What do French elections mean for markets?

The French Presidential elections (final round run-off will be 7 May) and Legislative elections (11 and 18th June) remain the last of the major Eurozone political events for the year in that the outcome of the German elections (24th September), dare we say, seem far less important given the likely mainstream choices. We don’t believe we can add much value in attempting to predict outcomes other than to observe that the French version of parliamentary democracy seems designed for inertia, even more so than the U.S. version, in that the President has very little real power without the backing of Parliament. Whilst a Le Pen victory would likely trigger a round of Eurozone risk aversion, it should not be equated with a French exit from the Eurozone. That would remain a very complicated and, hence, unlikely outcome regardless of how aggressively markets wish to price this.

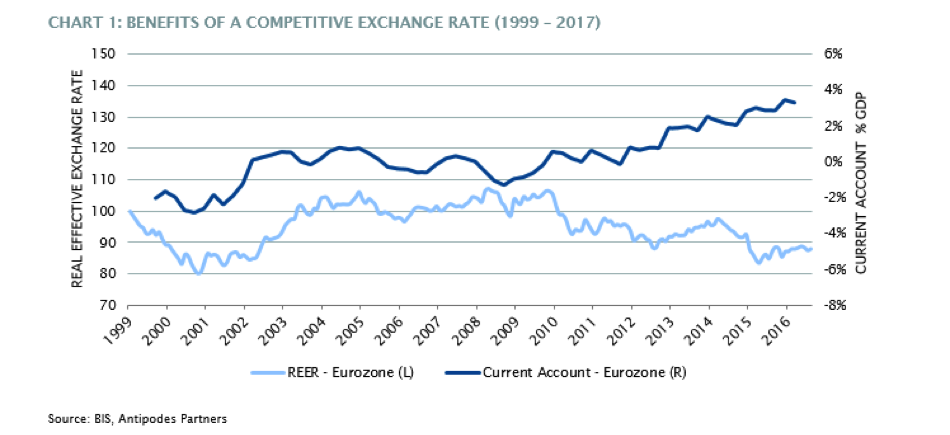

On the flipside, absent a negative political surprise, post the French elections, the European Central Bank (ECB) will come under pressure to normalise policy. European economic fundamentals are much stronger than the headlines imply. Based on a workforce participation measure of employment, the Eurozone recovery in employment has been stronger than that in the U.S. This shouldn’t surprise given the Euro is super-competitive trading close to its lows on a Real Effective Exchange Rate (REER) basis (Chart 1). Further, the data suggest that in the face of uncertainty Europeans have deferred consumption which may ultimately result in a catch-up phase and a much more durable recovery.

Given Europe’s status as a very large exporter of savings to the rest of the world, the knock-on effects of such a potential policy normalisation should not be underestimated (beyond the potential for the Euro to rebound, just a general tightening in global liquidity conditions). Already the ECB is discussing hiking rates even as it keeps up its rate of QE, i.e. reversing the order of tightening that the Federal Reserve adopted. Why would it do this? Primarily to improve the profitability of the European banking sector, encourage lending whilst also keeping a lid on sovereign yield spreads. Ironically, according to our heat-map, the cheapest sector globally is European Financials, the direct beneficiaries of such a policy.

In summary, the Eurozone bond market (and European Domestic facing equities, especially Financials) are discounting a deep deceleration in growth at the same time that North American domestic-facing equities are discounting a reacceleration in growth. Without wanting to make a big call either way, we believe it’s highly likely that both markets are mispriced.

At the core of our investment philosophy, we seek in our long investments both attractively priced businesses (margin of safety) and investment resilience (characterised by multiple ways of winning), with the opposite logic applying to our shorts. Whilst the investment case will always be predicated on idiosyncratic stock factors such as competitive dynamics, product cycles, management and regulatory outcomes, we seek to amplify the investment case by taking advantage of style biases and macroeconomic risks/opportunities.

In our last quarterly report, we noted that the blind assumption of unendingly low rates made the market vulnerable to a cyclical back-up in yields. Whilst this thesis initially played out and has partially reversed, we believe the risk is still asymmetrically priced. Accordingly, we are avoiding expensive versions of the bond proxies as long investments, accumulating selective opportunities, especially in Europe, that have suffered the most from yield curve compression whilst increasing our shorts on the beneficiaries of the low rate world, i.e. expensive bond proxies and growth.

In conclusion, we’re encouraged by the growing valuation dispersion within and across markets (region/sector/factor) as we think this is indicative of broadening pragmatic value opportunities, both long and short.

To find out how Antipodes Partners has positioned itself in global markets, read our March Quarterly Report: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jacob Mitchell is Antipodes’ chief investment officer. He is an award-winning fund manager, with more than 25 years' experience investing in equity markets. Jacob founded Antipodes in 2015 after deciding to leave Platinum Asset Management where he spent 14 years and worked as deputy chief investment officer and a portfolio manager of the flagship Platinum International Fund.

Jacob holds a Bachelor of Commerce from the University of Western Sydney.

3 topics

Jacob Mitchell is Antipodes’ chief investment officer. He is an award-winning fund manager, with more than 25 years' experience investing in equity markets. Jacob founded Antipodes in 2015 after deciding to leave Platinum Asset Management where he...

Expertise

Jacob Mitchell is Antipodes’ chief investment officer. He is an award-winning fund manager, with more than 25 years' experience investing in equity markets. Jacob founded Antipodes in 2015 after deciding to leave Platinum Asset Management where he...

Expertise

Comments

Comments

Sign In or Join Free to comment