Where are we in the global investment cycle?

It’s now a decade since the first problems with US sub-prime mortgages started to appear and nearly eight years since share markets hit their global financial crisis lows. From those lows in 2009 lows US shares are up 239%, global shares are up 167% and Australian shares are up 80% (held back by relatively higher interest rates, the absence of money printing, the plunge in commodity prices from their 2011 highs and the high $A). An obvious question is how close the next downturn is, which ultimately relates to where we are in the investment cycle.

Key points:

- We are still a long way from the peak in the investment cycle. There is little sign of economic excess globally: underlying inflation is low; spare capacity remains; there is no sign of overinvestment; credit growth is modest; monetary conditions are not tight; share market valuations are okay, and investors are not euphoric.

- The cyclical bull market in shares has more upside.

The long US cyclical bull market

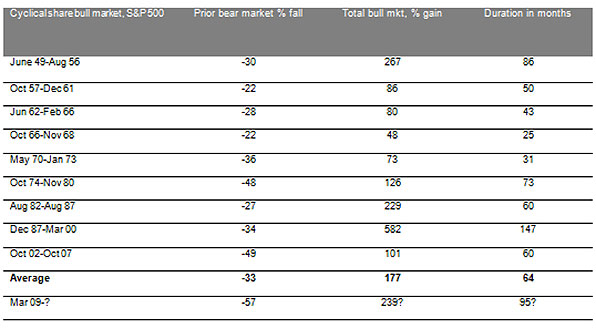

Where we are in the investment cycle is particularly pertinent in relation to the US. The cyclical bull market in US shares that started in March 2009 will be eight years old in March. It’s the second longest cyclical bull market since World War Two in terms of time and the third strongest in terms of percentage gain. See the next table.

Cyclical bull markets in US shares since WW2

I have applied the definition that a cyclical bull market is a rising trend in shares that ends when shares have a 20% or more fall (i.e., a cyclical bear market). Source: Bloomberg, AMP Capital.

Similarly, according to the US National Bureau of Economic Research, the current US economic expansion that started in June 2009 at 92 months old is the fourth longest since 1929 and compares to an average expansion of 70 months. With the US cyclical bull market and economic expansion both now long in the tooth, some fear that US shares are vulnerable to another bear market and by implication given the direction setting influence of the US share market, global and Australian shares would be vulnerable too. A related concern is that, with the US economic expansion already longer than normal, any stimulus that President Trump may provide risks overheating the US economy and much higher interest rates which could bring on a bear market.

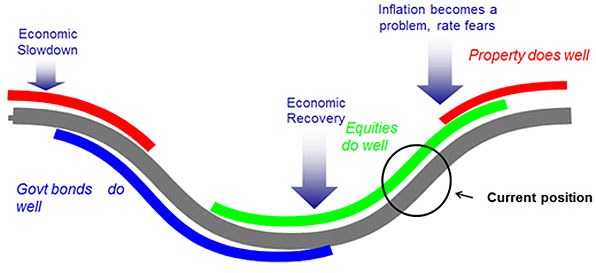

The investment cycle

The next chart shows a stylised version of the investment cycle where the thick grey line represents the economic cycle.

Source: AMP Capital

A typical cyclical bull market in shares has three phases:

- Scepticism - Phase 1 normally starts when economic conditions are still weak, and confidence is poor, but smart investors start to see value in shares helped by ultra-easy monetary conditions, low-interest rates and low bond yields.

- Optimism - Phase 2 is driven by strengthening profits as economic growth turns up and investor scepticism gives way to optimism. While monetary policy may start to tighten, it is from very easy conditions and will remain easy as inflation remains low. Therefore, bond yields may drift higher but not enough to derail the cyclical bull market in shares.

- Euphoria - Phase 3 sees investors move from optimism to euphoria helped by strong economic and profit conditions which pushes shares into overvalued territory. Meanwhile, strong economic conditions drive signs of economic excess – overinvestment, full capacity utilisation, surging private sector debt, high and surging inflation – which forces central banks to move into tight monetary policy, in turn pushing bond yields significantly higher. The combination of overvaluation, investors being fully loaded up on shares and tight monetary policy sets the scene for a new bear market.

Typically the bull phase lasts 3-5 years. But it varies depending on how quickly recovery precedes, excess builds up, inflation rises, and extremes of overvaluation and investor euphoria appear. As a result “bull markets do not die of old age but of exhaustion”.

So where are we now in the investment cycle?

So right here the big question is: are we in the “euphoria” phase that ultimately leads to the “exhaustion” of the cyclical bull market in shares and the next bear market? The best way to look at this is to look at economic conditions, monetary conditions, share market valuation and investor sentiment and positioning:

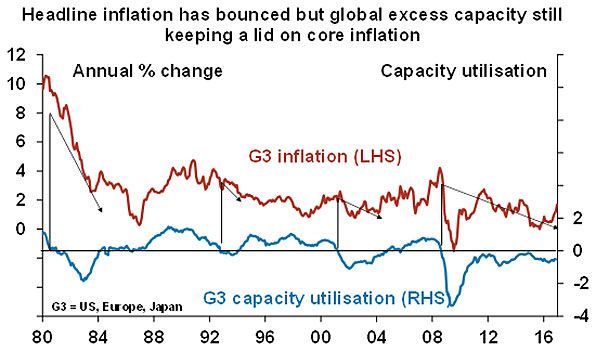

Firstly, in terms of economic conditions, it’s hard to argue we are in the “euphoria” phase. There are few signs of economic excess:

- While headline inflation is rising globally, this largely reflects the bounce in oil prices. Core inflation in major countries ranges between zero (Japan) to 1.7% (US), i.e. far from out of control.

- After years of below trend growth globally, spare capacity still remains, and this will constrain core inflation. Similarly, wages growth remains depressed even in the US (at around 2.5% year on year) despite a tighter labour market.

Source: Bloomberg, AMP Capital

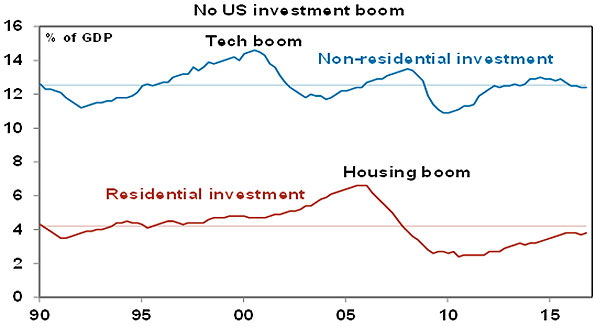

- There is no sign of overinvestment globally – in fact, there has been too little investment. While the US recovery is further advanced, even here business investment (excesses in which preceded the tech wreck) and residential property investment (excesses in which preceded the GFC) are around or below their long-term averages relative to GDP.

Source: Thomson Reuters, AMP Capital

- Overall private sector debt growth is modest in most countries (except for corporate debt in the US and China).

Secondly, global monetary conditions remain easy and in the absence of broad-based excess (in growth, debt, or inflation) look likely to remain so. Yes, the Fed is likely to hike rates more aggressively this year, but it’s still from a very easy base and other central banks (including the RBA) are either on hold or easing. So a shift to tight money that brings an end to the economic cycle looks a fair way off.

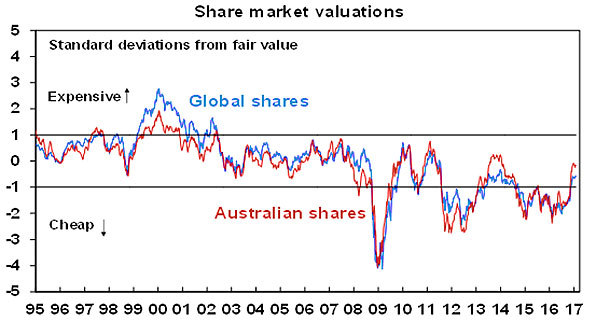

Thirdly, share market valuations are mostly okay. Sure, measured in isolation against their own history shares are no longer cheap. In fact, forward price to earnings multiples in the US and Australia are above long-term averages. However, once the gap between share market earnings yields and still low bond yields is allowed for, shares are fair value to cheap depending on the market (next chart).

Source: Bloomberg, AMP Capital

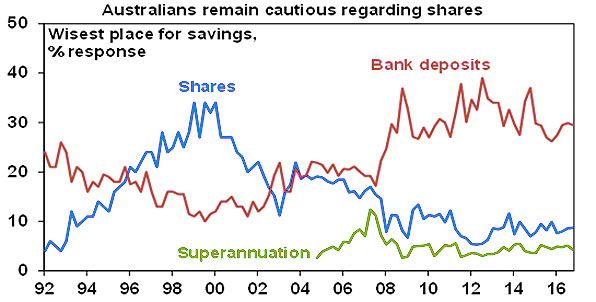

Fourthly, while short term investor sentiment is excessively bullish long-term measures of positioning are not. In the US the huge investor flows into bond funds over the last few years have yet to reverse in favour of shares. In Australia, sentiment towards shares as a wise destination for savings remains low and investors still prefer bank deposits. No euphoria here.

Source: Westpac/Melbourne Institute, AMP Capital

Finally, while the US cycle is more advanced, it could be argued that the 19% fall in US shares in mid-2011 was a bear market. So the bull market in US shares is perhaps not so old after all! Moreover, major non-US share markets and Australian shares did have a bear market in both 2011 and 2015-16, so their cyclical bull markets are not old at all. In this regard, European and Japanese share markets are relatively attractive thanks to cheaper valuations and still dovish central banks.

Overall, we are still not seeing the signs of excess, euphoria and exhaustion that typically come at cyclical economic and share market peaks. So barring some sort of external shock, the cyclical bull market in shares looks like it still has further to go – particularly if global economic growth returns to more normal levels which in turn will help earnings.

With regard to any Trump fiscal stimulus, this analysis suggests there is still a bit of room for it before it causes the US economy to overheat. Particularly if the US dollar continues to trend higher, which takes some off the pressure of the Fed to raise rates. In any case, it’s looking likely that fiscal stimulus in the US won’t hit until late this year and will unlikely to be more than 1% of US GDP given the constraints Congress is likely to impose. In fact, the focus is more likely to be on providing a boost via economic reforms – deregulation, tax reform and inducements to invest - rather than traditional stimulus.

Investment implications

First, while corrections should be anticipated – with Trump and upcoming Eurozone elections being potential triggers – we still appear to be a long way from the peak in the investment cycle.

Second, non-US share markets and economies – notably Japan and Europe - are less advanced in their cycles and so provide opportunities for investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

3 topics

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management