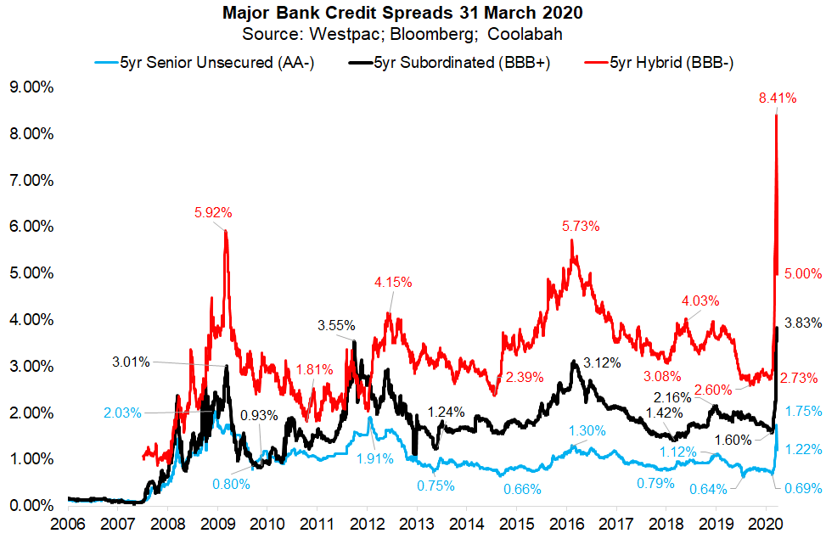

All of this is exceedingly pragmatic. The banks could potentially issue new debt and hybrid securities right now if they really had to, but it would be heinously expensive, pushing up their funding costs, which would have to be passed on to business and household borrowers in the form of higher lending rates. At a time when credit spreads are incredibly high, and the banks are seeking to act as one of "Team Australia’s" shock absorbers through a deep, albeit temporary, crisis, this would be completely counterproductive.

APRA's statement on Tuesday has been very carefully constructed to emphasise the significance of "the next couple of months" and crucially gives the major banks cover if they want to defer a half-yearly dividend until their full-year results or pay a much smaller one at the half-year. Three of the four majors report their half-year numbers in about a month with CBA releasing its full-year results in August.

I expect one of the majors to potentially defer its half-yearly dividend to focus on prudently building capital while the two others that report soon will probably pay a substantially reduced distribution. All of this is "credit positive" for depositors, bond-holders, and hybrid investors.

In this context, APRA explicitly states the while over the next couple of months it expects banks "will seriously consider deferring decisions on the appropriate level of dividends until the outlook is clearer...where a Board is confident that they are able to approve a dividend before this, on the basis of robust stress testing results that have been discussed with APRA, this should nevertheless be at a materially reduced level".

This gives the major banks the flexibility of deferring their half-year dividend until the full-year, or paying a substantially reduced one with APRA's blessing once various hurdles have been met. Again, my base-case is one defers, and two pay. In the case of the latter, APRA has encouraged the banks to use dividend reinvestment plans to support capital generation.

CBA is carrying massive excess capital of about $4 billion and can be counted on to distribute a reasonable dividend following the end of its full-year in August, especially considering the hundreds of thousands of retirees who hold bank stocks for their attractive yields.

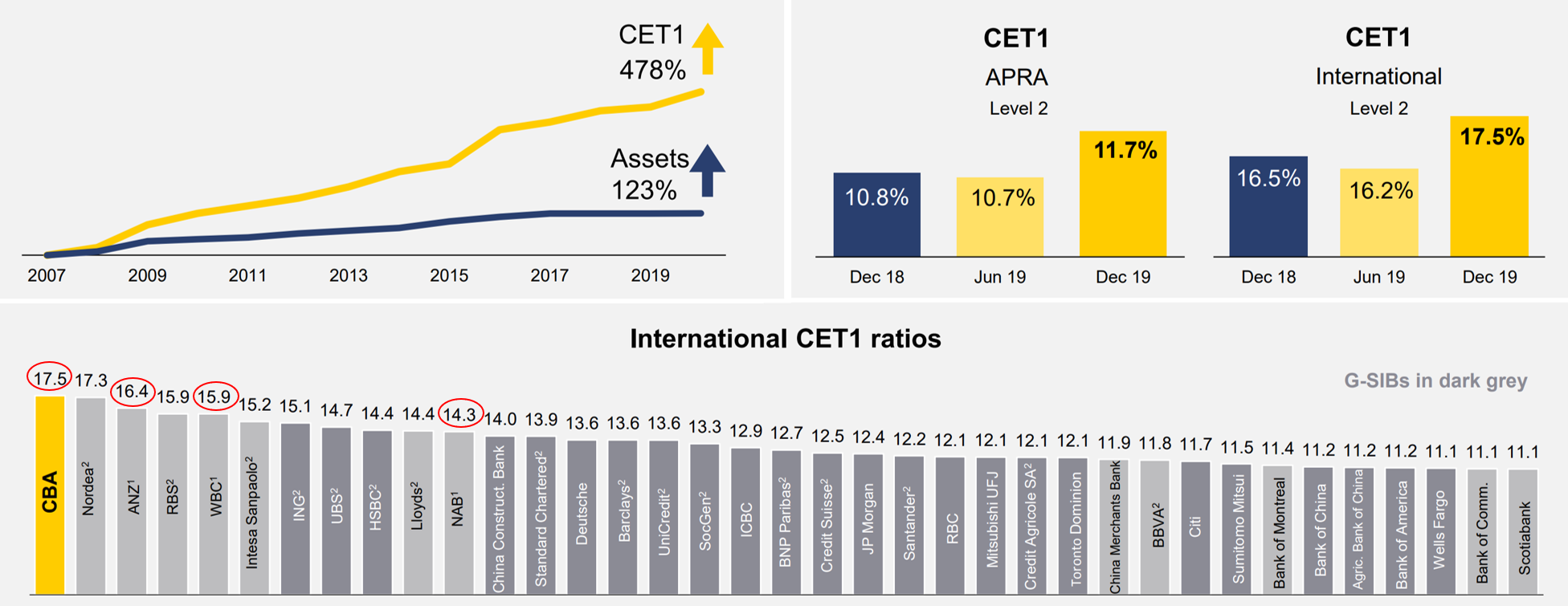

Focusing on retaining profits to support the banks' common equity tier one (CET1) capital buffers is unambiguously good news for creditors. A more interesting question is how bad the crisis could get, and what it means for loan losses and the banks’ capital ratios. On an internationally-harmonised basis, CBA’s 17.5 per cent common equity tier one (CET1) capital ratio ranks higher than any other large bank globally according to its latest results presentation. (ANZ ranks third, Westpac fourth, and NAB tenth.)

The “unquestionably strong” core equity buffers the banks have accumulated since 2014 protect creditors from losses in the event that loan losses spike. These first-loss reserves have been augmented by a huge increase in conservatism across the financial system as banks divested riskier non-core businesses and substantially enhanced the quality of their lending standards.

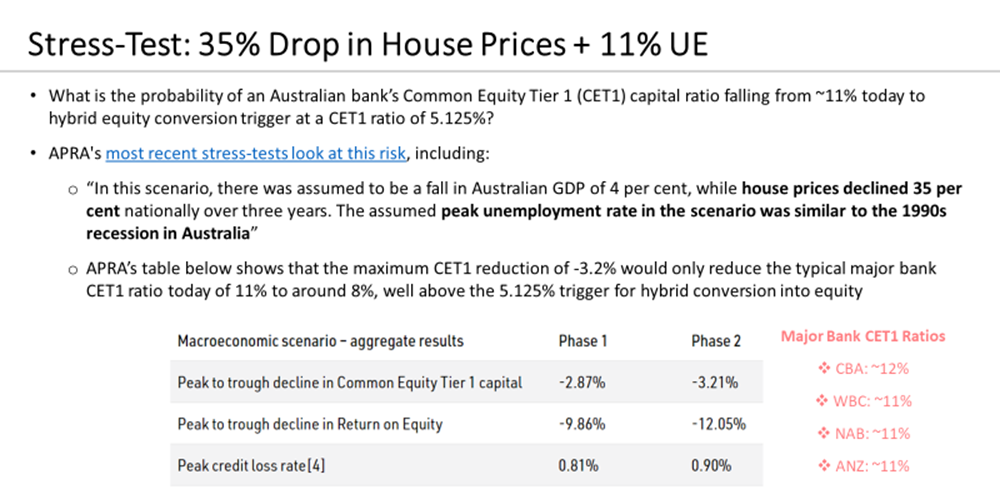

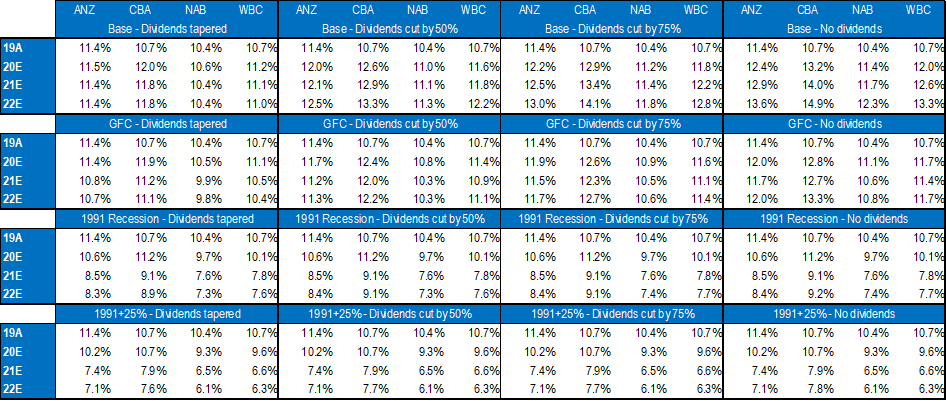

In APRA’s latest published stress-test of bank balance-sheets, the regulator assumed a scenario worse than the GFC with a 35 per cent drop in house prices and an increase in unemployment to around 11 per cent, amongst other adverse inputs. APRA found that average bank capital ratios only fell by around three percentage points, which would reduce the major banks’ CET1 ratios from 11 per cent currently to circa 8 per cent. This is way above the 5.125 per cent CET1 threshold at which point the bank’s hybrid securities are converted into equity. It was also a change from stress-tests in years prior when the banks were not as well capitalised.

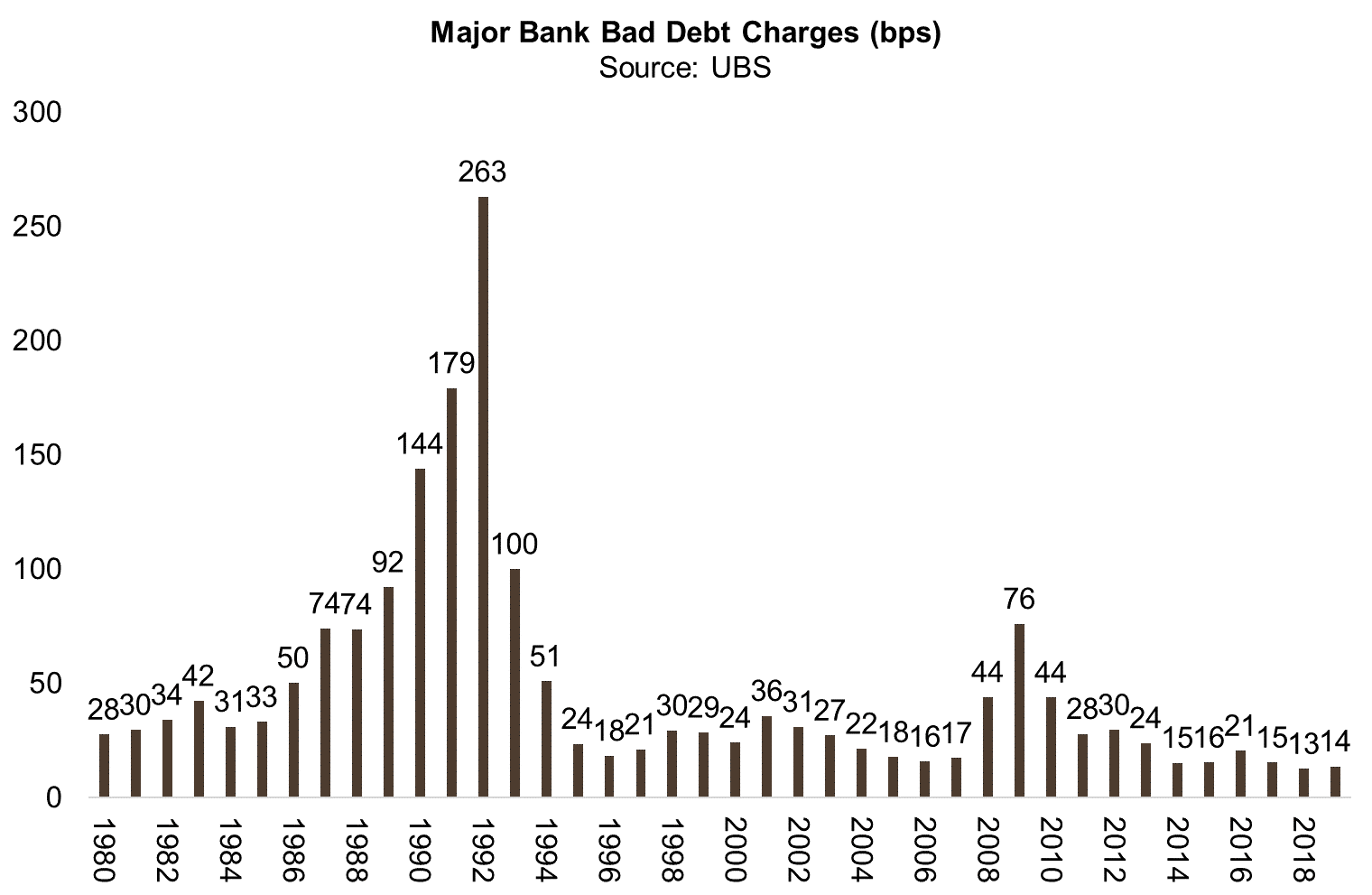

My analysts have run a range of even more challenging scenarios, including a recession that is assumed to be 25 per cent worse than the 1991 downturn when the banks’ bad and doubtful debt (BDD) charges soared to almost 3 per cent (specifically, 263 basis points) of their gross loans in 1992. That is almost 10 times worse than the peak losses assumed by Standard & Poor’s in its downside modelling and multiples the losses APRA's stress-test projected.

In 1991 the major banks were much less risk-averse and far more free-wheeling with their lending standards. They also did not have government-guaranteed deposits or access to special emergency lending facilities via the RBA's Committed Liquidity Facility. And they did not pay over $1 billion in annual taxes to the government for the implicit public guarantee on their senior bonds (via the wholesale liability levy), which S&P recognises with a two notch rating upgrade to AA-.

When my team jacks-up loan losses to levels that are 25 per cent worse than the experience between 1990 and 1993, they find that the banks’ CET1 ratios still bottom-out in the 6.3 per cent to 7.8 per cent range at their nadir (see table below). While APRA’s hard-nosed approach to deleveraging the banks since 2014 has been tough for shareholders to bear via lower returns on equity, it has bequeathed depositors and creditors the safest banks in the world.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Disclaimer: This information has been prepared by Smarter Money Investments Pty Ltd. It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not an indicator of nor assures any future returns or risks. Smarter Money Investments Pty Limited (ACN 153 555 867) is authorised representative #000414337 of Coolabah Capital Institutional Investments Pty Ltd, which holds Australian Financial Services Licence No. 482238 and authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271.

4 topics

5 stocks mentioned

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment