Why do we own Facebook?

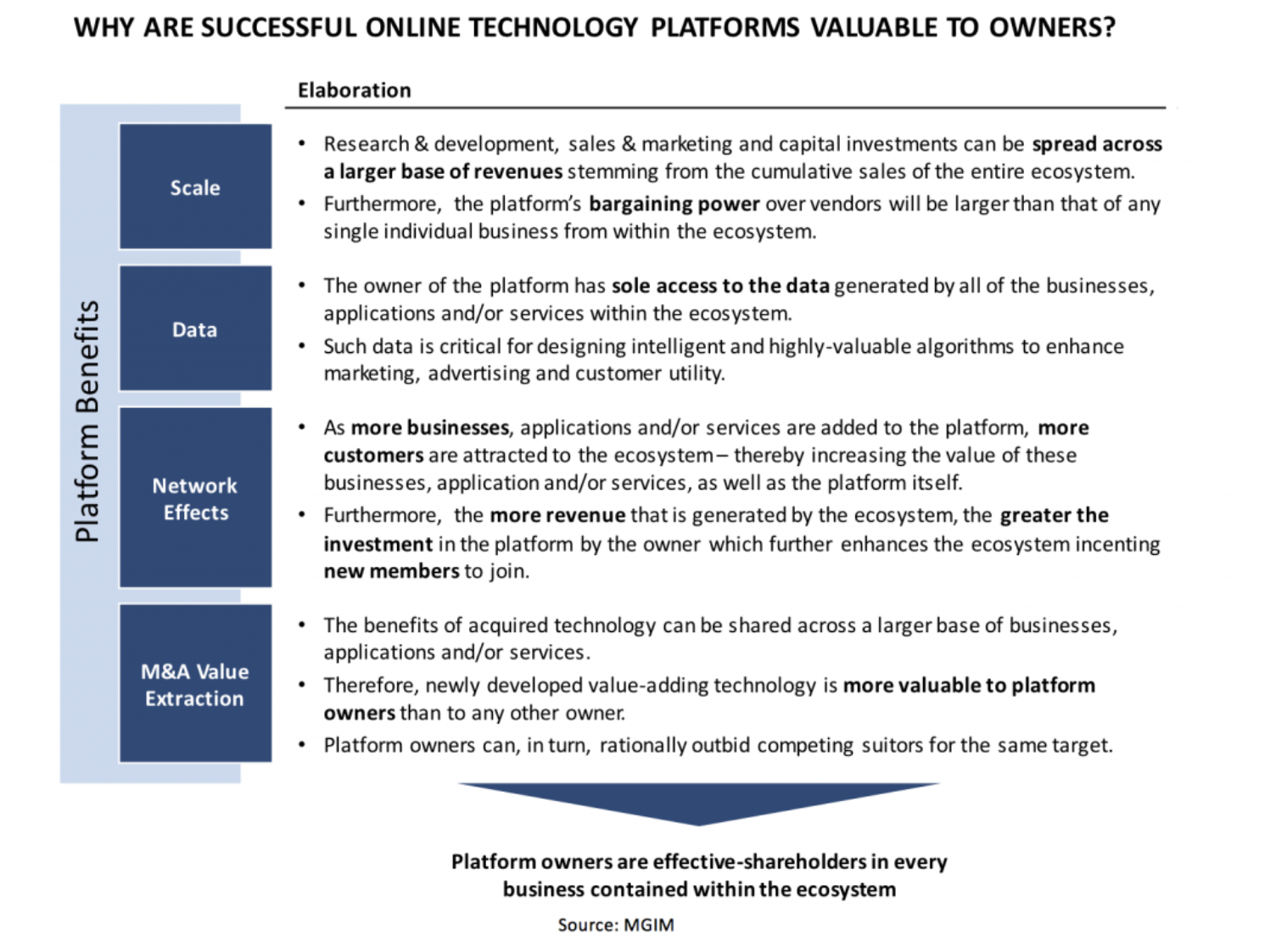

At Montgomery Global, we believe the online technology platform is a special business model that, if successful, will deliver owners supernormal returns for a long period of time. As positive network effects compound the value of the platform’s ecosystem for all users, the ecosystem grows, and with it does the scale of the platform, its access to valuable data and its ability to monetize new (or acquired) technology over the existing platform.

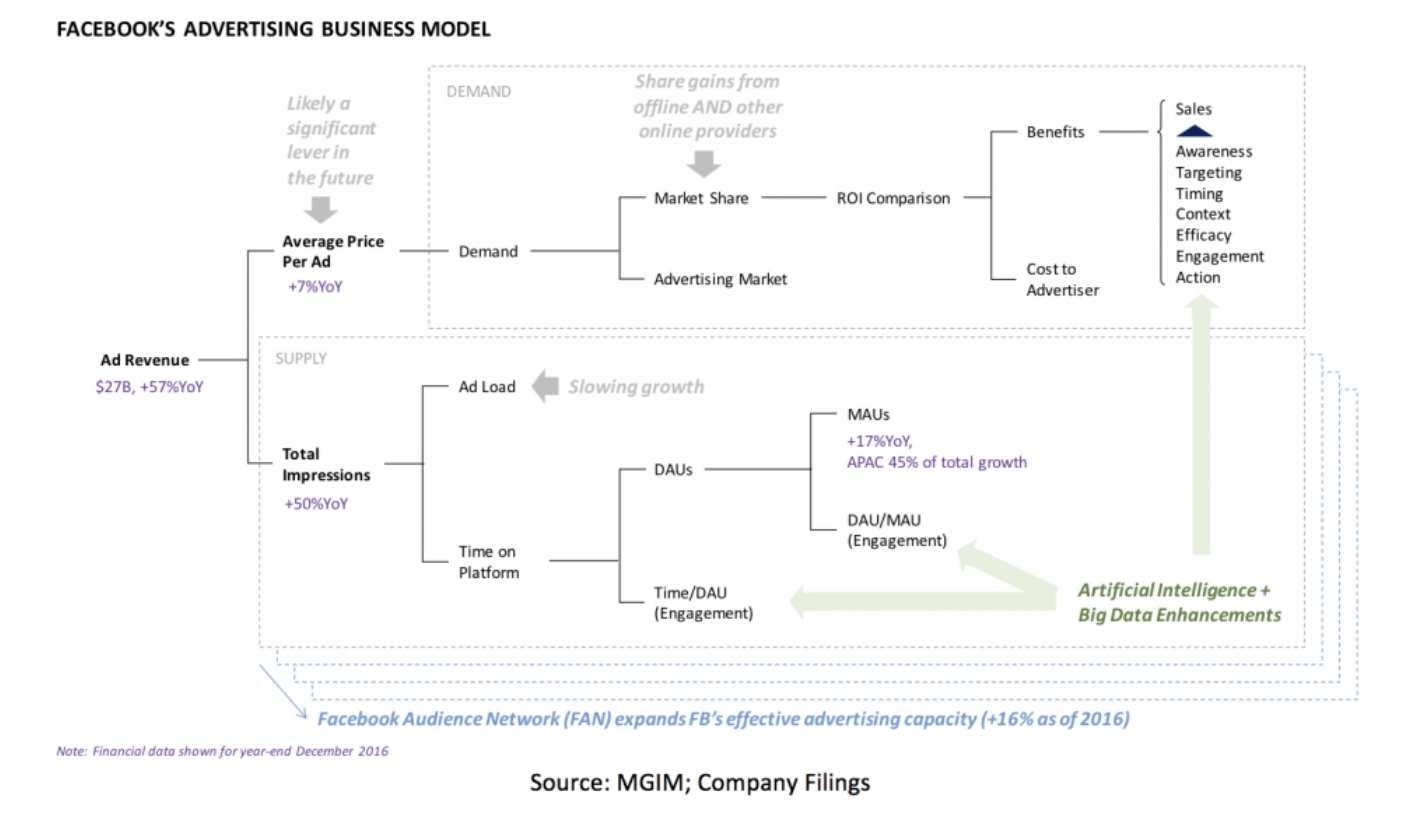

One of the world’s great online technology platforms today is a little business called Facebook (NASDAQ: FB). Facebook is the clear winner when it comes to social networking in the world (ex-China). With 1.9 billion monthly-active-users (MAUs), Facebook has built an enormous and ever-growing database of personal information on more than quarter of the world’s population. And it has created an advertising platform upon which advertisers can target cohorts of Facebook members based on highly-specific criteria. This, in-turn, dramatically increases the efficacy of advertising on the Facebook platform – and hence, a rapidly growing amount of ad spend has been diverted towards Facebook over recent years. (Facebook’s advertising revenue grew by +51 per cent in its most recent quarter compared to one year prior).

The key to understanding Facebook is to understand its advertising model. We believe Facebook’s advertising business model can be summarised by the chart below. Essentially, Facebook can generate both “demand” for its advertising by improving its efficacy; and “supply” of impressions by driving up user engagement and time spent on its properties, ad loads (though this has almost maxed out) and via non-Facebook mobile sites following the creation of the Facebook Audience Network (FAN). Over time, we believe Facebook could charge a lot more for the value it offers advertisers. Said another way, the vast majority of Facebook’s revenue growth to date has been driven by market share gains, not pricing power.

Facebook’s advertising business, driven by four million active advertisers, is highly-diversified and, we believe, resilient. Facebook’s advertising revenue growth has been broad-based across all regions, marketer segments and verticals. Its largest 100 advertisers represent less than 25 per cent of the company’s total advertising revenues. The business generates roughly half its revenue in the US, with the remainder stemming from around the world (ex-China, North Korea and Iran in which Facebook is banned).

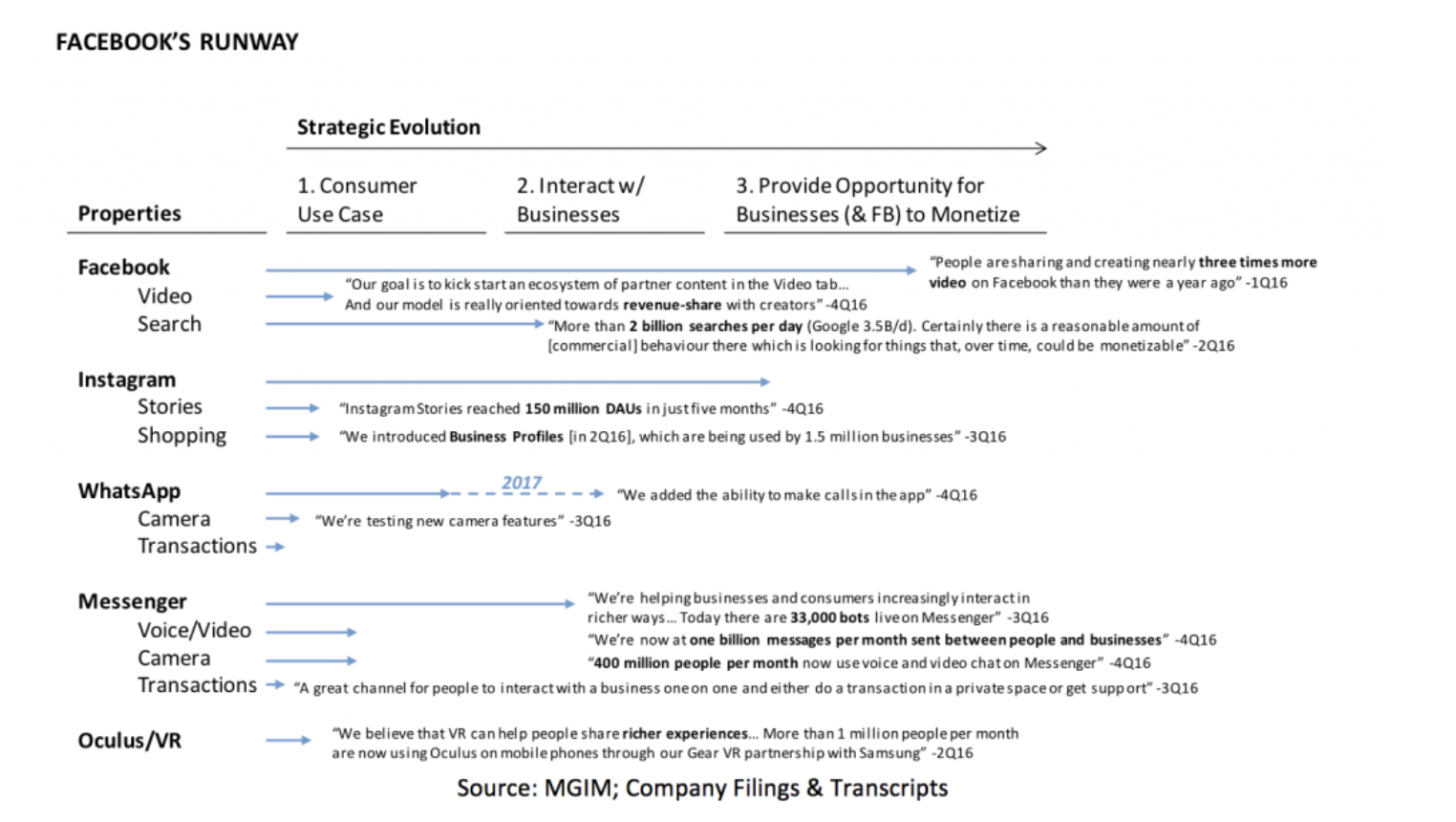

As if this advertising platform were not enough, Facebook owns a number of other properties that are in only the very early stages of monetisation. Now, before Facebook will attempt to monetise a property, it will go to great lengths to build a consumer use case or value proposition. Following this, it will then facilitate the interaction with businesses on the property. Then, and only then, will Facebook attempt monetisation. This is the company’s “strategic evolution” which it follows.

Shown below are Facebook’s properties and the stages they are at with respect to their respective strategic evolutions. And Facebook’s other properties are social network behemoths in their own right. Consider that Instagram already has around 600 million MAUs, WhatsApp 1.2 billion MAUs and Messenger more than 1 billion MAUs. Yet these properties are generating an almost-negligible amount of revenue at the moment. And we know messaging apps can become wildly profitable – just look at Tencent’s WeChat messaging app in China! From this perspective, we believe Facebook has a long runway ahead to continue growing its revenues and earnings.

Of course, understanding the extraordinary extent of Facebook’s business quality is a necessary, but insufficient, condition for us to own its stock. We also need to ensure that the business is undervalued. In the case of Facebook, we believe the growth expectations built into the stock’s current price, while strong, remain conservative relative to the opportunity that lies ahead for the Facebook platform. Remember, successful online technology platforms are uniquely attractive in the sense that, as they grow, so too does their ability to add value to all who participate in their ecosystem. We believe Facebook is an extraordinarily high-quality business with an intrinsic value that has not yet been fully recognised by the market.

The Montgomery Global Funds own shares in Facebook

If you want easy access to online technology platforms invest in the Montgomery Global Equities Fund (Managed Fund) (ASX: MOGL) and receive or reinvest a minimum targeted yield of 4.5% p.a. To access the PDS and find out more, please visit the MOGL website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

2 topics

1 stock mentioned

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets