Why is the market ignoring the growing anxiety in China?

Chinese stocks are now trading below the level they were in 2015 when they caused major global uncertainty and a massive uptick in volatility after they lost 30% in a few short weeks.

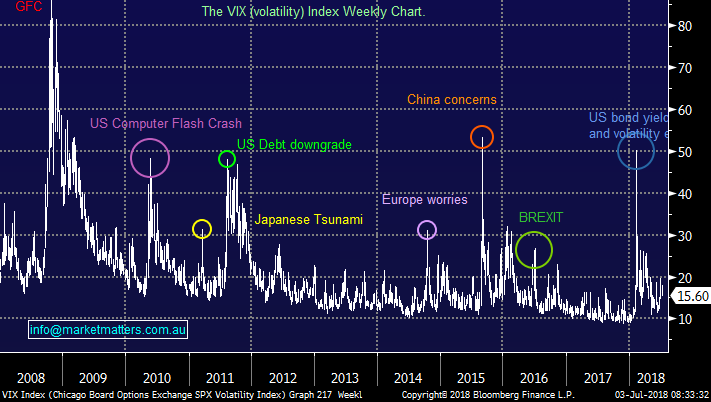

The concern then was that a slowdown in the world’s economic growth engine would lead to a new financial crisis. The VIX traded to its highest level since the height of the GFC and we saw US stocks drop by around ~10% towards the end of 2015.

Markets subsequently settled down and recovered before another bout of anxiety took hold in early 2016 following economic growth numbers that were below market expectations. That triggered another drop in global equities, this time around ~14% for US stocks, however volatility remained below the 2015 levels.

In the ~9 years since the GFC, China has been the cause of the biggest drop in equities and the highest spike in volatility.

This prompts the obvious question: why is the market ignoring the growing anxiety in China?

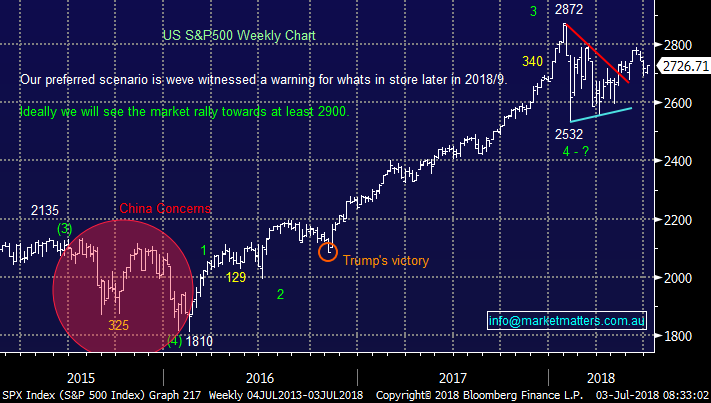

S&P 500 Chart

Volatility Index Chart

Shanghai Composite Chart

Trade war starts to bite

Yesterday we saw Chinese equities book their 5th largest decline for the year as concern around a potential trade war escalates. China has the most to lose in this tussle given that the US is the region’s biggest export market + China is the biggest exporter of goods globally.

A reduction in global trade overall shrinks China’s addressable market for their products which is obviously a negative influence on Chinese economic growth. The last two Chinese led declines for global equities came on the back of growth concerns.

Chinese equities are now down 13.06% over the past 12 months, with the lion’s share of those falls coming in the last few months. The most obvious exposure to Chinese growth for Australia is borne through resources which have been frustratingly strong in the last few weeks.

We’re now very underweight the sector looking to buy weakness which has proven elusive to date, however the overnight moves across the commodity complex and the weakness we’re seeing in the Chinese market has us more confident that we’ll be able to get set back in the resource stocks into further weakness.

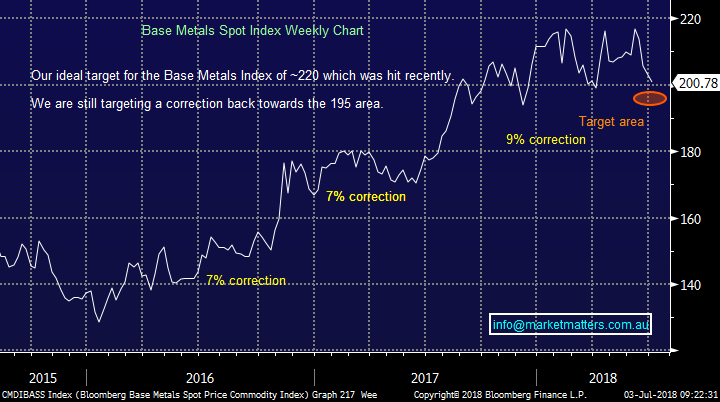

Base Metals Spot Index Chart

The first 2 resource stocks MM are looking to buy into weakness are BHP & OZL.

1 BHP Billiton (BHP) $33.60

No surprises following our recent reports that BHP is our number one pick with capital returns coming soon and they are likely to be huge. The stocks fairly volatile and even while its doubled in the last 2-years it’s still managed retracements of 18.7%, 21.1% and 12.5% - a ~16% correction from the 2018 high which is well within these degrees of recent corrections.

MM is looking to buy BHP below $30.00, or ~10% lower

BHP Billiton (BHP) Chart

2 OZ Minerals (OZL) $9.48

We’ve been looking at Oz Minerals since we took profits too early from our last foray in the Copper stock.

MM likes OZL below $9, where it was trading back in April

Oz Mineral (OZL) Chart

Conclusion

The bubbling trade war between the US and China is having a bigger impact on China at present. Chinese equities have been very weak which should be a warning sign for our commodity stocks, and markets more generally. We’re likely buyers of BHP and OZL into further weakness

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 topic

2 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment